| ||

| 9th October 2025 | view in browser | ||

| Gold outshines fading dollar | ||

| The U.S. dollar has experienced a significant decline of over 10% since the start of the year. Meanwhile, gold’s rise above $4,000 per ounce reflects growing investor preference for it over the dollar, while expectations of U.S. rate cuts and a Trump administration favoring a weaker dollar add uncertainty. | ||

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

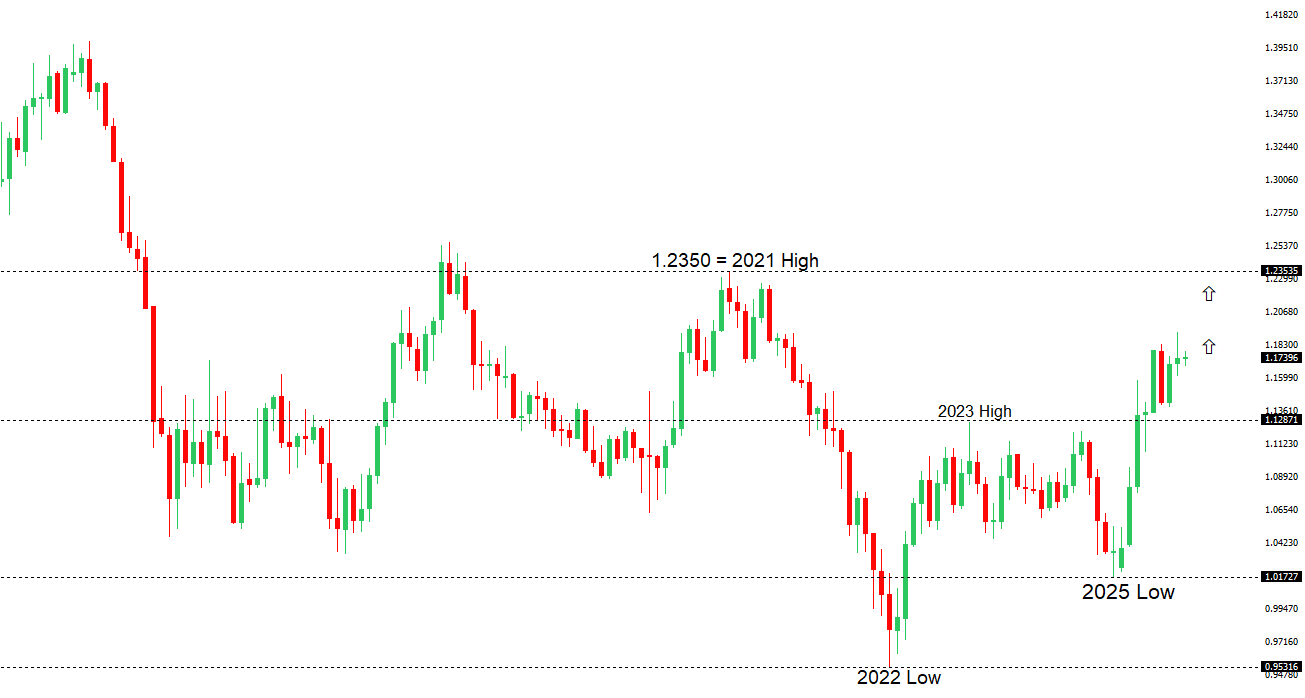

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1919 - 16 September/2025 high -Strong R1 1.1779 - 1 October high - Medium S1 1.1600 - Figure - Medium S2 1.1574 - 27 August low - Strong | ||

| EURUSD: fundamental overview | ||

| Germany’s industrial production dropped sharply by 4.3% in August, exceeding expectations of a 1.0% decline, driven by new U.S. tariffs, global uncertainty, and a significant 18.5% fall in automotive output. Factory orders hit a low not seen since 2012, and economists predict a bleak outlook for Europe’s largest economy due to weak demand and trade tensions, despite planned government investments. The European Central Bank is unlikely to cut rates soon, with policymakers like Escriva and Muller emphasizing flexibility and a stable 2% inflation target, while France’s political developments may help stabilize the euro. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 155.00. | ||

| ||

| R2 154.80 - 12 February high - Strong R1 153.00 - 8 October high - Medium S1 150.20 - 7 October low - Medium S2 149.03 - 6 October low - Strong | ||

| USDJPY: fundamental overview | ||

| Markets are betting on aggressive monetary and fiscal policies from Sanae Takaichi, pushing USDJPY higher, but her need for coalition support from centrist parties like Komeito may lead to a more moderate approach than anticipated. Public concerns over inflation and her appointment of experienced finance ministers suggest restrained stimulus plans, with markets watching her upcoming meeting with BOJ Governor Ueda for clues on policy alignment. Despite expectations, Japan’s steady wage growth supports the BOJ’s cautious tightening path, and Takaichi’s ambitious promises may face challenges, potentially tempering market optimism and yen weakness, though failure to secure coalition deals could exacerbate yen depreciation. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6707 - 17 September/2025 high - Strong R1 0.6660 - 18 September high - Medium S1 0.6556 - 8 October low - Medium S1 0.6520 - 26 September low - Strong | ||

| AUDUSD: fundamental overview | ||

| Markets have observed a shift toward a slower, more cautious monetary easing cycle from the Reserve Bank of Australia, reducing expectations for rapid rate cuts and supporting the Australian dollar in the near term. Most economists expect a 25-basis-point cut to 3.35% at the RBA’s November 4 meeting, though financial markets are less certain, with only a 37% chance priced in, reflecting concerns about rising inflation and a tight job market. Some economists and a hawkish minority even suggest a potential rate hike by mid-2026 if inflation persists. Meanwhile, Australia’s growing foreign reserves (A$107.1bn in September) and elevated consumer inflation expectations (4.8% in October) reinforce the RBA’s cautious stance, while a potential interest-rate gap with the U.S., where the Federal Reserve is expected to cut rates more aggressively, could push the Australian dollar to 70 US cents by mid-2026. | ||

| Suggested reading | ||

| Will Investors Need a Seatbelt This Month, or a Helmet?, M. Hulbert, MarketWatch (October 4, 2025) How AMD’s Own Stock Will Finance OpenAI’s Chip Buys, J. Bort, TechCrunch (October 7, 2025) | ||