| ||

| 31st July 2025 | view in browser | ||

| Dollar surges on strong data, hawkish Fed | ||

| The U.S. dollar strengthened for a fifth consecutive day on Wednesday, driven by robust U.S. GDP and employment data, which prompted investors to abandon bearish dollar positions. | ||

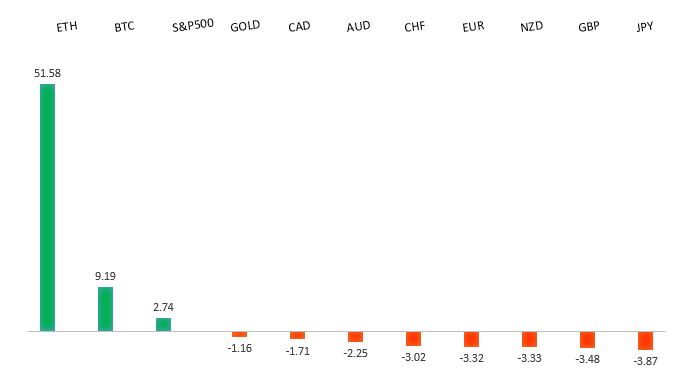

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1000. | ||

| ||

| R2 1.1600 - 29 July high - Medium R1 1.1500 - Figure - Medium S1 1.1313 - 30 May low - Medium S2 1.1210 - 29 May low - Strong | ||

| EURUSD: fundamental overview | ||

| After the FOMC meeting and strong US economic data, G10 currencies weakened against the dollar, with the euro stabilizing after a sharp sell-off pushed its RSI into oversold territory. The euro area economy grew by 0.1% in Q2, beating expectations but masking weaknesses in Germany and Italy, further pressured by new US-EU trade tariffs that could reduce GDP by 0.3-0.5%. Euro zone wage growth is projected to slow to 2.6% in Q1 2026, down from 3.1% in Q4 2025, raising concerns about undershooting the ECB’s 2% inflation target. Despite these challenges, the ECB remains cautious about further rate cuts, preferring to monitor economic developments before acting. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 152.00. | ||

| ||

| R2 150.00 - Psychological - Strong R1 149.50 - 30 July high - Medium S1 146.81 - 25 July low - Medium S2 145.85 - 24 July low - Strong | ||

| USDJPY: fundamental overview | ||

| With the U.S. economy showing resilience and strengthening the dollar, attention turns to the upcoming Bank of Japan meeting, where rates are expected to remain steady while the BOJ may raise its inflation outlook. Despite recent data showing robust retail sales and industrial production, indicating economic momentum, the BOJ’s cautious “risk management approach” could signal no immediate rate hikes, potentially weakening the yen if markets perceive a dovish stance. Suntory Holdings CEO Takeshi Ninami urges the BOJ to raise rates to counter yen weakness and inflation pressures impacting daily life in Japan. | ||

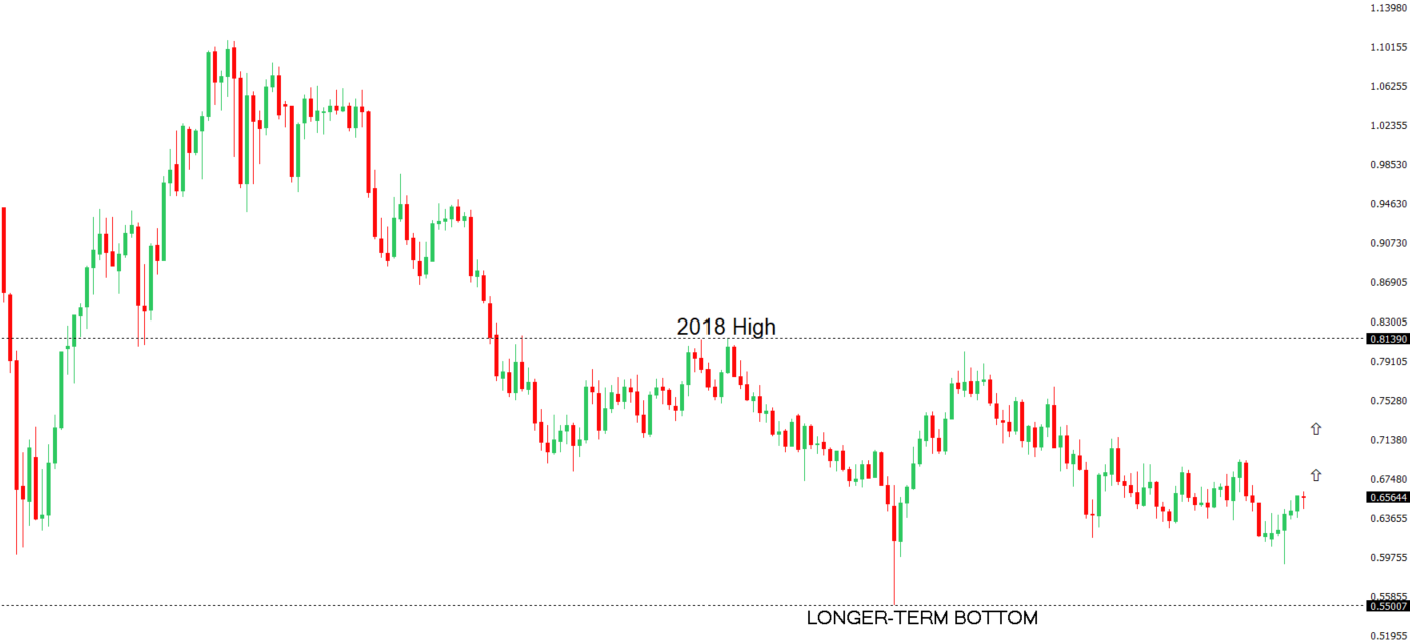

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6688 - 7 November 2024 high - Strong R1 0.6625 - 24 July/2025 high - Medium S1 0.6426 - 30 July low - Medium S1 0.6373 - 23 June low - Strong | ||

| AUDUSD: fundamental overview | ||

| Chinese trade negotiator Li Chenggang announced an extension of the US-China trade truce in Stockholm, though US Treasury Secretary Bessent noted that final approval from Trump is pending due to unresolved technical details. No major agreements were confirmed, but both sides appear committed to avoiding escalation, keeping future trade deal possibilities open. Meanwhile, China’s massive Yarlung Zangbo dam project could boost demand for heavy equipment and commodities like steel and cement, potentially benefiting Australia’s economy due to its iron ore exports. Australia’s Q2 CPI data came in below expectations at 0.7% QoQ and 2.1% YoY, supporting expectations for a 25bps rate cut by the RBA in August, with economists noting that inflation is under control and monetary policy may ease further. | ||

| Suggested reading | ||

| What Is Driving Inflation?, B. Ritholz, The Big Picture (July 29, 2025) Busting Three Myths, R. Detrick, Carson (July 29, 2025) | ||