| ||

| 21st April 2026 | view in browser | ||

| Markets steady as Iran talks inch forward | ||

| Global markets head into the new day with a cautiously constructive tone, as investors continue to navigate mixed geopolitical signals around US–Iran negotiations, where conflicting rhetoric is being offset by signs of progress toward talks in Islamabad and the possibility of a ceasefire extension. | ||

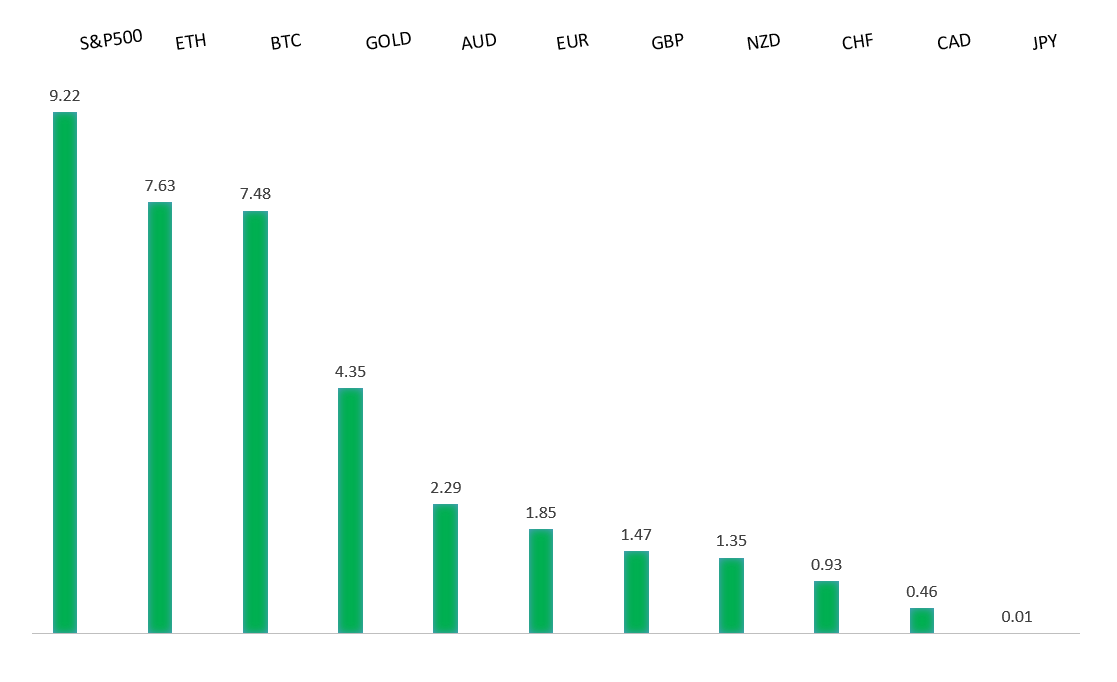

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

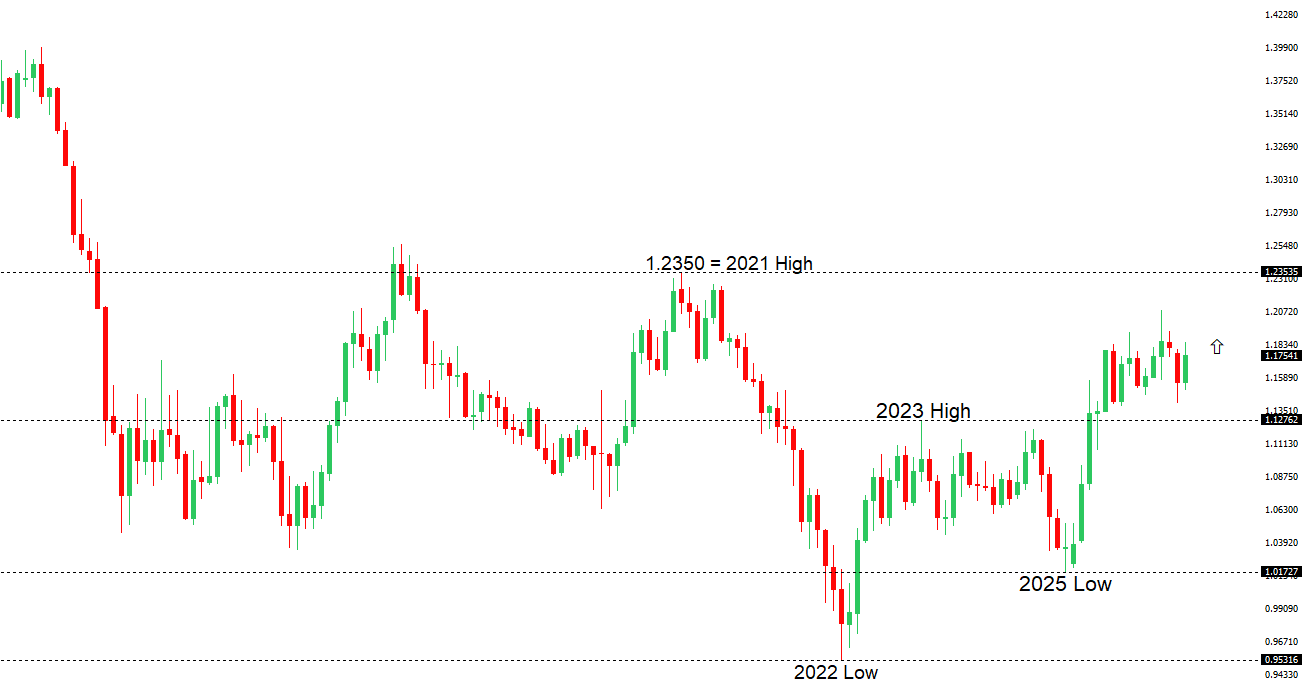

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1850 - 17 April high - Strong R1 1.1800 - Figure - Medium S1 1.1729 - 20 April low - Medium S2 1.1650 - 9 April low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has been supported by a softer US dollar backdrop, helping EURUSD push up toward the 1.1800 area, as easing geopolitical tensions between the US and Iran—on news both sides are set to resume negotiations—have encouraged a more constructive risk tone and reduced safe-haven demand for the dollar. At the same time, US data has leaned dollar-negative, with the recently softer-than-expected US Producer Price Index readings reinforcing expectations for a less aggressive Fed policy outlook, even as labor market signals remain resilient via the ADP National Employment Report. On the eurozone side, firmer German producer prices have offered some modest fundamental backing for the euro, contributing to the relative outperformance as markets continue to balance improving regional data against a still-cautious growth outlook. | ||

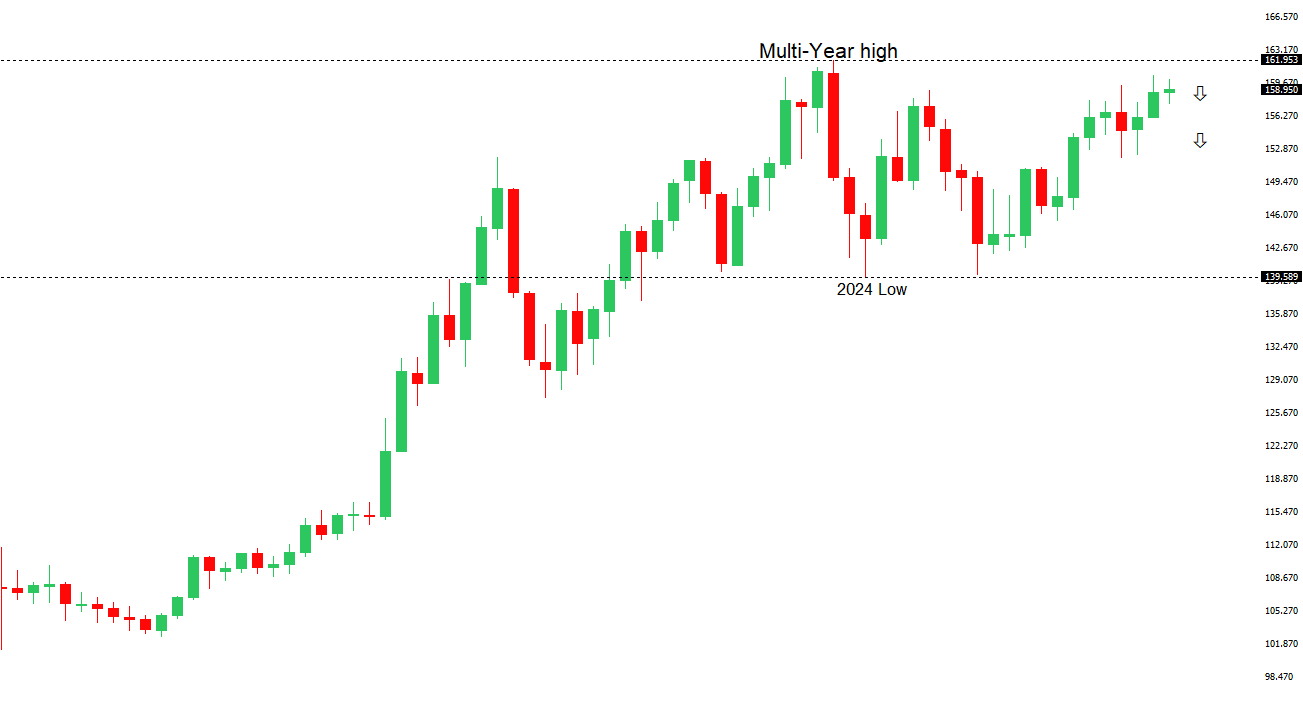

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 160.46 - 30 March/2026 high - Strong R1 160.03 - 7 April high - Medium S1 158.00 - Figure - Medium S2 157.51 - 19 March low - Strong | ||

| USDJPY: fundamental overview | ||

| The Japanese yen has been under pressure, with USDJPY pressured higher as markets scale back expectations for near-term tightening from the Bank of Japan, particularly amid concerns that rising energy costs could weigh on Japan’s already fragile growth outlook. Geopolitical tensions have also played a role, with renewed strain between the US and Iran supporting the US dollar through safe-haven demand, further dragging on the yen. Domestically, a strong earthquake off Japan’s east coast and reports of a tsunami have added an element of uncertainty, though confirmation of no damage to key infrastructure, including nuclear facilities, has limited direct economic fallout. Overall, the yen remains driven by a combination of dovish central bank expectations, external geopolitical developments, and relative dollar strength. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7222 - 17 April/2026 high - Strong R1 0.7200 - Figure - Medium S1 0.7115 - 20 April low - Medium S2 0.6963 - 8 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar continues to hold up well overall despite renewed geopolitical uncertainty around US–Iran tensions, as it’s helped along by offsetting, constructive domestic fundamentals. Ongoing disruptions to global energy supply have lifted inflation expectations, reinforcing the case for further tightening from the Reserve Bank of Australia, especially alongside a still-robust labor market that has markets leaning toward another rate hike at the upcoming meeting. At the same time, mixed signals around ceasefire negotiations and the approaching deadline for de-escalation have kept risk sentiment fragile, limiting upside in the Aussie despite a relatively supportive macro backdrop, with attention now turning to Thursday’s PMI data for clearer direction on growth momentum. | ||

| Suggested reading | ||

| The Problem With Kevin Warsh Isn’t His Wealth, It’s His Wealth, J. Tamny, Forbes (April 19, 2026) They Dared to Exit Merrill, Became Renegades In Process, A. Welsch, Barron’s (April 15, 2026) | ||