| ||

| 5th March 2026 | view in browser | ||

| Geopolitics keep USD supported, oil firm | ||

| The US dollar remains supported amid ongoing Middle East tensions as the Iran conflict enters day six, with oil firm, yields elevated on inflation concerns, equities slightly softer, central bank commentary in focus, and a busy global data calendar ahead while China signals a slower but more sustainable growth target. | ||

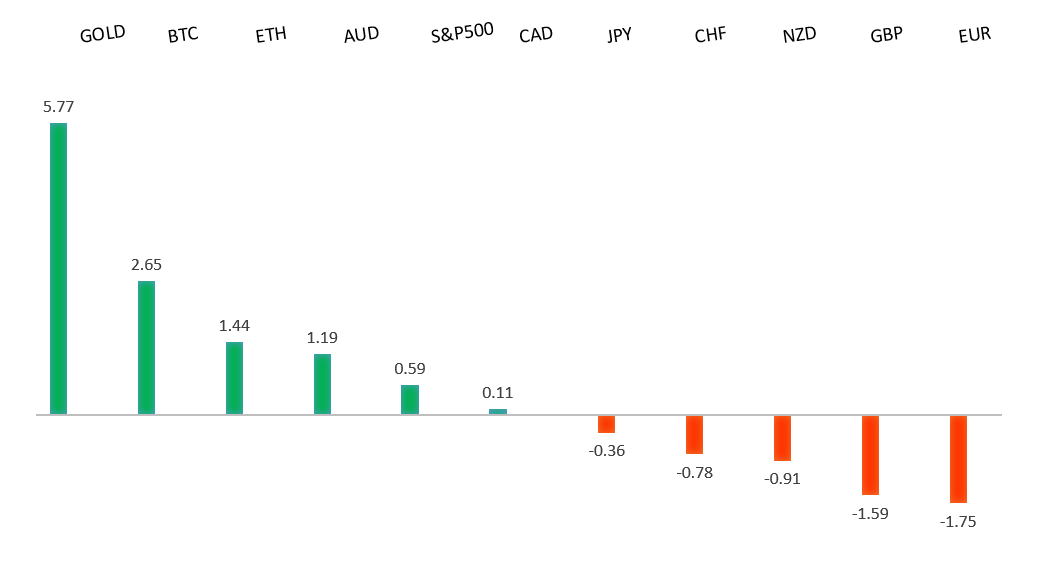

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

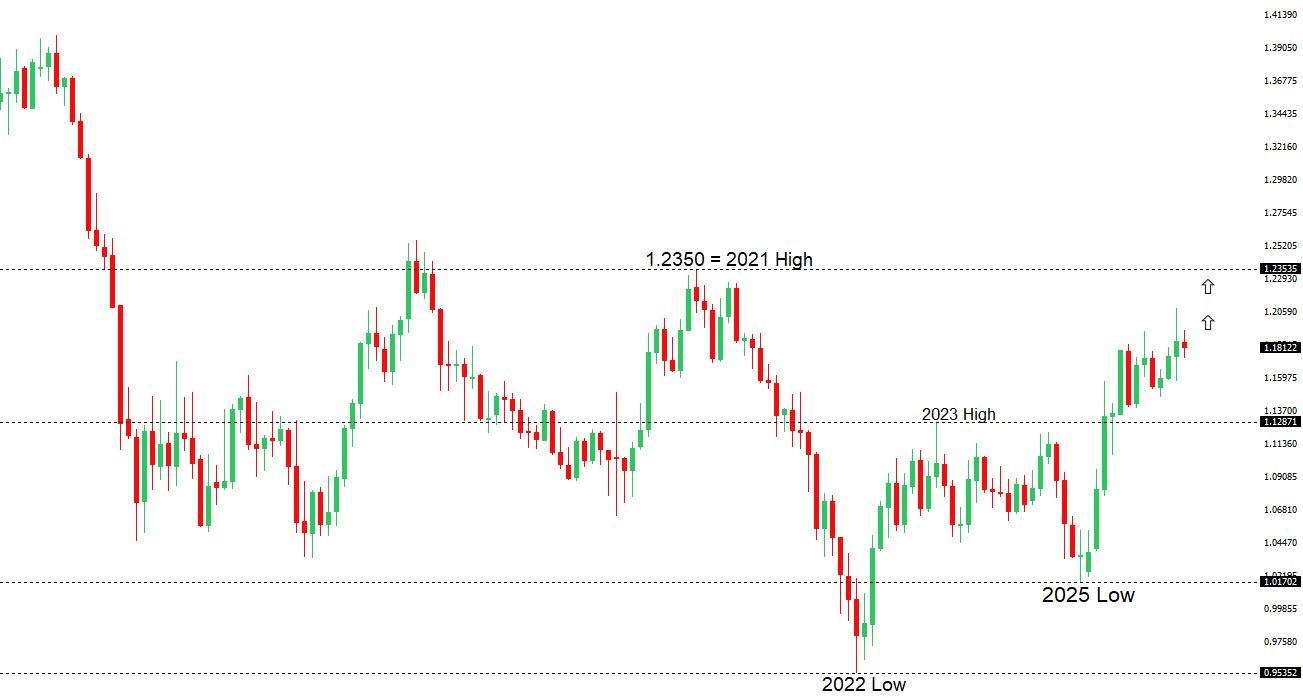

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1500. | ||

| ||

| R2 1.1835 - 23 February high - Strong R1 1.1707 - 3 March high - Medium S1 1.1575 - 4 March low - Medium S2 1.1530 - 3 March /2026 low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro remains under pressure after a sharp two-day drop erased the January rally, despite a modest bounce. The decline reflects a stagflation-style energy shock tied to the Iran conflict, which has driven oil and European gas prices sharply higher while euro-area inflation has already surprised to the upside. Because Europe is highly dependent on imported energy priced in dollars, rising fuel costs act as a direct economic “tax,” weakening the euro even as they complicate ECB policy by keeping inflation elevated and growth uncertain. As long as energy prices stay high and central banks remain cautious, the balance of risks still favors further downside. | ||

