| ||

| 25th July 2025 | view in browser | ||

| Dollar firms as Fed drama simmers | ||

| Markets remain on edge amid growing speculation that a political risk event could unfold, tied to President Trump escalating his campaign to remove Fed Chair Powell. The absence of the usual Fed criticism from both Trump and Treasury Secretary Bessent today may have supported a modest bounce in the dollar and weighed on Treasuries. | ||

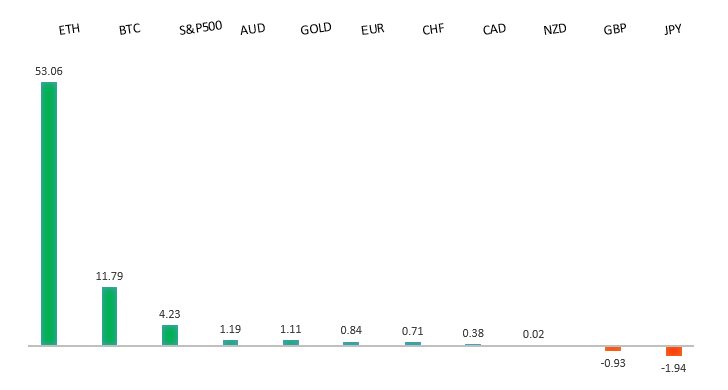

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1000. | ||

| ||

| R2 1.1830 - 1 July/2025 high - Strong R1 1.1789 - 24 July high - Medium S1 1.1557 - 17 July low - Medium S2 1.1446 - 19 June low - Strong | ||

| EURUSD: fundamental overview | ||

| The European Central Bank kept its deposit rate at 2% as expected, awaiting clarity on US-Euro trade talks and offering no hints on future rate moves due to uncertain tariff outcomes. Eurozone economic data shows growing momentum, with the Composite PMI rising to 51.0 in July, driven by stronger manufacturing and services sectors, alongside robust Q1 2025 GDP growth of 0.6%. Analysts suggest the ECB may pause rate cuts longer than anticipated, with some predicting a shift toward rate hikes if inflation rises and trade uncertainties ease. A potential 15% US-EU tariff deal could strengthen the euro by reducing economic risks, potentially pushing the Euro toward 1.1900–1.2000, especially if US rate cut expectations grow. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 152.00. | ||

| ||

| R2 150.00 - Psychological - Strong R1 149.19 - 16 July high - Medium S1 146.11 - 23 July low - Medium S2 145.85 - 24 July low - Strong | ||

| USDJPY: fundamental overview | ||

| The Bank of Japan’s Deputy Governor Shinichi Uchida noted that a US trade deal has reduced economic uncertainty, boosting market optimism for potential rate hikes, though USDJPY weakened. Persistent inflation, with Tokyo’s July CPI at 2.9% and core measures steady at 3.1%, supports the BOJ’s policy normalization, but political uncertainty following the LDP’s electoral setback and potential leadership change could impact monetary policy. A possible shift to Sanae Takaichi as PM, who favors monetary easing and a weaker yen, might pressure the BOJ to delay rate hikes, while proposed consumption tax cuts could raise bond yields and further weaken the yen. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6688 - 7 November 2024 high - Strong R1 0.6625 - 24 July/2025 high - Medium S1 0.6454 - 17 July low - Medium S1 0.6373 - 23 June low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian Dollar gained strength due to improved market optimism following a US-Japan trade deal, raising hopes for similar agreements with Europe and China. RBA Governor Michele Bullock’s recent comments reduced expectations for aggressive rate cuts, emphasizing a resilient labor market despite a rise in unemployment to 4.3% in June, which aligns with RBA forecasts. She highlighted that inflation is gradually approaching the 2.5% target, though the upcoming Q1 core inflation may be slightly below the expected 2.6%, and cautioned against overreacting to single data points. Bullock’s hawkish stance, noting the RBA’s restrained rate hikes in 2022-2023, led to higher Australian bond yields and a stronger AUD, with markets now less certain about an August rate cut and scaling back expectations for consecutive cuts without clearer signs of economic slowdown. | ||

| Suggested reading | ||

| Germany’s spending gamble, D. Garahan, Financial Times (July 24, 2025) Active Investing Is A Loser’s Game, L. Swedroe, Morningstar (July 23, 2025) | ||