| ||

| 3rd April 2026 | view in browser | ||

| Cautious markets eye volatile oil, thin NFP | ||

| The broader macro tone remains cautious amid ongoing Middle East developments, though occasional optimistic rhetoric has provided temporary relief and supported brief recoveries in risk sentiment. | ||

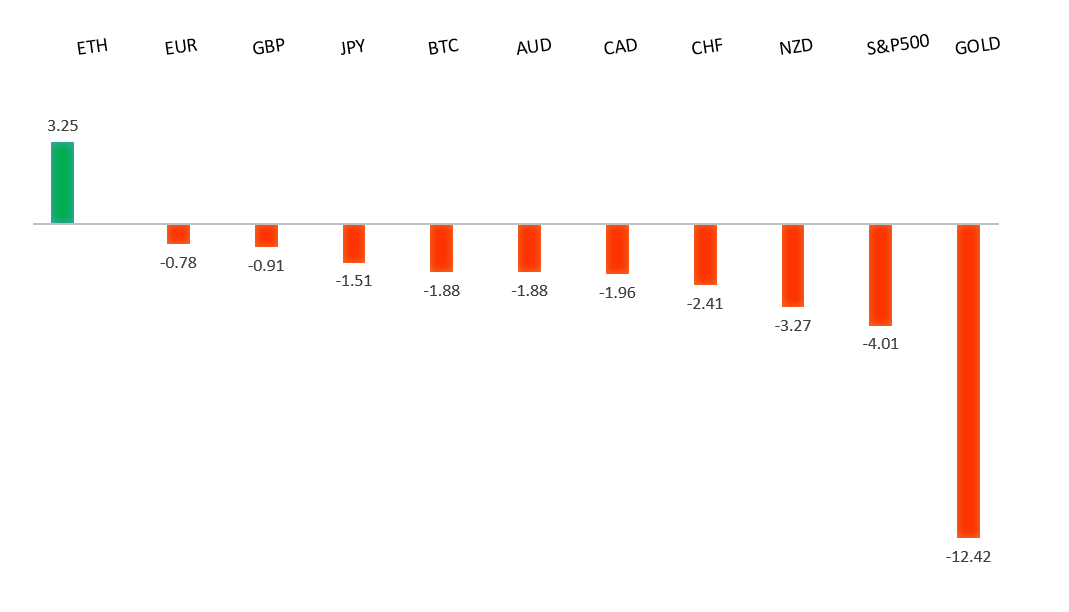

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1668 - 10 March high - Strong R1 1.1641 - 23 March high - Medium S1 1.1443 - 30 March low - Medium S2 1.1411 - 13 March/2026 low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has been supported over the past 24 hours primarily by a softer U.S. dollar backdrop, with markets reassessing Fed policy expectations after mixed U.S. data and cautious commentary around inflation risks. At the same time, improving risk sentiment—driven by easing geopolitical concerns—has reduced demand for the dollar as a safe haven, indirectly benefiting the single currency. On the European side, relatively stable data and a lack of dovish surprises from the European Central Bank have helped anchor rate expectations, while resilience in recent regional indicators continues to support the view that policy will remain restrictive for longer. Overall, the move has been less about euro-specific catalysts and more a function of shifting rate differentials and broader macro positioning. | ||

