| ||

| 20th April 2026 | view in browser | ||

| Risk off returns as Iran tensions lift oil | ||

| Global markets are starting the week on a cautious footing as geopolitical tensions between the US and Iran intensify, even as both sides continue to signal a desire to reach a deal. | ||

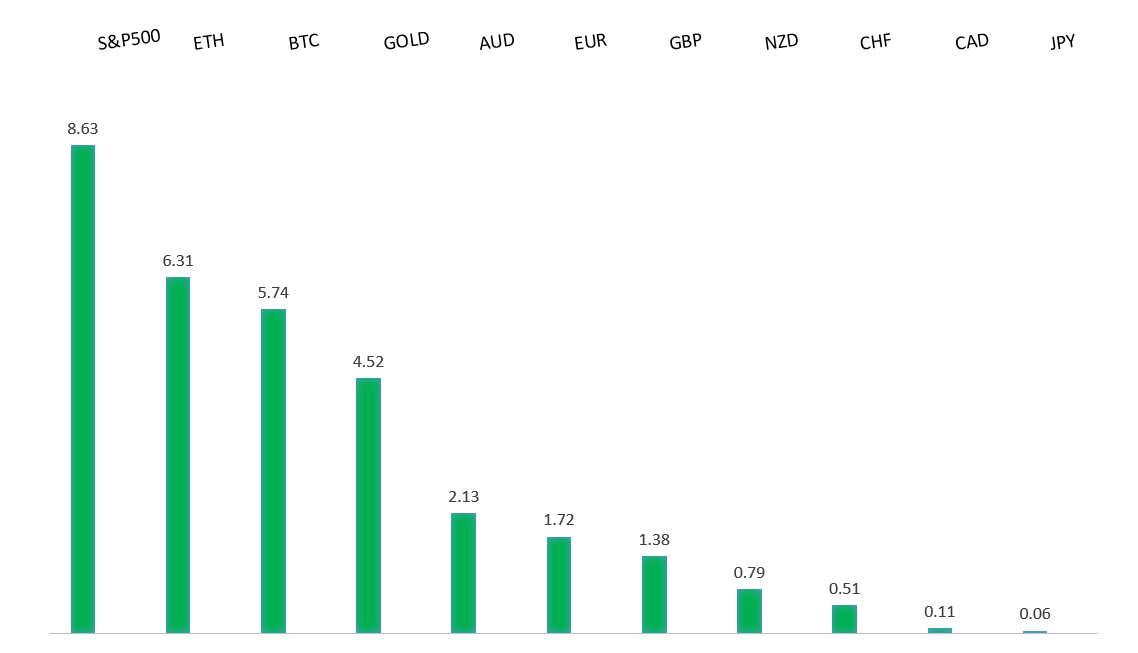

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

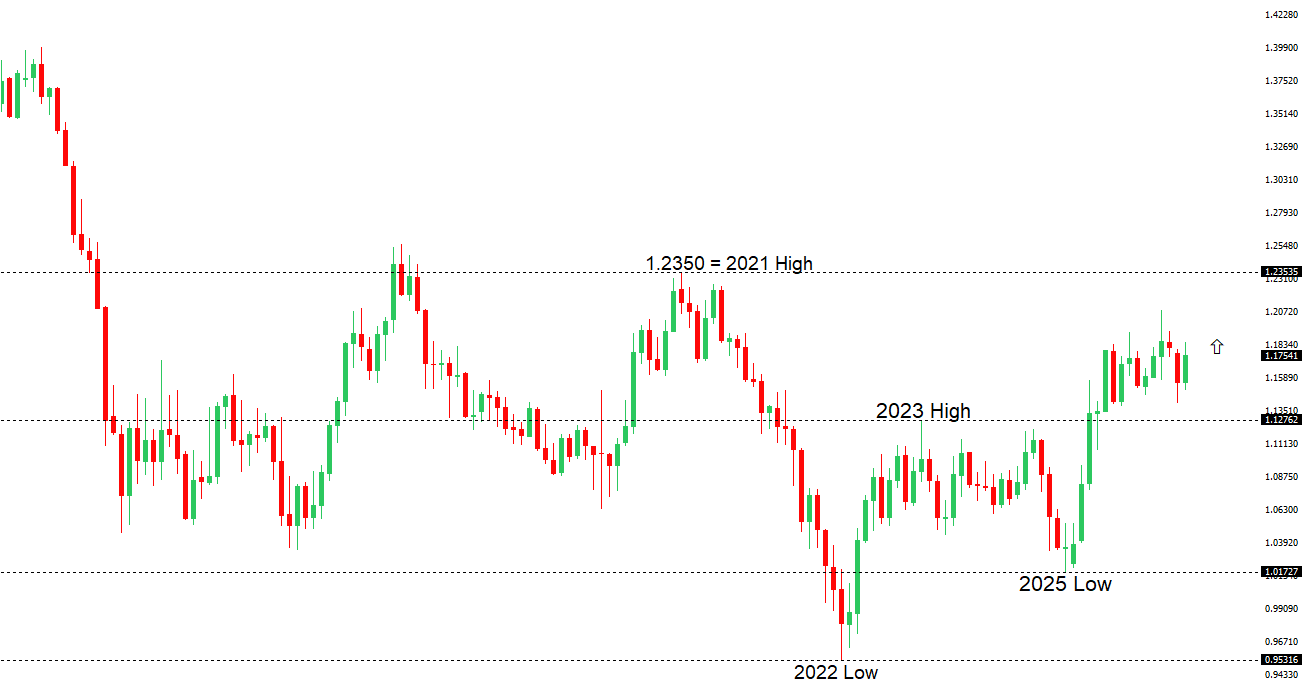

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1850 - 17 April high - Strong R1 1.1800 - Figure - Medium S1 1.1754 - 14 April low - Medium S2 1.1650 - 9 April low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro is trading with a softer tone to start Monday, weighed primarily by external geopolitical risks rather than any fresh eurozone specific catalysts, as escalating tensions in the Middle East and higher oil prices act as a terms-of-trade negative for the region’s energy-importing economies. On the domestic front, the lack of new data or hawkish signals from the ECB is leaving the currency without support, especially as policy expectations remain anchored around a cautious and gradual easing path. Meanwhile, steady policy from China and a broadly firmer US dollar backdrop amid risk aversion are adding to downside pressure, with the euro also reflecting some sensitivity to global trade uncertainty given the bloc’s export-heavy profile. | ||

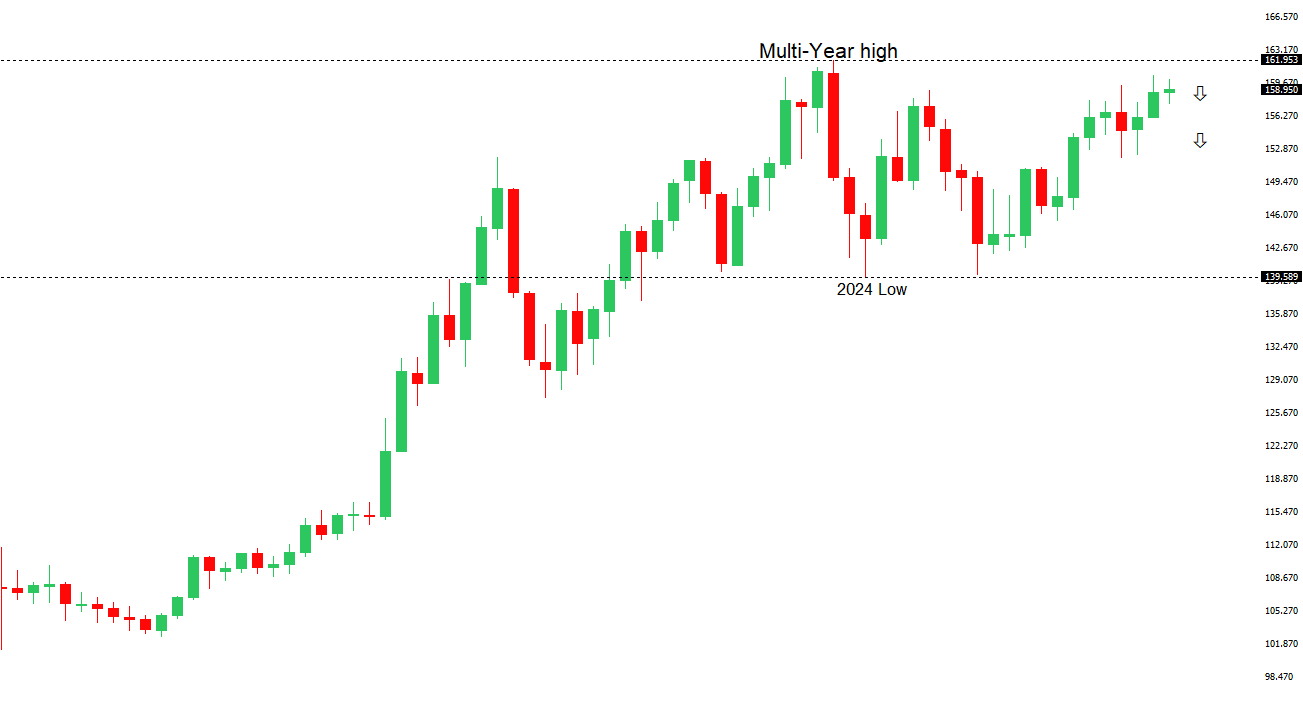

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 160.46 - 30 March/2026 high - Strong R1 160.03 - 7 April high - Medium S1 158.00 - Figure - Medium S2 157.51 - 19 March low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen remains on the back foot to start the week, driven by a mix of geopolitical and structural headwinds that are offsetting its traditional safe-haven appeal. Escalating tensions in the Middle East and the ongoing disruption in the Strait of Hormuz are particularly negative for Japan, given its heavy reliance on imported energy, with higher oil prices worsening the country’s trade balance and growth outlook. This dynamic is limiting yen demand even as broader risk sentiment deteriorates. At the same time, the Bank of Japan’s still accommodative policy stance continues to contrast with relatively tighter global settings, keeping yield differentials unfavorable. On the policy front, rhetoric from Tokyo has intensified, with officials signaling heightened concern over FX volatility and hinting at a rising risk of intervention as USDJPY pushes toward key levels, though for now this has only slowed, not reversed, the yen’s weakness. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7222 - 17 April/2026 high - Strong R1 0.7200 - Figure - Medium S1 0.7077 - 14 April low - Medium S2 0.6963 - 8 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar is holding up relatively well on Monday after an initial gap lower, with dip-buying emerging as supportive domestic fundamentals offset a more cautious global backdrop. While renewed US–Iran tensions and a firmer US dollar at the open briefly pressured AUD, the move has been limited by shifting expectations around US monetary policy, with reduced odds of further Fed tightening capping USD upside. At the same time, the RBA’s comparatively hawkish stance continues to underpin the currency, reinforcing yield support for AUD. That said, the currency remains sensitive to broader risk sentiment and global trade dynamics, meaning gains are being tempered as markets weigh geopolitical uncertainty against still-solid carry appeal. | ||

| Suggested reading | ||

| Risk, Not Volatility, Is the Real Enemy for Investors, C. Benz, Morningstar (April 15, 2026) A Dispatch From The Bond Number Crunchers, M. Russell, Bond Vigilantes (April 15, 2026) | ||