| ||

| 22nd July 2025 | view in browser | ||

| Trade tensions and Fed scrutiny hit dollar | ||

| The US Dollar got off to a soft start to the week, though thinner summer trading conditions have restrained activity across G10 and emerging markets | ||

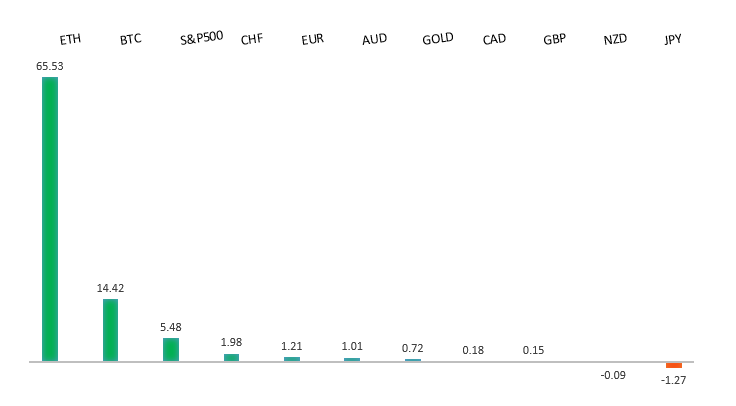

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1000. | ||

| ||

| R2 1.1800 - Figure - Medium R1 1.1722 - 16 July high - Medium S1 1.1557 - 17 July low - Medium S2 1.1446 - 19 June low - Strong | ||

| EURUSD: fundamental overview | ||

| ECB President Lagarde expressed confidence in managing inflation from over 10% in 2022 without triggering a eurozone recession, with the ECB expected to maintain its 2% deposit rate at Thursday’s meeting. Despite President Trump’s threatened 30% tariffs on EU imports, which could slow growth and inflation if exceeding 10%, the ECB is likely to hold off on immediate action, possibly signaling a September rate cut if risks intensify. Markets anticipate the ECB’s next cut may be its last this cycle, while expecting more Fed cuts, boosting EURUSD optimism. The ECB’s bank lending survey, upcoming PMI data, and Germany’s IFO index will provide insights into tariff impacts, as the EU, led by countries like Germany, prepares potential “anti-coercion” countermeasures against the U.S. if trade talks fail. Meanwhile, the Kremlin supports new Ukraine peace talks, but significant diplomatic gaps remain. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 152.00. | ||

| ||

| R2 150.00 - Psychological - Strong R1 149.19 - 16 July high - Medium S1 146.91 - 16 July low - Medium S2 145.75 - 10 July low - Strong | ||

| USDJPY: fundamental overview | ||

| Japanese Prime Minister Shigeru Ishiba faces growing pressure after his coalition’s loss of its upper house majority, potentially complicating U.S.-Japan trade talks and increasing calls for his resignation if he fails to prevent steep U.S. auto tariffs. The yen weakened as expected, with markets having anticipated the coalition’s defeat, but the USDJPY rise is likely capped as focus shifts to coalition negotiations and ongoing trade discussions. The Bank of Japan’s monetary normalization faces hurdles due to political pressure for fiscal stimulus, though sustained wage growth and firm inflation expectations should keep gradual normalization on track. However, yen bullish factors, like a swift U.S.-Japan trade deal or BOJ policy progress, now face higher obstacles, potentially fueling further yen weakness if bond market volatility prompts BOJ adjustments. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6596 - 11 July/2025 high - Strong R1 0.6555 - 16 July high - Medium S1 0.6454 - 17 July low - Medium S1 0.6373 - 23 June low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar weakened slightly against the US dollar, after the Reserve Bank of Australia minutes revealed a cautious approach to further interest rate cuts, emphasizing a “gradual” easing strategy. The RBA is awaiting confirmation that inflation will sustainably hit its target, with next week’s Q2 CPI data and updated staff forecasts critical for its August 12 meeting. Attention now turns to RBA Governor Bullock’s upcoming speech, especially after June’s unexpected unemployment rise to 4.3%. | ||

| Suggested reading | ||

| Why I’m moving to Abu Dhabi, S. McBride, RiskHedge (July 18, 2025) Kevin Hassett Wants To Be Fed Chairman, J. Tamny Forbes (July 20, 2025) | ||