| ||

| 18th September 2025 | view in browser | ||

| Powell’s “Insurance Cut” Dims Hopes for Aggressive Easing | ||

| The Federal Reserve cut interest rates by a quarter of a percentage point, its first reduction in nine months, prompted by signs of a weakening job market despite persistent inflation above the 2% target. Fed Chair Jerome Powell described the move as an “insurance cut,” signaling caution rather than the start of aggressive easing, which tempered initial market optimism and led to rising Treasury yields and a stronger dollar. | ||

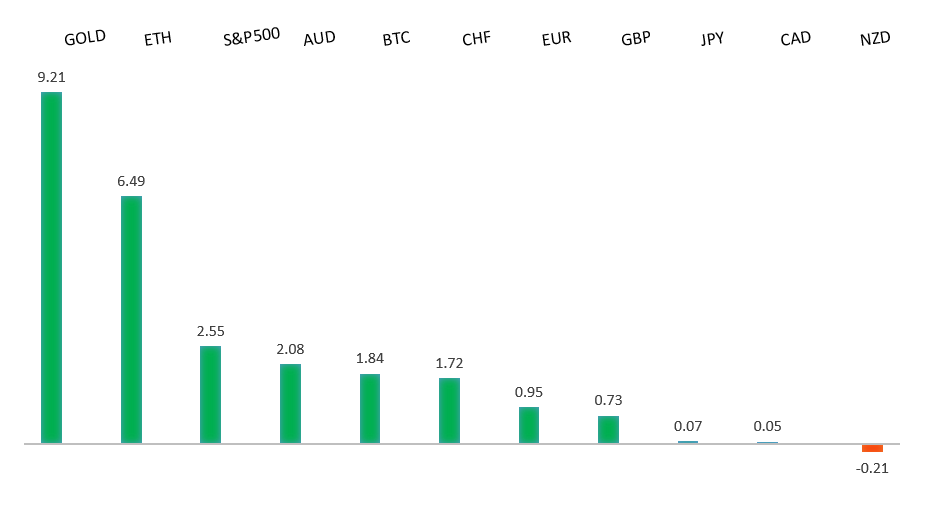

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

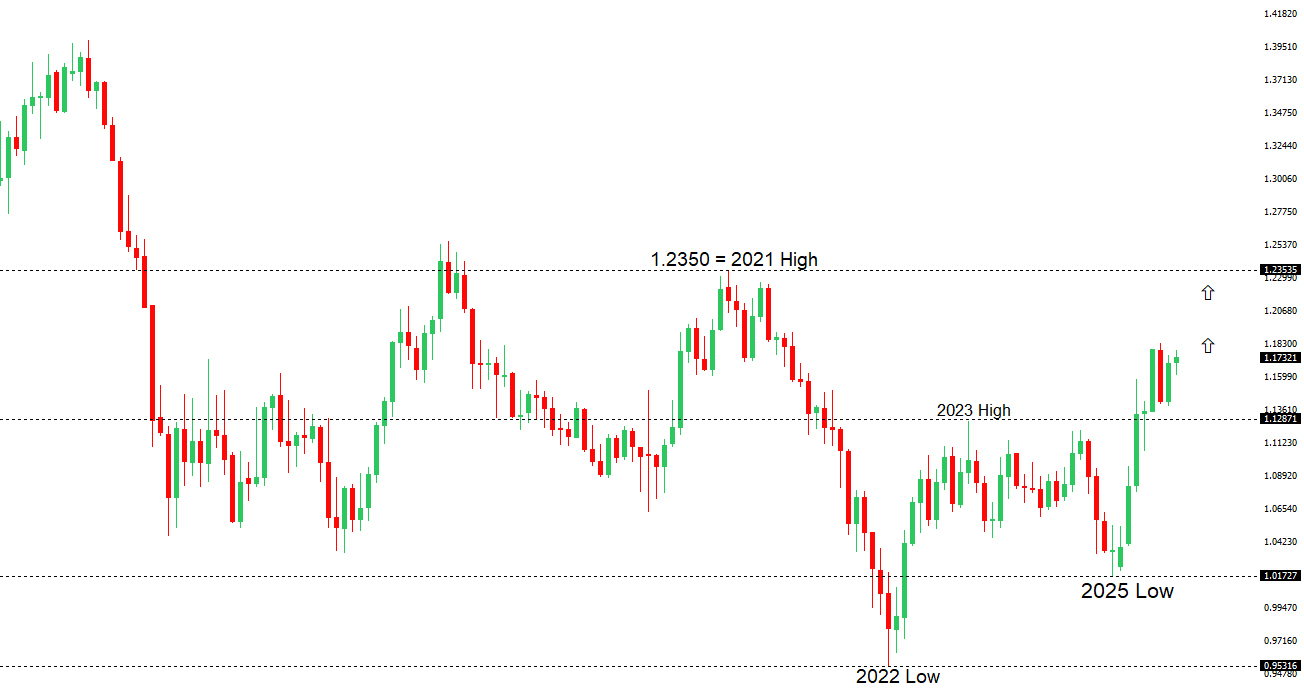

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.2000 - Psychological - Strong R1 1.1919 - 16 September/2025 high - Medium S1 1.1758 - 16 September low - Medium S2 1.1660 - 11 September low - Medium | ||

| EURUSD: fundamental overview | ||

| The Euro dipped from a four-year high of 1.1919 after the Federal Reserve met expectations with a 25bps rate cut and signaled two more cuts in 2025, triggering a “sell the news” reaction, though the broader uptrend from the February 2025 low of 1.0141 is expected to resume. Eurozone inflation remains sticky, with August CPI at 2.0% and core inflation steady at 2.3%, aligning with the ECB’s target but raising concerns among hawkish ECB officials who see rate hikes, possibly by June 2026, as more likely than further cuts unless economic data weakens. This divergence between the ECB and Fed, alongside persistent inflation and potential U.S. tariff impacts, supports a bullish Euro outlook. | ||

