| ||

| 29th July 2025 | view in browser | ||

| US-EU trade deal shakes markets, Dollar surges | ||

| Financial markets have kicked off the week contending with what has been a significant US-EU trade deal. This deal has been behind a third consecutive day of US dollar strength against major currencies, particularly the Euro. | ||

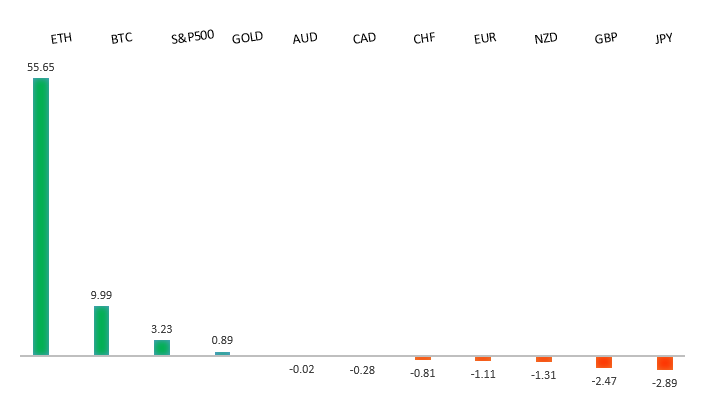

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1000. | ||

| ||

| R2 1.1789 - 24 July high - Medium R1 1.1700 - Figure - Medium S1 1.1557 - 17 July low - Medium S2 1.1446 - 19 June low - Strong | ||

| EURUSD: fundamental overview | ||

| EU officials, initially aiming for a tariff-free trade deal with the US, settled for a 15% tariff rate, higher than the anticipated 10%, and made additional concessions. Lacking critical exports like rare earths, the EU, which mainly exports luxury goods, faced a weaker bargaining position, potentially pushing Europe to hasten economic reforms and diversify trade partners. The 15% tariff is unlikely to significantly disrupt EU growth or inflation, with the ECB maintaining its 2% deposit rate and viewing any inflation dip as temporary. While the euro weakened due to the lopsided deal, markets may soon focus on the EU avoiding a worse outcome, with expectations of divergent US and EU monetary policies influencing currency trends in the near term. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 152.00. | ||

| ||

| R2 150.00 - Psychological - Strong R1 149.19 - 16 July high - Medium S1 146.81 - 25 July low - Medium S2 145.85 - 24 July low - Strong | ||

| USDJPY: fundamental overview | ||

| Despite the US-Japan trade deal, Prime Minister Ishiba’s position remains shaky due to the LDP minority status in both houses, with growing internal pressure for his resignation. If Ishiba steps down, Shinjiro Koizumi and Sanae Takaichi are leading contenders for LDP leadership; Koizumi supports the Bank of Japan’s independence, while Takaichi favors monetary easing and could resist BOJ rate hikes. The BOJ is expected to hold rates steady at its upcoming meeting, with markets focused on its inflation outlook and hints of future rate hikes, though a new “risk management approach” may justify caution despite strong inflation trends. June retail sales, industrial production, and housing data, particularly retail sales showing consumer strength, will influence yen trading before the BOJ meeting. | ||

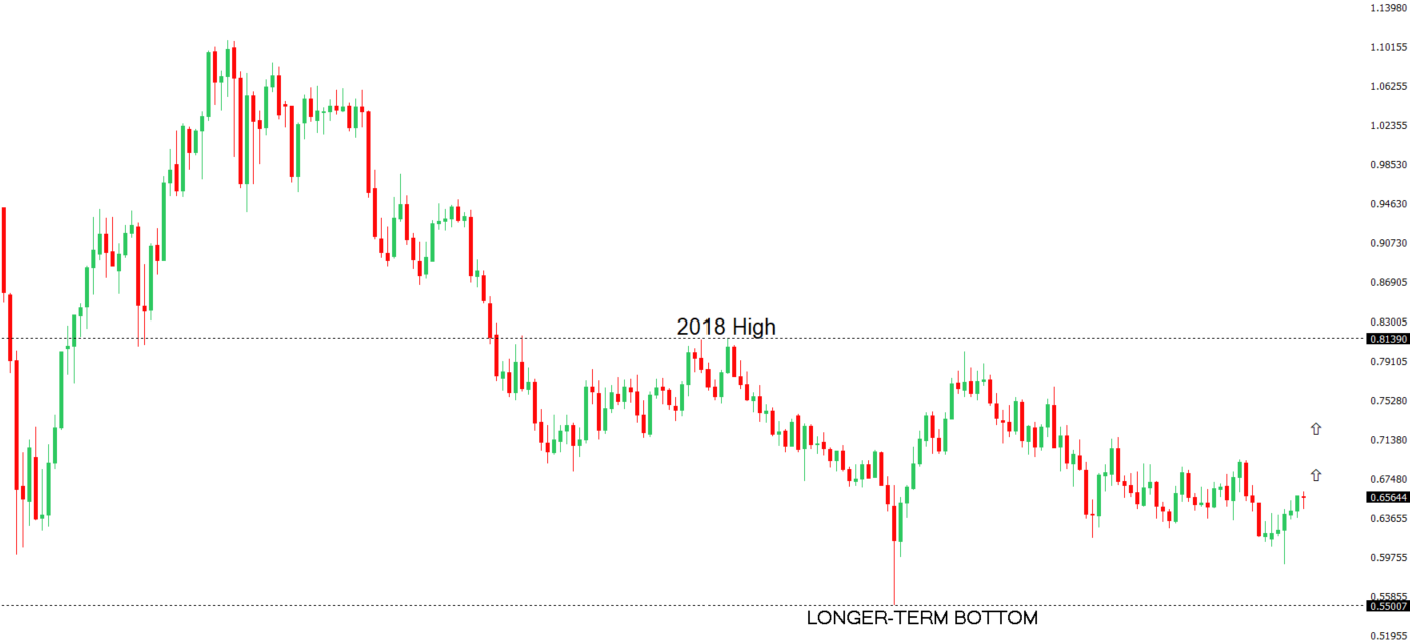

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6688 - 7 November 2024 high - Strong R1 0.6625 - 24 July/2025 high - Medium S1 0.6454 - 17 July low - Medium S1 0.6373 - 23 June low - Strong | ||

| AUDUSD: fundamental overview | ||

| The market is focused on the upcoming FOMC meeting, where the Federal Reserve is expected to maintain a cautious, data-driven stance, boosting the U.S. dollar against other G10 currencies. Australian super funds, managing a A$4.1 trillion asset base, are reassessing U.S. investments and increasing AUD hedging to mitigate potential declines in the AUDUSD exchange rate. Australia’s Q2 CPI, due July 30, is projected to show inflation easing to 2.2% YoY, potentially prompting an RBA rate cut in August, though Governor Bullock’s recent hawkish remarks suggest a slower approach to rate cuts, supported by a stable labor market and slightly lower-than-expected core inflation. While markets still anticipate an August cut, expectations for aggressive, consecutive cuts have waned, with two cuts projected by year-end, likely in August and November. | ||

| Suggested reading | ||

| Bernanke & Yellen’s Inflation Mystification Ails Fed, J. Tamny, Forbes (July 27, 2025) Quantitative Ranking of Federal Reserve Chairs, J. Divine, US News & World Report (July 24, 2025) | ||