| ||

| 10th February 2026 | view in browser | ||

| Dollar pressure, Asia steady, Risk on | ||

| Global markets open with a risk-on, soft-dollar bias as easing US growth and policy credibility concerns, firmer JPY and CNY dynamics, and steady ECB and BOJ signaling reinforce a gradual shift away from US Dollar dominance toward selective FX strength and carry-friendly conditions. | ||

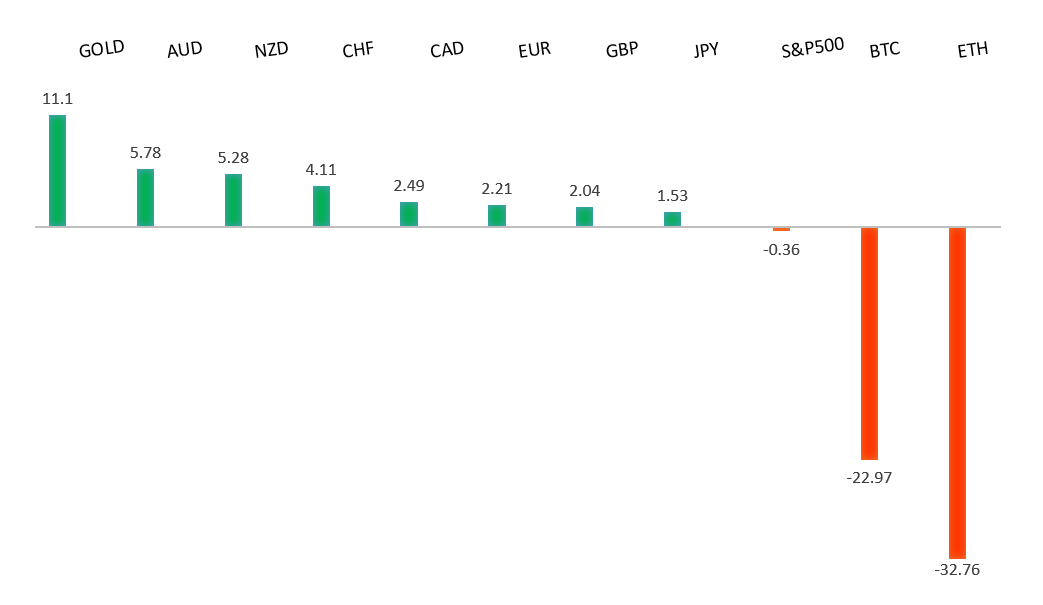

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

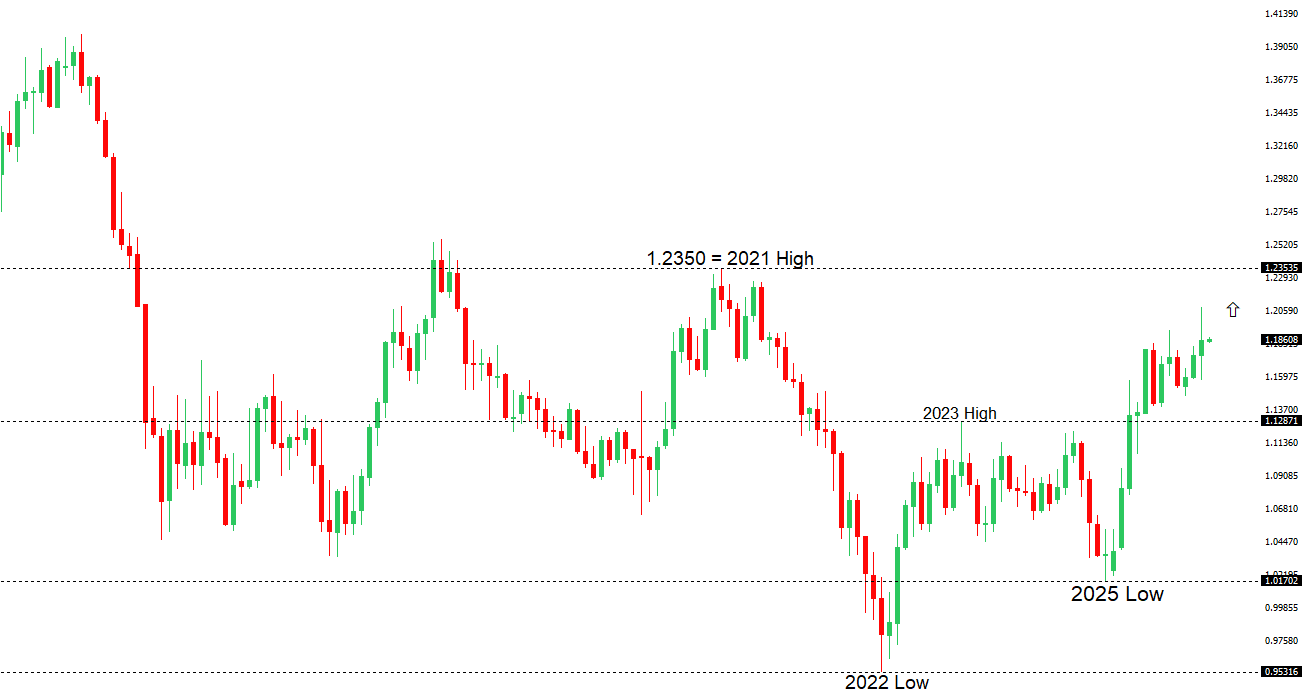

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1500. | ||

| ||

| R2 1.2083 - 27 Janaury/2026 high - Strong R1 1.1927 - 9 February high - Medium S1 1.1765 - 6 February low - Medium S2 1.1728 - 23 January low - Medium | ||

| EURUSD: fundamental overview | ||

| The euro was little changed, consolidating after Monday’s jump and holding near the late-January 4.5-year high. Recent ECB messaging has been notably calm, with President Lagarde and several Governing Council members downplaying the rise in the currency as “not dramatic,” stressing that the exchange rate is already baked into baseline forecasts and that inflation remains in a good place, leaving little appetite to push back against euro strength while it stays within recent ranges. Officials including Nagel and Kazimir have reinforced that view, signaling comfort with a temporary dip below the 2% inflation target in coming years and making clear that only a material deviation from the current outlook would justify a rate rethink, rather than modest euro-driven disinflation. Beyond near-term policy, Lagarde is also framing price stability within a broader EU push on competitiveness and resilience—highlighting initiatives such as a savings and investment union, a digital euro, and a deeper single market—which, alongside fiscal support in large economies like Germany, underpins a gradual medium-term growth story that many still see as structurally supportive for the euro. That said, CFTC data show speculative long positioning already stretched, leaving the currency vulnerable to sharper pullbacks if data or ECB communication were to challenge this steady baseline narrative. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. The recent break below 154.39 strengthens the outlook. | ||

| ||

| R2 158.00 - Figure - Medium R1 157.66 - 9 February high - Medium S1 154.55 - 2 February low - Medium S2 151.97 - 28 January/2026 low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen extended its rebound following Japan’s election, where the LDP and its allies secured a decisive super-majority, giving PM Takaichi a strong mandate to pursue a more activist but still measured policy agenda. While markets initially leaned into the so-called “Takaichi trade” — pricing a pro-growth mix of tax cuts, higher defense spending, rising JGB yields and firmer equities alongside renewed yen weakness — investor focus is now shifting to how far fiscal expansion can go without testing bond-market tolerance. Some banks see the stronger mandate accelerating BOJ normalization, pulling forward the first rate hike to as early as April and lifting terminal rate expectations, while others still favor a July move given the BOJ’s wage focus and caution around carry-trade risks. Near term, concerns around fiscal slippage keep USDJPY biased higher, with the 157–160 zone in focus as a potential intervention trigger, but medium-term dynamics look more constructive for the yen as political breathing room, gradual rate hikes and a BOJ normalizing on its own terms reduce the risk of entrenched, one-way weakness. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. Setbacks should now be well supported ahead of 0.6300. | ||

| ||

| R2 0.7158 - 2023 high - Strong R1 0.7099 - 9 February/2026 high - Strong S1 0.6897 - 6 February low - Medium S2 0.6834 - 23 January low - Medium | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar is modestly lower on the day and consolidating just below a near three-year high after Monday’s sharp rally, as investors weigh signs that domestic demand may be cooling faster than the RBA expected even with markets still pricing the cash rate close to 4.25% by year-end. December data released late Monday showed household spending fell 0.4%, well below expectations and reversing earlier strength, with weakness broad-based and more pronounced after adjusting for population growth, suggesting consumers ended 2025 on a softer footing. In contrast, the NAB’s January business confidence survey pointed to a more optimistic outlook, with confidence rising to its highest level since October, though this was tempered by a pullback in business conditions. While Governor Bullock has reiterated the RBA’s discomfort with inflation remaining above target and the need for demand to slow unless supply improves, the latest data hint the economy may already be losing momentum, potentially easing inflation pressures over time. Positioning data show speculators have increased net long AUD exposure, reflecting lingering optimism around relatively tight policy, but the currency remains highly sensitive to upcoming inflation, labor and wage data, where any renewed price pressure could quickly revive rate-hike expectations and push AUDUSD higher. | ||

| Suggested reading | ||

| How shopping chatbots might transform retail, C. Criddle, Financial Times (February 9, 2026) Warsh Will Soon Realize Powell Was Never Very Powerful, J. Tamny, Forbes (February 8, 2026) | ||