| ||

| 3rd October 2025 | view in browser | ||

| Global markets cautious as US shutdown clouds data | ||

| The US government shutdown delayed key data like nonfarm payrolls and jobless claims, forcing reliance on private-sector data. The shutdown, combined with fiscal concerns and trade tensions, raises risks to economic growth. | ||

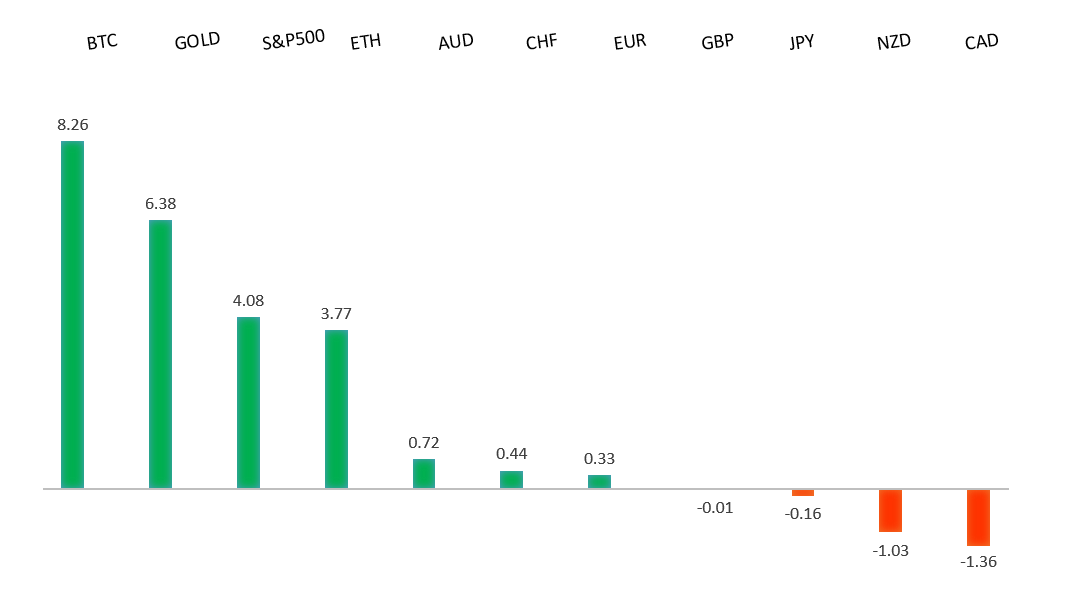

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1919 - 16 September/2025 high -Strong R1 1.1820 - 23 September high - Medium S1 1.1646 - 25 September low - Medium S2 1.1574 - 27 August low - Strong | ||

| EURUSD: fundamental overview | ||

| ECB Governing Council member Martins Kazaks stated that the current 2% interest rate is suitable unless significant economic shocks occur, with the ECB ready to adjust policies based on inflation risks and new data. The eurozone unemployment rate rose slightly to 6.3% in August, but remains near historic lows, with resilience in southern countries like Spain and Italy contrasting with rising joblessness in Germany and France, highlighting the need for flexible ECB policies. Meanwhile, the Swiss National Bank increased foreign exchange interventions in Q2 2025, favoring euros over dollars to stabilize the Swiss franc amid U.S. tariffs and negative Swiss inflation, potentially signaling a broader shift in global currency reserve strategies. ECB’s Francois Villeroy de Galhau echoed calls for strengthening the euro’s global role through more euro-area safe assets, amid U.S. protectionism and stablecoin growth. Upcoming Eurozone PPI data for August 2025 is expected to show deflationary trends, with a forecasted year-on-year decline to -0.4%, reflecting weak industrial pricing power. | ||

