| ||

| 6th March 2026 | view in browser | ||

| Payrolls, policy shifts and energy risks | ||

| Global markets enter the day focused on rising geopolitical and energy tensions around the Strait of Hormuz, new U.S. policy moves on AI chips and Iran, Trump’s nomination of Kevin Warsh as Fed Chair, and key data ahead including Eurozone GDP and a softer U.S. jobs report that could shape expectations for the Fed’s policy path. | ||

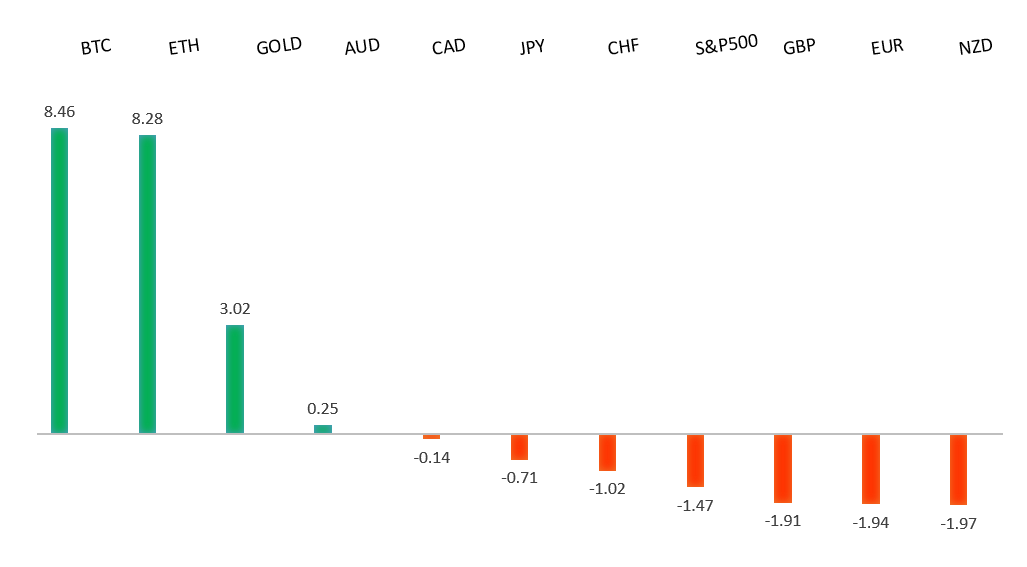

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

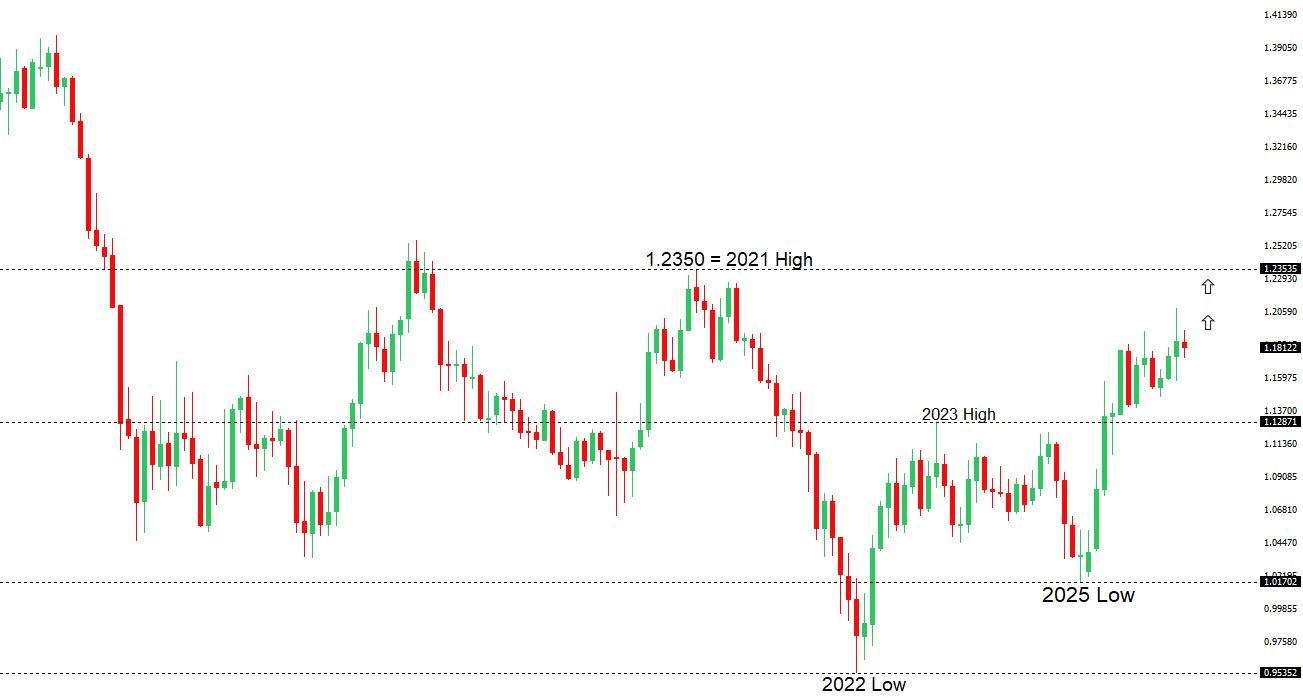

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1500. | ||

| ||

| R2 1.1835 - 23 February high - Strong R1 1.1707 - 3 March high - Medium S1 1.1575 - 4 March low - Medium S2 1.1530 - 3 March /2026 low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has fully reversed the January rally and has fallen about 1.7% this week. At the same time, the ECB increasingly sees the escalating US-Iran conflict as an upside risk to euro-area inflation through higher energy prices, though officials still view markets as orderly and are not signaling an immediate policy shift. Policymakers broadly suggest they will tolerate temporary energy spikes but could act if inflation expectations begin to drift, leaving near-term euro pricing more sensitive to energy and inflation-expectations data than to growth surprises. Meanwhile, the February ECB minutes confirmed a unanimous decision to hold rates near the 2% inflation target with “full optionality,” an outlook now being tested by rising geopolitical risks. | ||

