| ||

| 1st October 2025 | view in browser | ||

| Fed caution, jobs data key for dollar | ||

| Last week’s robust U.S. economic data and the Federal Reserve’s cautious approach to aggressive rate cuts supported a modest recovery in the U.S. dollar, though its broader bearish trend persists. | ||

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1919 - 16 September/2025 high -Strong R1 1.1820 - 23 September high - Medium S1 1.1646 - 25 September low - Medium S2 1.1574 - 27 August low - Strong | ||

| EURUSD: fundamental overview | ||

| German inflation rose to 2.4% in September, surpassing expectations due to higher service costs and smaller energy price declines, contributing to a eurozone-wide trend where inflation hit 2.2%, above the ECB’s 2% target. ECB policymakers are divided, with some advocating for steady rates and others open to future easing, though decisions will remain data-driven. Despite short-term inflationary pressures from energy, Germany’s disinflation trend continues, with inflation expected to stabilize above 2%. The ECB remains cautious, while the eurozone benefits from a stronger euro and mitigated tariff impacts, though trade and geopolitical risks persist. Long-term, Germany’s reforms and infrastructure spending may boost eurozone growth, supporting a bullish euro against the dollar. | ||

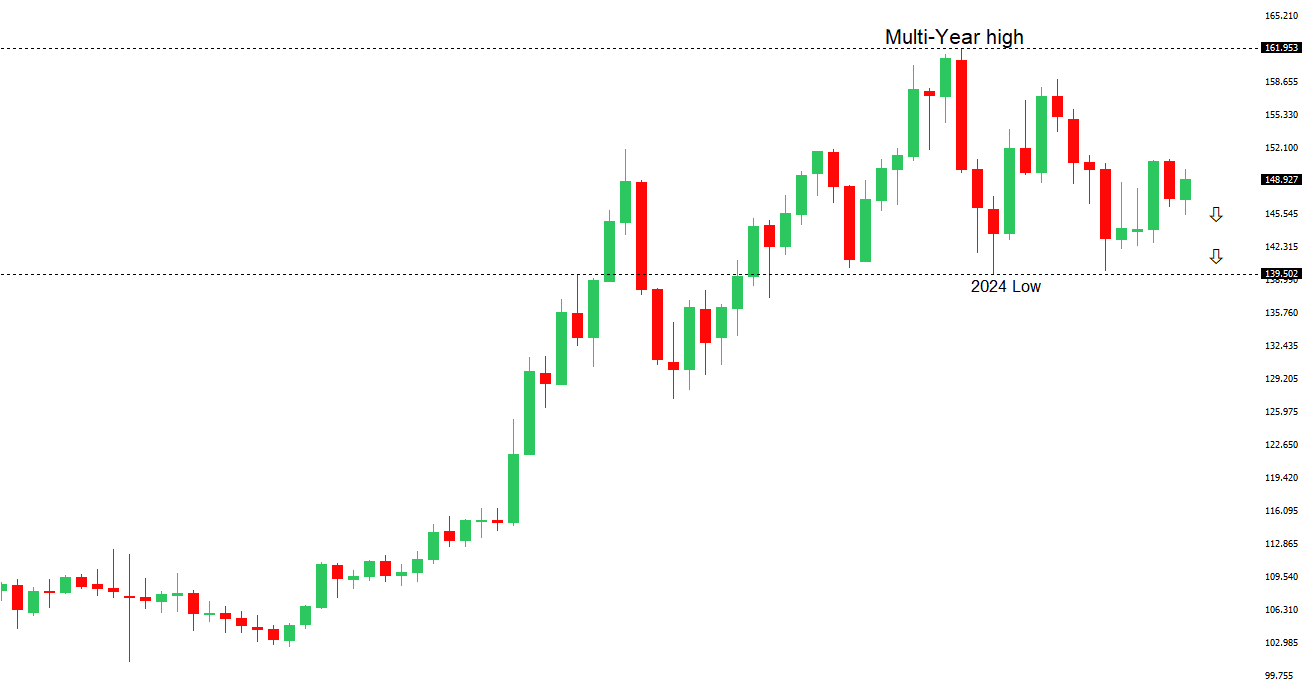

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 152.00. | ||

| ||

| R2 150.92 - 1 August high - Strong R1 149.96 - 26 September high - Medium S1 147.46 - 23 September low - Medium S2 145.48 - 17 September low - Strong | ||

| USDJPY: fundamental overview | ||

| The Bank of Japan is considering further interest rate hikes, with two of nine policy board members advocating for an immediate increase to address persistent inflation, while the majority prefers caution due to uncertainties around the U.S. economy. The BOJ plans to reduce its government bond purchases to ¥3.3 trillion monthly and offload some exchange-traded funds, signaling a gradual shift from ultra-loose monetary policy. Market expectations for an October rate hike have risen, with a 68% probability, supported by improving business confidence in Japan’s Tankan survey and comments from BOJ board member Asahi Noguchi, indicating stronger economic and price risks. These moves are expected to support the yen by tightening monetary policy and reducing bond market pressure. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6707 - 17 September/2025 high - Strong R1 0.6660 - 18 September high - Medium S1 0.6520 - 26 September low - Medium S1 0.6483 - 2 September low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Reserve Bank of Australia maintained the cash rate at 3.6%, as inflation, particularly in services, is not cooling as quickly as expected, with the 2.5% target still the priority. Despite resilient growth and a tight labor market, the RBA is adopting a cautious, data-driven approach, reducing expectations for near-term rate cuts, with markets now seeing less than a 40% chance of a cut in November and analysts predicting gradual easing into 2026. Rising labor costs and robust consumer spending support economic confidence, but softening job market trends and global risks like U.S. tariffs and weaker Chinese demand could prompt a policy shift if growth falters, while the Australian dollar strengthens due to slower easing expectations and potential rate divergence with the U.S. | ||

| Suggested reading | ||

| How First Brands Group collapsed, R. Smith, Financial Times (September 30, 2025) Gold: The Most Interesting Chart In The World, J. Calhoun, Alhambra (September 28, 2025) | ||