| ||

| 30th September 2025 | view in browser | ||

| Jobs report, tariffs, and shutdown fears pressure dollar | ||

| The U.S. dollar has shown signs of recovery due to resilient economic data and the Federal Reserve’s cautious approach to further rate cuts, but its broader downward trend persists, with technical indicators suggesting limited upward momentum. | ||

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1919 - 16 September/2025 high -Strong R1 1.1820 - 23 September high - Medium S1 1.1646 - 25 September low - Medium S2 1.1574 - 27 August low - Strong | ||

| EURUSD: fundamental overview | ||

| This week, key Eurozone data includes September’s flash CPI, August’s unemployment rate, and August’s PPI numbers, with Germany’s inflation and unemployment figures also in focus. The Euro has risen after Spanish inflation increased to 3.0% in September, hinting at broader Eurozone inflation rising to 2.2%, which may discourage further ECB interest rate cuts and support euro bulls. ECB Chief Economist Philip Lane sees no major inflation risks, suggesting stable rates, while some economists predict the ECB will maintain its 2.00% deposit rate through 2026, though a small cut remains possible. Despite hawkish ECB views, potential trade uncertainties and economic weaknesses could revive dovish policies. Germany’s stable 6.3% unemployment and 2.2%-2.3% inflation rates reflect persistent price pressures, driven by food prices and easing energy deflation. Long-term, ECB caution contrasts with expected aggressive Fed rate cuts, supporting EUR strength, alongside Germany’s reforms boosting Eurozone growth prospects. | ||

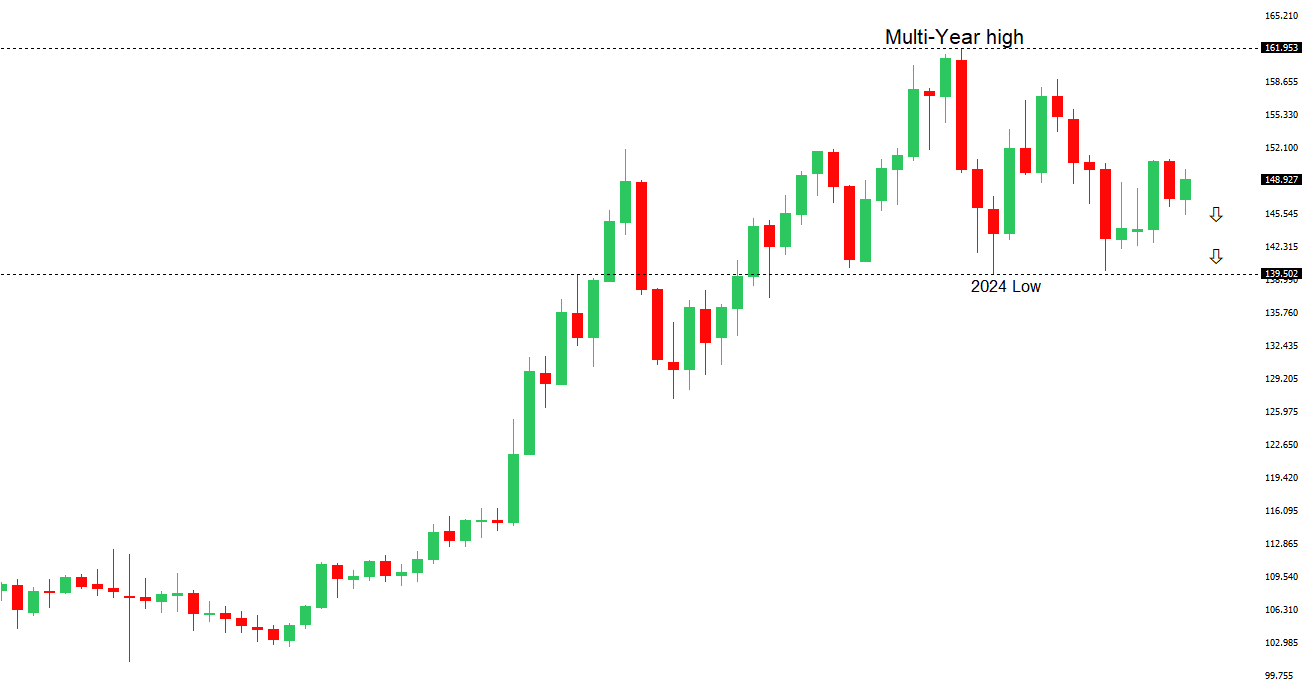

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 152.00. | ||

| ||

| R2 150.92 - 1 August high - Strong R1 149.96 - 26 September high - Medium S1 147.46 - 23 September low - Medium S2 145.48 - 17 September low - Strong | ||

| USDJPY: fundamental overview | ||

| The Bank of Japan is under increasing pressure to raise interest rates, with two board members advocating for a quarter-point hike at the September meeting, signaling a hawkish shift despite Governor Kazuo Ueda’s cautious stance. Rising inflation, particularly in food and daily goods, and a potential yen drop are fueling calls for a rate hike as early as October, especially if economic data remains strong and the U.S. avoids a downturn. The upcoming Tankan survey and Deputy Governor Uchida’s speech this week could provide further clues on BOJ’s policy direction, while Japan’s industrial production and retail sales weakened in August, though manufacturers expect a rebound in September. The Liberal Democratic Party’s leadership race, with Shinjiro Koizumi as a frontrunner, may influence BOJ’s confidence in raising rates, potentially strengthening the yen if Koizumi wins. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6707 - 17 September/2025 high - Strong R1 0.6660 - 18 September high - Medium S1 0.6520 - 26 September low - Medium S1 0.6483 - 2 September low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Reserve Bank of Australia maintained the cash rate at 3.60%, citing stable labor markets, recovering demand, and persistent inflation, signaling a cautious, data-driven approach with no immediate rate cuts expected. Despite recent rate cuts still impacting the economy, the RBA remains vigilant about inflation and global risks, suggesting a hawkish stance that may prolong restrictive monetary policy. Recent data shows a sharp decline in building approvals and private sector housing, highlighting weakness in construction and housing demand, while private sector credit growth remains steady but shows no significant acceleration. | ||

| Suggested reading | ||

| There’s No Dollar ‘Demand’ & ‘Supply’: There’s Only Production, J. Tamny, Forbes (September 28, 2025) Companies You Least Expect Will Become AI Stocks, S. McBride, RiskHedge (September 26, 2025) | ||