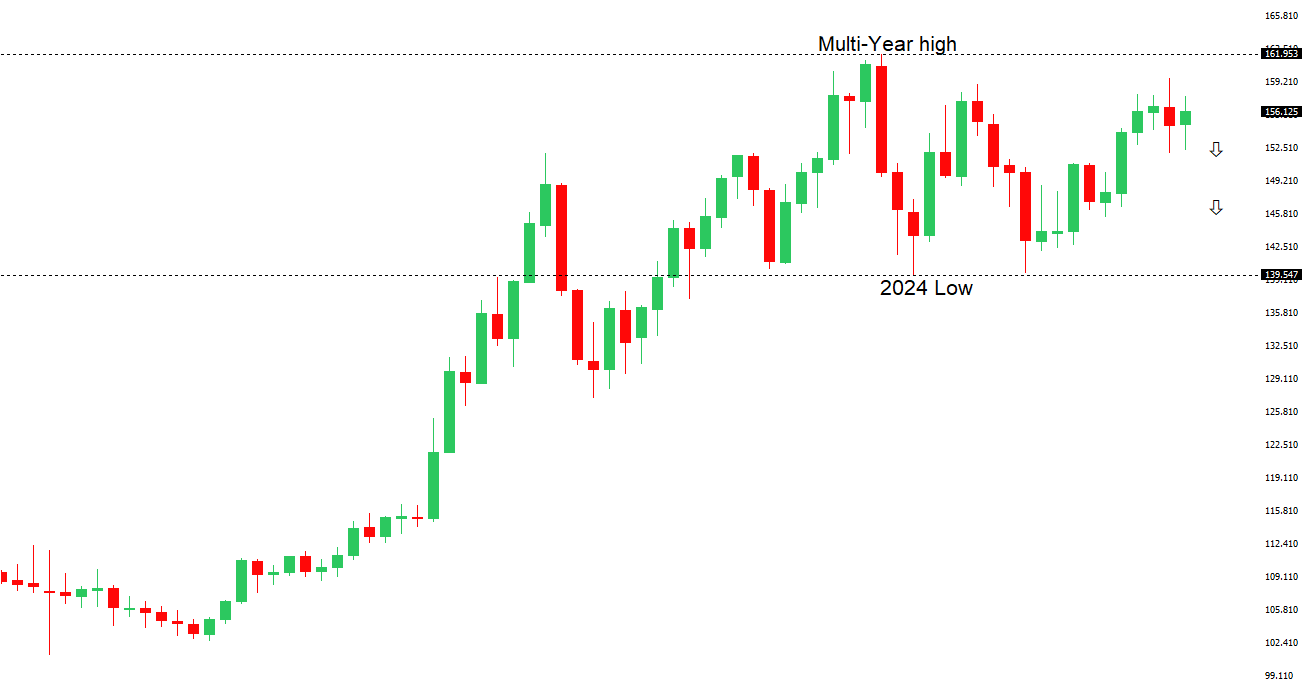

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. The recent break below 154.39 strengthens the outlook. | ||

| ||

| R2 159.46 - 14 January/2026 high - Strong R1 157.97 - 3 March high - Medium S1 155.34 - 25 February low - Medium S2 154.00 - 23 February low - Medium | ||

| USDJPY: fundamental overview | ||

| The yen traded mostly steady in Asia and is only modestly weaker against the dollar year-to-date, though renewed energy security concerns are emerging after Japan was warned of limited support to offset disruptions around the Strait of Hormuz. Given Japan’s heavy reliance on imported energy, higher fuel costs could complicate fiscal expansion plans and add to inflation pressures, with at least one refiner already cancelling March exports amid expectations of higher prices. USDJPY remains pulled between Japan’s energy vulnerability and the Fed-BOJ policy gap, versus safe-haven demand and the risk of official intervention if the yen weakens too quickly. Still, scope exists for yen strength if carry trades unwind and domestic yields rise, while ongoing wage growth and expectations of gradual BOJ tightening continue to support the medium-term outlook for the currency. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7158 - 2023 high - Strong R1 0.7147 - 12 February/2026 high - Strong S1 0.6944 - 3 March low - Medium S2 0.6897 - 6 February low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar is modestly bid today, recovering roughly half of Thursday’s near 1% drop, though it remains capped below 0.7100. Recent data point to a softer backdrop, with Australia’s January trade surplus narrowing to A$2.6b as exports fell and imports rebounded, while trade with China rose sharply, highlighting Australia’s heavy reliance on China even as the surplus with its largest partner shrinks. Domestically, a modest 0.3% rebound in January consumption—driven mostly by services and essentials—signals cautious households, suggesting demand momentum is cooling and raising the bar for further RBA tightening despite February’s rate hike. | ||

| Suggested reading | ||

| Why Japan’s Bond Market Matters To The US Economy, D. Lachman, AEIdeas (March 3, 2026) On AI Eating The World, V. Katsenelson, The Intellectual Investor (March 5, 2026) | ||