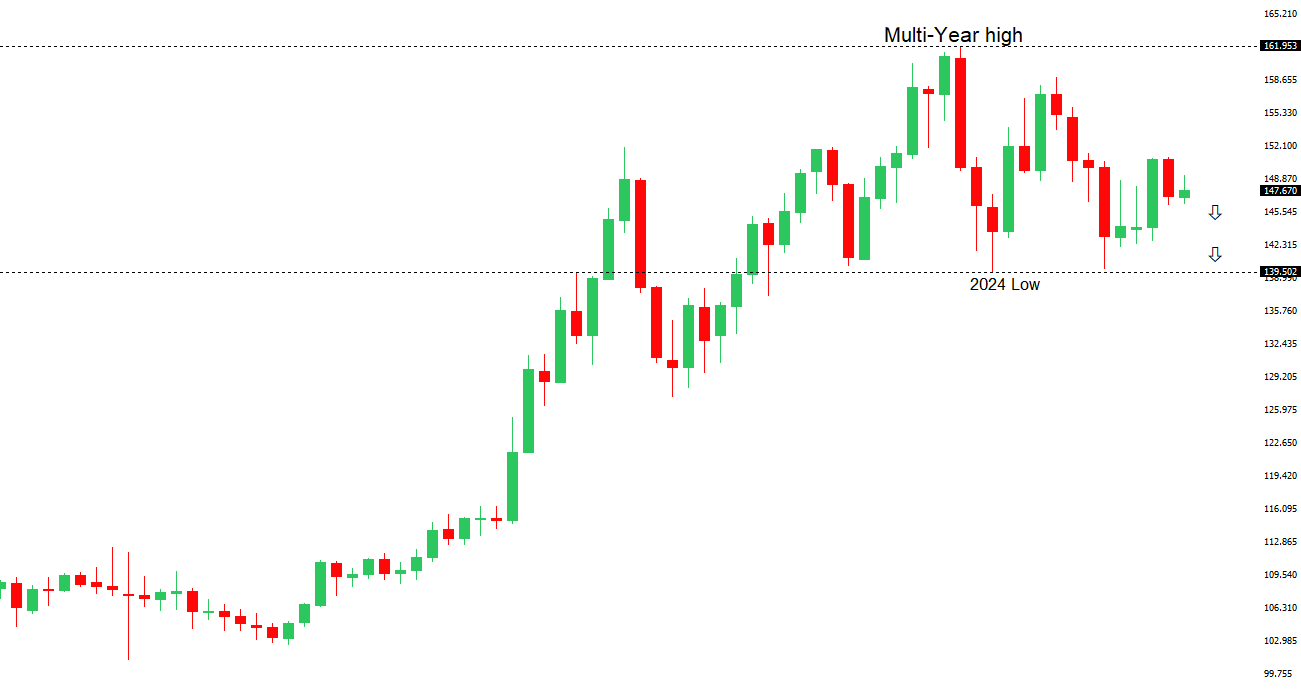

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 152.00. | ||

| ||

| R2 150.92 - 1 August high - Strong R1 149.14 - 3 September high - Medium S1 146.28 - 16 September low - Medium S2 145.48 - 17 September low - Strong | ||

| USDJPY: fundamental overview | ||

| The Bank of Japan is likely to keep its benchmark interest rate at 0.5% this Friday, awaiting clarity on Japan’s political leadership following Ishiba’s resignation, which has weakened investor confidence and the yen. Despite political uncertainty, steady economic growth, rising wages, and reduced U.S.-Japan trade risks support expectations for a potential BOJ rate hike to 0.75% by October or December, with a Bloomberg survey favoring January at the latest. A possible win by Shinjiro Koizumi in the Liberal Democratic Party leadership race could bolster BOJ’s tightening plans, potentially strengthening the yen, while a Sanae Takaichi victory might weaken it due to her support for continued easing. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6707 - 17 September/2025 high - Strong R1 0.6700 - Figure - Medium S1 0.6580 - 10 September low - Medium S1 0.6483 - 2 September low - Medium | ||

| AUDUSD: fundamental overview | ||

| The U.S. dollar has stabilized after a 25bps Federal Reserve rate cut aligned with market expectations, but risks of further weakening persist due to soft U.S. labor data, shifting central bank rate expectations, and concerns over Fed independence. In Australia, the Reserve Bank of Australia is nearing its 2–3% inflation target while maintaining full employment, with rates likely to stay at 3.6% and potential cuts eyed for November and early 2026, supported by improving consumer demand and lending. However, recent labor data shows a cooling job market, with a surprising 5,400 job loss in August, driven by a 40,900 drop in full-time positions, signaling weaker labor demand and potential risks to consumer spending. Meanwhile, Australia’s superannuation funds are increasing overseas investments and currency hedging, which could support the Australian dollar but introduces new risks if market volatility rises. | ||

| Suggested reading | ||

| Recall Me Maybe | FT Drama, D. Baddiel, Financial Times (September 17, 2025) Why the Federal Reserve’s Cut May Not Boost Economy, M. Hulbert, MarketWatch (September 17, 2025) | ||