| ||

| 18th May 2026 | view in browser | ||

| Oil spike fuels inflation fears and higher yields | ||

| Global markets are under pressure as escalating geopolitical tensions drive an oil-led inflation shock, pushing yields higher, weighing on equities, and broadly supporting the dollar. | ||

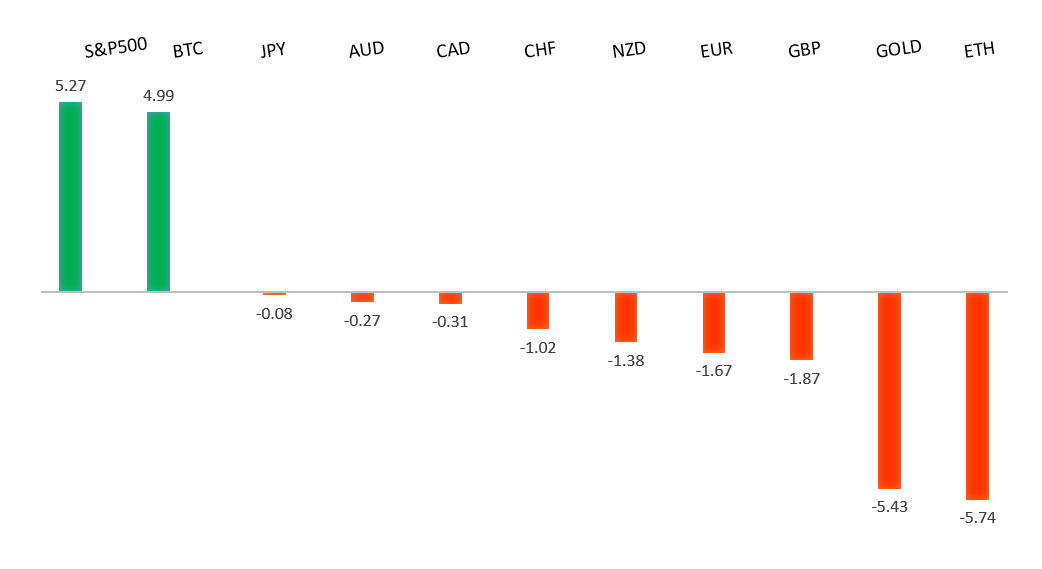

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1797 - 6 May high - Medium R1 1.1722 - 14 May high - Medium S1 1.1600 - Figure - Medium S2 1.1589 - 8 April low - Strong | ||

| EURUSD: fundamental overview | ||

| The Euro has been under pressure in recent sessions, with EURUSD drifting lower as the US Dollar strengthens on a combination of rising rate expectations and a more defensive global backdrop. Markets have repriced the path of Federal Reserve policy after a series of hawkish signals from officials stressing that inflation remains the dominant concern, with pricing for an additional rate hike jumping sharply. This widening policy divergence—at least in the near term—has tilted yield support back toward the Dollar. At the same time, elevated geopolitical tensions, including risks around the Strait of Hormuz and broader US-China frictions, have driven safe-haven demand into the Dollar, further weighing on the Euro. That said, downside in the single currency has been somewhat cushioned by expectations that the European Central Bank will also need to maintain a hawkish stance, with sticky inflation keeping the door open for further tightening, limiting the extent of EUR underperformance even as external headwinds persist. | ||

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 159.53 - 17 April low - Medium R1 159.08 - 18 May high - Medium S1 157.29 - 14 May low - Medium S2 155.02 - 6 May low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen has come under renewed pressure, with USDJPY pushing back above 159 as a confluence of external and domestic fundamentals tilts decisively against the currency. The primary driver has been broad USD strength, underpinned by rising geopolitical tensions around Iran, which are reinforcing the dollar’s safe-haven appeal while simultaneously pushing oil prices higher and reviving global inflation risks. This dynamic has fed directly into more hawkish Fed expectations, with markets now pricing a meaningful probability of further tightening and US yields remaining elevated—widening rate differentials sharply in favor of the dollar. In contrast, the yen is failing to benefit from traditional risk-off flows, as Japan’s heavy reliance on imported energy leaves it particularly exposed to Middle East-driven oil shocks, worsening the domestic terms of trade and growth outlook. At the same time, the Bank of Japan remains far behind the Fed in policy normalization, limiting any yield support for the currency. While intermittent intervention fears from Japanese authorities are helping to slow, but not reverse, the move, they have so far proven insufficient against the powerful combination of USD strength, higher US yields, and Japan-specific vulnerability to the current geopolitical backdrop. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7300 - Figure - Medium R1 0.7278 - 6 May/2026 high - Medium S1 0.7101 - 30 April low - Medium S2 0.6963 - 8 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian Dollar remains under pressure, trading below 0.7150, primarily driven by a combination of weaker-than-expected Chinese data and a more supportive backdrop for the US Dollar. Disappointing activity indicators out of China—most notably soft Retail Sales, slower Industrial Production, and a contraction in Fixed Asset Investment—have reinforced concerns about demand from Australia’s largest trading partner, weighing directly on AUD sentiment. At the same time, the USD has found renewed strength as Federal Reserve officials continue to emphasize a higher-for-longer stance on interest rates, with markets sharply repricing the probability of additional tightening. This policy divergence is further amplified by rising geopolitical tensions, including US-Iran frictions and broader global uncertainty, which are boosting safe-haven flows into the Dollar. While higher oil prices could, in theory, support Australia via terms of trade, the dominant drivers at present remain China growth concerns and relative rate dynamics, keeping AUDUSD biased to the downside. | ||

| Suggested reading | ||

| A “Casino” Stock Market, B. Smead, Smead Capital Management (May 14, 2026) Inflation’s Elevated No Matter How You Slice It, S. Varghese, Carson Group (May 13, 2026) | ||