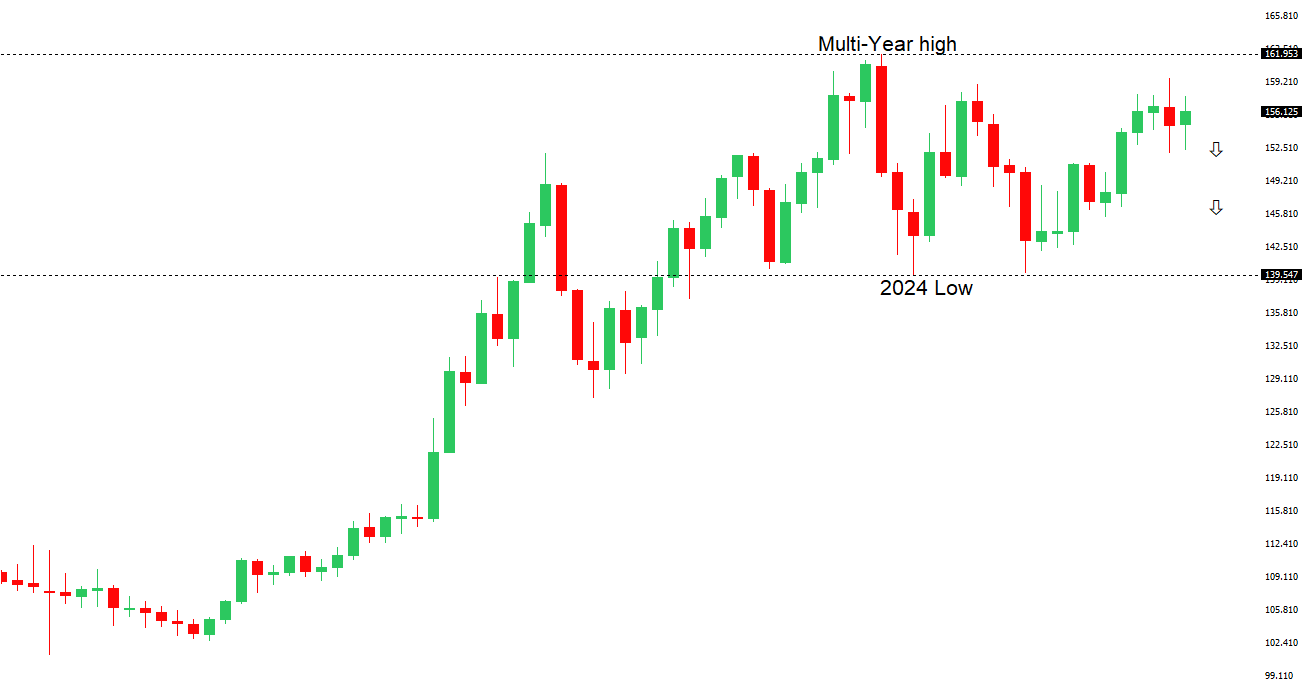

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. The recent break below 154.39 strengthens the outlook. | ||

| ||

| R2 159.46 - 14 January/2026 high - Strong R1 157.97 - 3 March high - Medium S1 155.34 - 25 February low - Medium S2 154.00 - 23 February low - Medium | ||

| USDJPY: fundamental overview | ||

| The yen is trying to hold onto recent gains on the back of concerns about potential intervention. Japan’s Finance Minister Katayama reiterated that both Japan and the US could take “decisive action” under the G7 stable currency framework, with recent rate-check activity reminding markets that coordinated signalling can quickly trigger a yen squeeze. Short-dated options show rising demand for yen protection, suggesting traders are hedging near-term event and intervention risk rather than positioning for a broader yen bull trend. While risk aversion and falling US Treasury yields could support the yen, the Bank of Japan is still cautious about tightening policy given global uncertainties, meaning a sustained JPY rally may require either deeper risk-off conditions or a disorderly move in USDJPY toward the 160 “danger zone.” | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7158 - 2023 high - Strong R1 0.7147 - 12 February/2026 high - Strong S1 0.6944 - 3 March low - Medium S2 0.6897 - 6 February low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar is under a little pressure, putting it on track to snap a six-week run of gains. January data was mixed, with the trade surplus narrowing to A$2.6b from A$3.4b as exports slipped 0.9%, while imports rose 0.8%, suggesting firmer domestic demand. Household spending rose 0.3% on the month but the annual pace of 4.6% came in below expectations. With Q4 GDP confirming solid economic momentum and steady private investment, dips toward the 0.69–0.70 area—particularly if driven by geopolitical headlines or yield swings—may offer opportunities to selectively accumulate AUD ahead of the mid-March RBA meeting, though escalating global growth concerns could still pressure the currency in the near term. | ||

| Suggested reading | ||

| A Sentiment Reaction, Not Catastrophe Prediction, Fisher Investments (March 3, 2026) U.S. Treasuries Failing Their Biggest Test In Decades, M. Hulbert, Marketwatch (March 2, 2026) | ||