Inside this report

This report examines how price discovery, liquidity depth and spread behaviour differ across venues and what that means for institutional trading strategies.

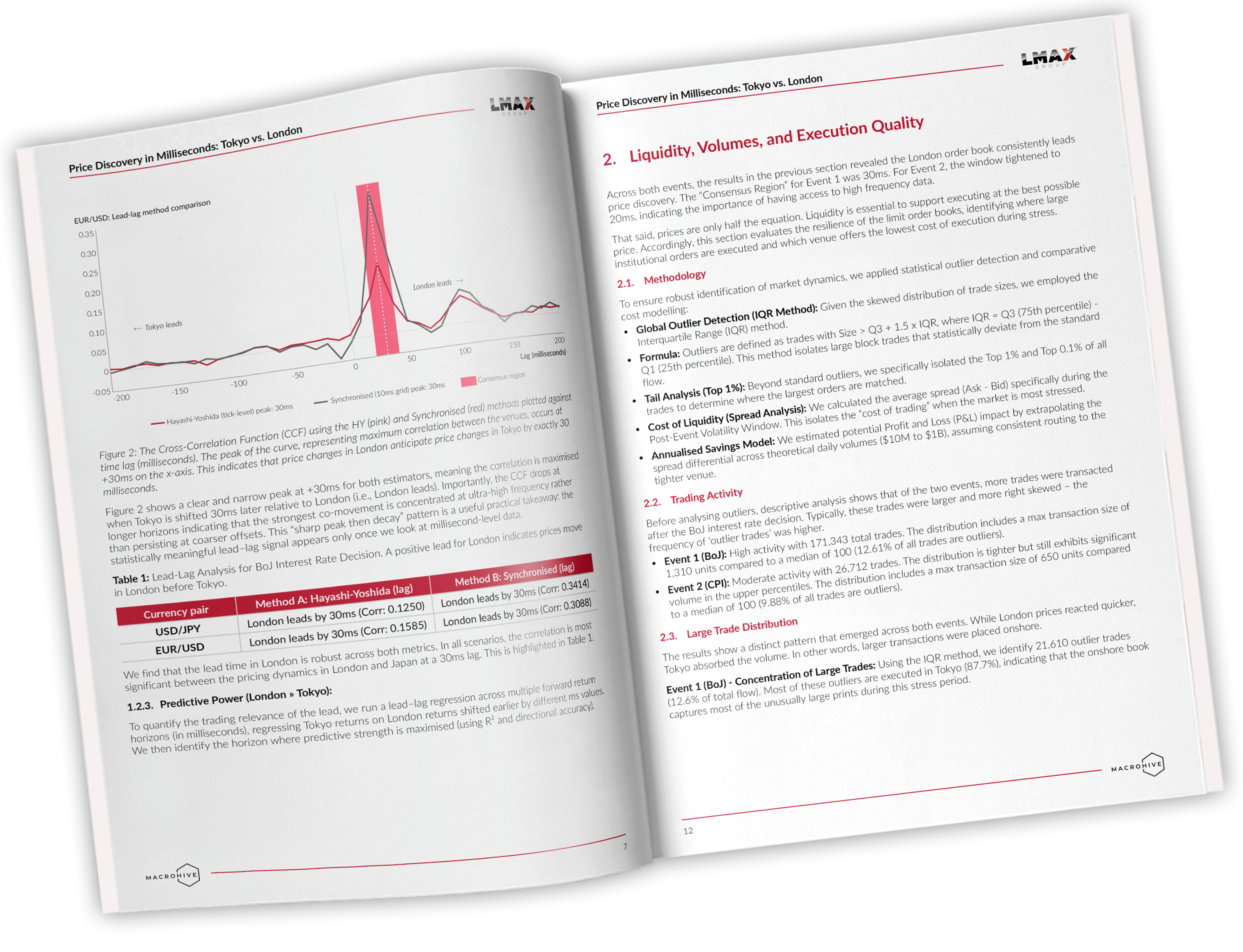

Millisecond change point detection and lead lag modelling show London reacting 20 to 30 milliseconds earlier than Tokyo, with statistically measurable predictive relationships.

While offshore venues lead price discovery, 100 percent of the largest trades in the top 1 percent were executed in Tokyo, highlighting differences in liquidity concentration.

During the February CPI release, London USD/JPY spreads widened to approximately 6.38 pips while Tokyo remained around 1.47 pips, representing a 77 percent relative difference.

Based on modelled spread differentials at 1 billion dollars of daily trading volume, the implied annualised cost differential approached 92.9 million dollars.

LMAX Group ultra fast, high quality market data with global institutional coverage

LMAX Group provides millisecond resolution order book data across global FX liquidity centres. With 1,000 price updates per second and transparent exchange execution, our data supports quantitative analysis of price discovery, liquidity resilience and volatility transmission.

This research is built on genuine institutional grade transaction data, enabling detailed modelling of lead lag behaviour, spread stability and execution cost during stress conditions.

Previous reports in this series include: