| ||

| 15th May 2026 | view in browser | ||

| Oil surge and yields climb as markets turn defensive | ||

| Rising geopolitical tensions around Iran are driving a risk-off shift across markets, with higher oil prices and bond yields supporting the dollar while weighing on equities, FX risk proxies, and precious metals. | ||

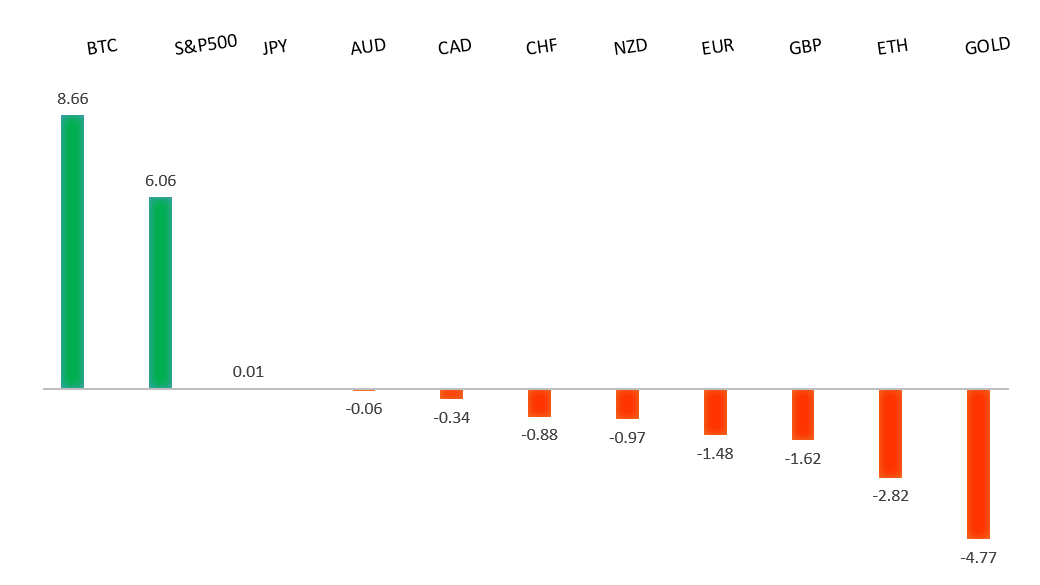

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1850 - 17 April high - Strong R1 1.1797 - 6 May high - Medium S1 1.1643 - 15 May low - Medium S2 1.1589 - 8 April low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has come under renewed fundamental pressure, driven primarily by a powerful shift in relative monetary policy expectations and stronger US macro data. A run of firm US releases—particularly resilient retail sales and hotter-than-expected CPI and PPI—has reinforced the “higher-for-longer” narrative around the Federal Reserve, with markets now largely pricing out rate cuts and even assigning some probability to further tightening. This has been compounded by hawkish Fed rhetoric emphasizing persistent inflation risks and economic resilience. At the same time, improving US-China relations and easing geopolitical tail risks (including commitments around the Strait of Hormuz) have supported broader risk sentiment but, more importantly, boosted the US Dollar via growth and stability channels. On the euro side, while expectations for a potential rate hike from the European Central Bank offer some offset, they have taken a back seat to the dominant USD story, with Eurozone data and inflation prints largely seen as secondary. The resulting widening in rate differentials and relative growth dynamics has tilted the near-term bias against the euro. | ||

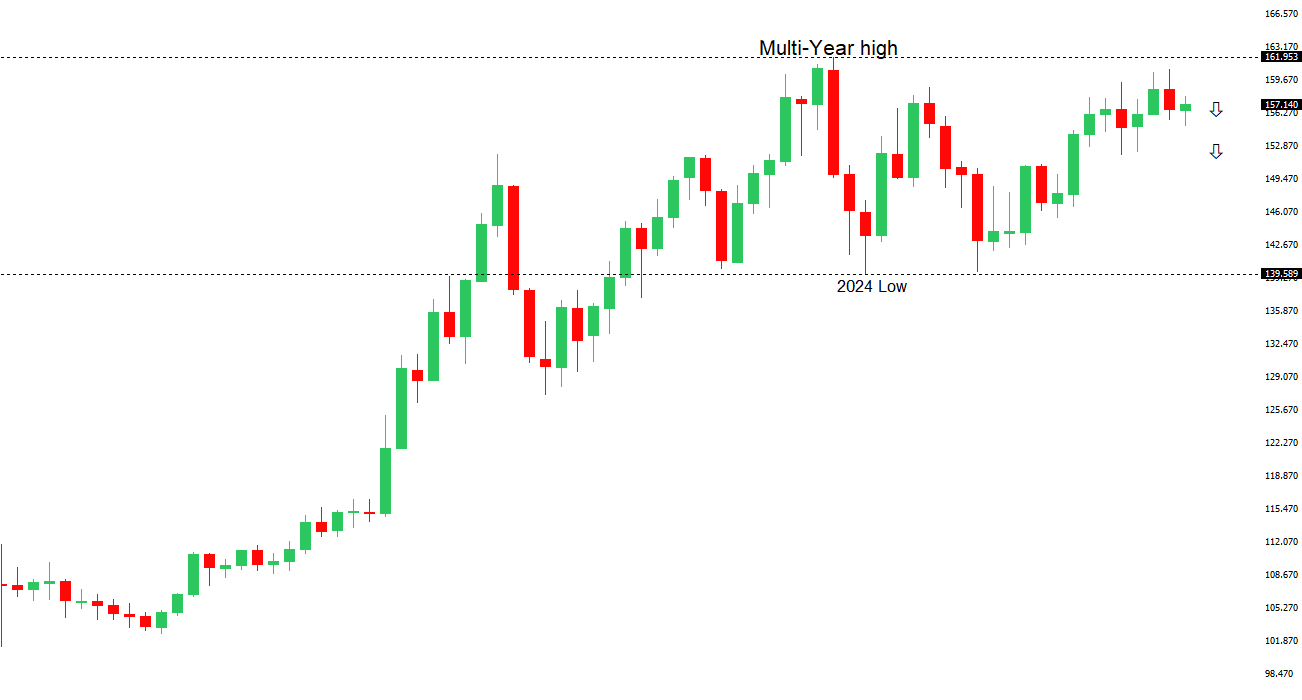

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 159.53 - 17 April low - Medium R1 159.00 - Figure - Medium S1 157.29 - 14 May low - Medium S2 155.02 - 6 May low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen remains under sustained fundamental pressure, driven primarily by the wide and persistent yield differential with the U.S., alongside growing skepticism that Japan’s policy tools can meaningfully reverse the trend. A recent Reuters poll highlights that nearly three-quarters of economists see FX intervention as ineffective in curbing weakness, especially with USDJPY already reclaiming levels around 158.50 and erasing prior intervention impact. While expectations remain for gradual Bank of Japan tightening—with many looking for a move toward 1.00% as soon as June and 1.25% by Q4—there is clear hesitation amid external risks, particularly the ongoing Middle East conflict, which is exacerbating Japan’s terms-of-trade shock via higher energy import costs. This dynamic is reinforcing downside pressure on the yen by worsening Japan’s trade balance and household purchasing power, as acknowledged by Finance Minister Katayama. At the same time, rising global yields and resilient U.S. economic data continue to anchor dollar strength, leaving the BOJ caught between supporting the currency and avoiding policy tightening that could undermine a still-fragile domestic recovery. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7300 - Figure - Medium R1 0.7278 - 6 May/2026 high - Medium S1 0.7101 - 30 April low - Medium S2 0.6963 - 8 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian Dollar has been trading with a softer tone, caught between external geopolitical uncertainty and shifting rate expectations. On the external front, markets are closely tracking developments around US-China relations following comments from Donald Trump highlighting “fantastic trade deals” with Xi Jinping, though underlying tensions—particularly around Taiwan—continue to inject caution. This matters for the Aussie given its strong correlation to China as Australia’s largest trading partner, leaving it sensitive to any deterioration in the relationship. At the same time, broader geopolitical risks tied to Iran and the Strait of Hormuz are adding another layer of uncertainty to global trade and commodity flows. On the macro side, firmer-than-expected US inflation has pushed markets to scale back expectations for Fed easing and even price some probability of additional tightening, supporting the USD and weighing on AUDUSD. This comes as the Aussie lacks a strong domestic catalyst, leaving it largely driven by external factors—namely China sentiment, global risk appetite, and widening rate differentials in favor of the US. | ||

| Suggested reading | ||

| The War on Billionaires Is Dangerous Nonsense, M. Strain, Project Syndicate (May 13, 2026) Is The US/China Decoupling Real?, N. Smith, Noahpinion (May 13, 2026) | ||