| ||

| 24th March 2026 | view in browser | ||

| Investors cautious to start the new day | ||

| Oil’s rebound amid escalating Middle East tensions and uncertain diplomacy is driving a cautious, risk-off tone across markets, with softer global data and key macro releases now in focus. | ||

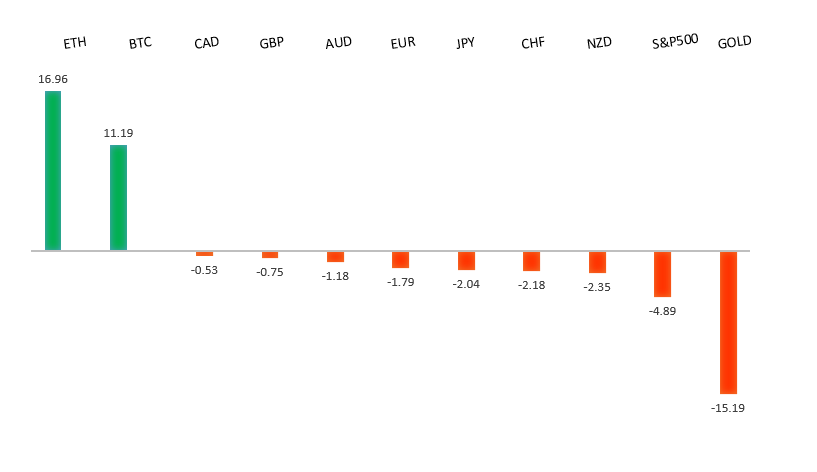

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1668 - 10 March high - Strong R1 1.1641 - 23 March high - Medium S1 1.1411 - 13 March/2026 low - Medium S2 1.1400 - Figure - Strong | ||

| EURUSD: fundamental overview | ||

| The euro is struggling to gain upside momentum as tensions in the Middle East—particularly the unresolved US-Iran conflict—push oil prices above $100, worsening the outlook for the eurozone. Rising energy costs risk adding to inflation while growth is already slowing, keeping the ECB cautious but increasingly hawkish beneath the surface, with markets now debating potential rate hikes as early as April or more likely June. While higher rate expectations offer some support to EURUSD, the currency remains vulnerable to further energy shocks and risk aversion, and is unlikely to rally meaningfully without clearer ECB tightening signals. Recent data also showed a decline in eurozone consumer confidence, highlighting the fragile backdrop. | ||

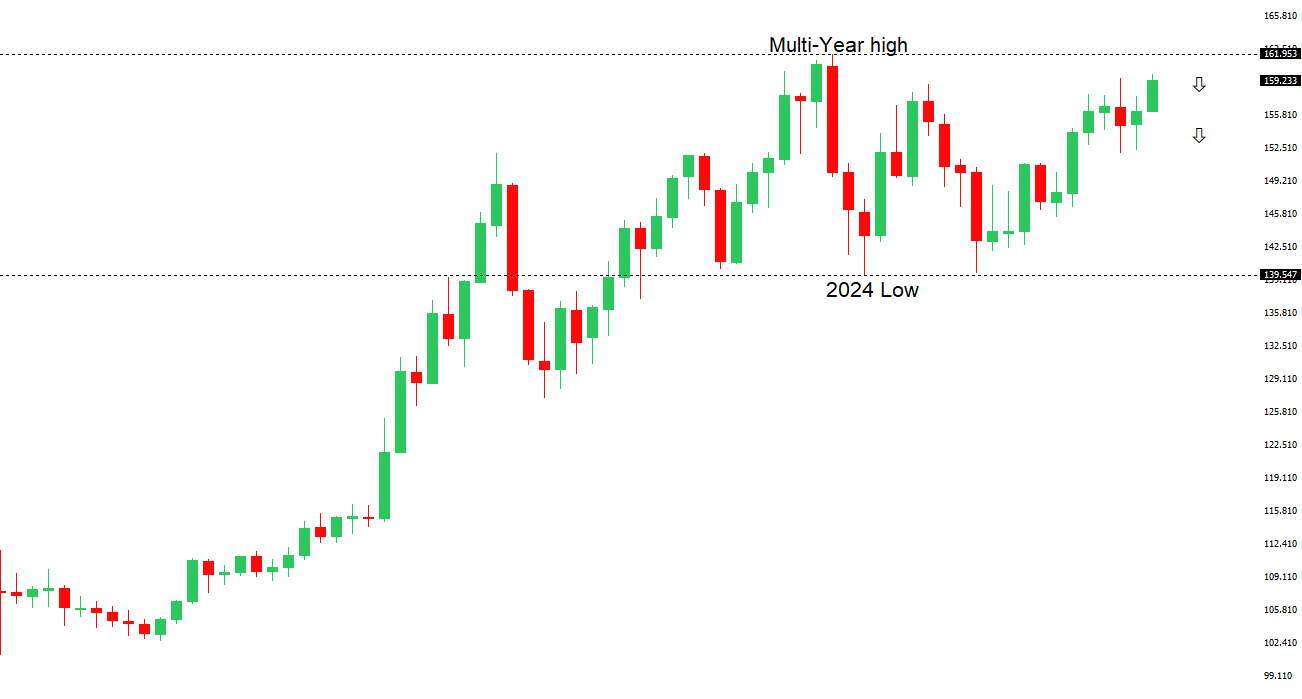

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 160.00 - Psychological - Strong R1 159.91 - 18 March/2026 high - Medium S1 157.27 - 10 March low - Medium S2 156.45 - 5 March low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen has managed to find only mild demand thus far, despite ongoing intervention warnings from officials. In the near term, the currency remains highly sensitive to headlines, as the Bank of Japan holds rates steady and waits to assess how geopolitical shocks—especially from the Middle East—impact inflation and growth. Elevated oil prices and Japan’s reliance on energy imports keep the bias tilted toward further yen weakness, though strong wage growth, persistent inflation, and the possibility of a rate hike should help prevent a deeper or sustained decline. Overall, expectations are for only modest yen recovery from current levels. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7200 - Figure - Medium R1 0.7188 - 11 March/2026 high - Medium S1 0.6910 - 23 March low - Medium S2 0.6897 - 6 February low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar is under pressure for a third day, driven by fading optimism around Middle East tensions and renewed USD strength. The outlook remains fragile as softer global growth and geopolitical risks threaten recent gains, though dips may find support from strong commodity prices and yields. Inflation is expected to stay elevated, with rising energy costs potentially complicating the RBA’s policy outlook despite signs of slowing economic activity. Recent PMI data confirms weakening momentum—especially in services—pointing to slower growth ahead, but persistent price pressures mean the RBA still faces a challenging balance. | ||

| Suggested reading | ||

| Invest If, When You Know Something Others Don’t, Fisher Investments (March 20, 2026) How Wealth For Generation X Compares by Age Group, K. Brockman, Motley Fool (March 19, 2026) | ||