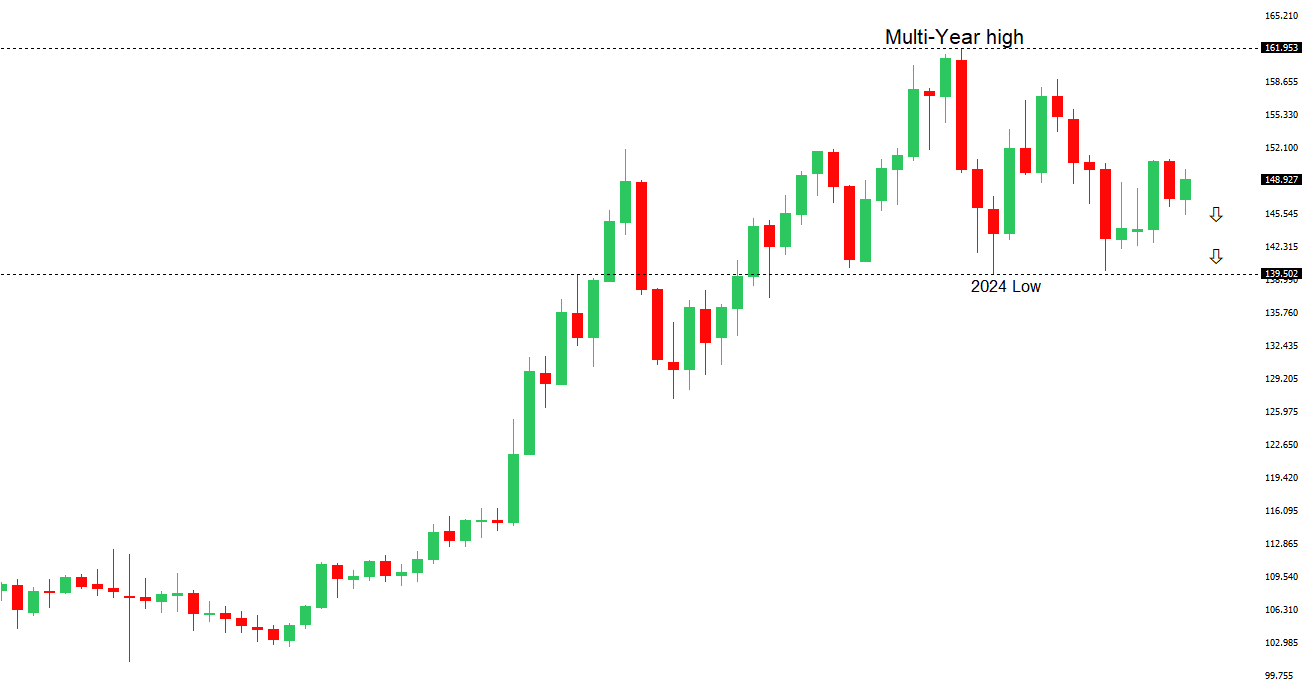

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 152.00. | ||

| ||

| R2 149.96 - 26 September high - Strong R1 148.85 - 30 September high - Medium S1 146.58 - 1 October low - Medium S2 145.48 - 17 September low - Strong | ||

| USDJPY: fundamental overview | ||

| The Bank of Japan is prepared to raise interest rates if economic growth and inflation align with projections, but has not set a specific timeline, according to Deputy Governor Shinichi Uchida and Governor Kazuo Ueda. Recent data, including the Q3 Tankan survey and revised PMI figures (Composite at 51.3, Services at 53.3), show improving business confidence and steady economic recovery, supporting potential policy tightening. However, global trade risks, domestic political uncertainty, and lack of clear guidance on rate hikes have left traders cautious, with USDJPY nearing key technical levels and the yen potentially strengthening if political stability emerges. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6707 - 17 September/2025 high - Strong R1 0.6660 - 18 September high - Medium S1 0.6520 - 26 September low - Medium S1 0.6483 - 2 September low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar is gaining strength due to expectations of a slower, more cautious monetary easing cycle, supported by robust economic data and a potential rate divergence with the U.S., where more Federal Reserve rate cuts are anticipated. However, persistent domestic inflation and global risks, such as U.S. tariffs and weaker Chinese demand, could reverse these gains if economic momentum falters, possibly prompting the Reserve Bank of Australia to cut rates more decisively. Recent data shows modest household spending growth, suggesting the RBA might consider rate cuts in November, while steady Chinese yuan appreciation supports the Australian dollar as a yuan proxy. Australia’s September PMI data indicates continued economic expansion, with rising business activity, export orders, and employment, signaling a gradual recovery aided by easing inflation and lower interest rates. | ||

| Suggested reading | ||

| AI Isn’t Driving the Labor Market Slowdown, M. Leonhardt, Barron’s (October 2, 2025) 10 Cheap Wide-Moat Stocks For The Rest Of The Year, S. Dziubinski, Morningstar (October 1, 2025) | ||