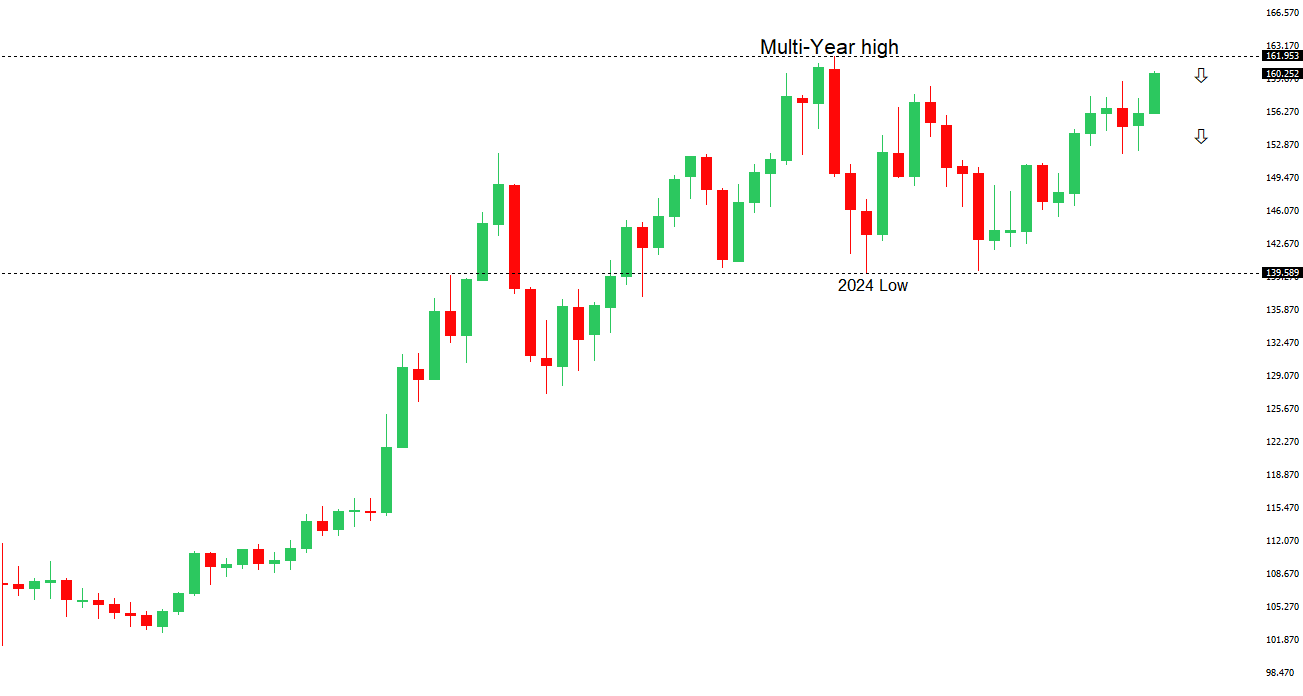

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 161.00 - Figure - Strong R1 160.46 - 30 March/2026 high - Medium S1 158.02 - 23 March low - Medium S2 157.51 - 19 March low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen has come under pressure amid a combination of external and policy-driven factors, with elevated oil prices on the back of Middle East tensions weighing on Japan’s terms of trade given its heavy reliance on energy imports. At the same time, persistent divergence in rate expectations continues to act as a headwind, with the Bank of Japan maintaining a cautious normalization path relative to other central banks, despite firmer domestic data and ongoing inflation concerns. While Japanese officials have reiterated warnings around excessive FX moves, markets remain unconvinced about the likelihood of imminent intervention, leaving the currency sensitive to broader yield differentials and shifts in global risk sentiment. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7188 - 11 March/2026 high - Strong R1 0.7000 - Psychological - Medium S1 0.6833 - 30 March low - Medium S2 0.6767 - 7 January high - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar has been supported by an improvement in global risk sentiment and a softer U.S. dollar backdrop, with easing geopolitical tensions helping to lift demand for higher-beta currencies. On the domestic side, relatively resilient data and stable expectations around the Reserve Bank of Australia have reinforced the view that policy will remain on hold for now, without a shift toward aggressive easing. At the same time, stronger signals out of China—Australia’s key trading partner—have provided an additional tailwind, particularly through the commodities channel, leaving the currency primarily driven by external growth expectations and broader macro positioning. | ||

| Suggested reading | ||

| What Are The Odds Of A Bear Market In 2026?, R. Detrick, Carson Group (April 1, 2026) AI, Tariffs, and Global Uncertainty, V. Katenelson, The Intellectual Investor (April 2, 2026) | ||