| ||

| 31st December 2025 | view in browser | ||

| Global growth steadies, policy support edges closer | ||

| Global macro signals heading into the new day point to steady but uneven growth across regions, with inflation generally easing and policy turning more supportive into 2026. | ||

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1400. | ||

| ||

| R2 1.1919 - 17 September/2025 high -Strong R1 1.1809 - 24 December high - Medium S1 1.1703 - 19 December low - Strong S2 1.1615 - 9 December low - Strong | ||

| EURUSD: fundamental overview | ||

| The Euro came under some pressure after failing to hold gains, with year-end flows limiting momentum despite a broader medium-term USD bearish backdrop. The key driver remains policy divergence: the ECB is signalling patience and caution, keeping rates at 2% as inflation hovers near target, while markets still expect the Fed to deliver further easing into 2026 despite internal disagreement on timing. Spanish inflation eased slightly in December but remains above the euro-area average, reinforcing expectations that the ECB will stay on hold for longer. Looking ahead, improving eurozone growth, a narrowing US growth advantage, and concerns over US debt and valuations underpin expectations among major banks for EURUSD to rise toward 1.20–1.25 by end-2026. | ||

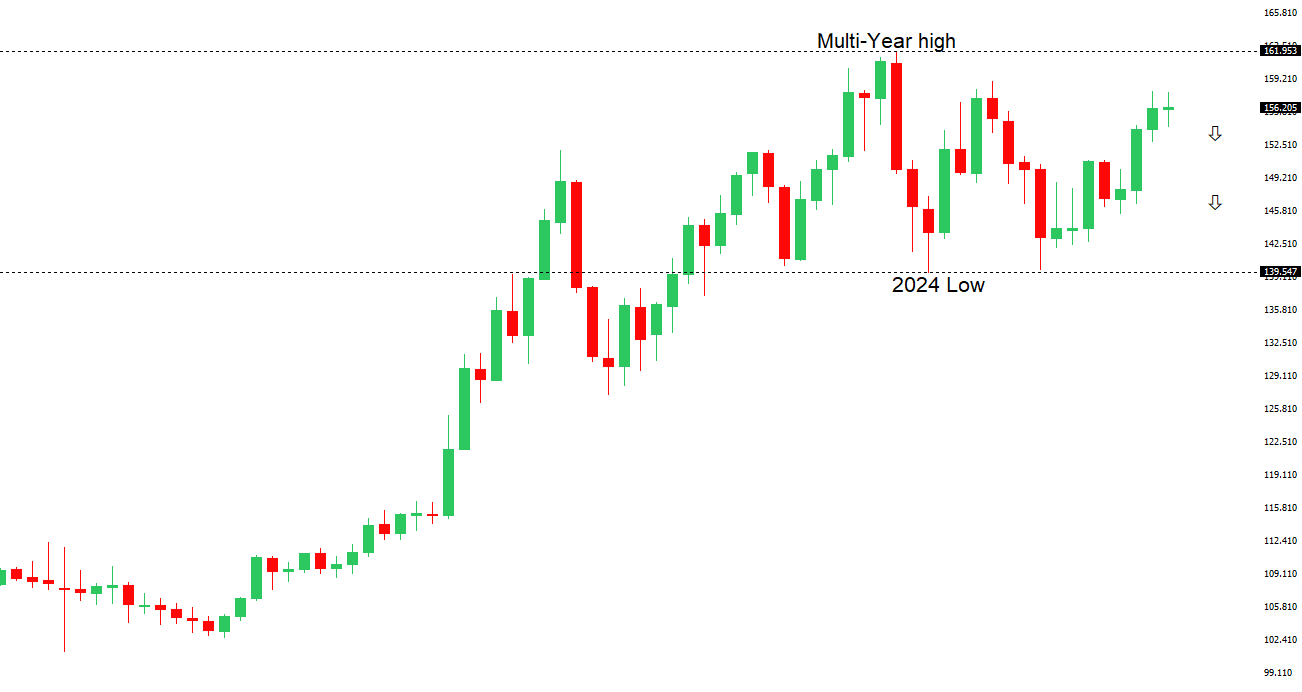

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 ahead of a fresh down-leg back towards the 2024 low at 139.58. | ||

| ||

| R2 157.90 - 20 November/2025 high - Strong R1 157.00 - Figure - Medium S1 154.39 - 16 December low - Strong S2 153.61 - 14 November low - Medium | ||

| USDJPY: fundamental overview | ||

| The yen remains driven more by concerns over Japan’s fiscal stance and policy credibility than by a clear normalization story. While the BOJ continues to debate gradual rate hikes, arguing policy is still below neutral, Japan’s expansionary budget and structural headwinds keep the yen under pressure. Authorities have signaled readiness to intervene if USDJPY breaks above 158, which would significantly raise political pressure, even as markets watch key technical levels around 155. Longer term, views are split: some see gradual BOJ tightening and Fed easing supporting yen appreciation, while many banks still expect persistent yen weakness due to wide yield gaps, negative real rates, capital outflows, and limits on how far the BOJ can raise rates. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6800 - Figure - Medium R1 0.6728 - 29 December/2025 high - Medium S1 0.6592 - 18 December low - Medium S2 0.6421 - 21 November low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar is holding up close to its year-to-date high, supported by resilient commodity demand and expectations that the RBA may shift toward tightening as inflation risks persist. Positive but modest support has come from signs of stabilization in China’s economy, though markets remain cautious given the uneven recovery and limited policy clarity. With the Aussie among the top-performing G10 currencies this quarter, sustained gains since mid-November, strong commodities, improving global risk sentiment, and a softer US dollar backdrop are expected to support further AUD appreciation into 2026. | ||

| Suggested reading | ||

| How Do Keynesians Think the Economy Will Perform In ’26?, J. Mathis, The Week (December 30, 2025) A Weak Dollar Remains Big Danger, J. Tamny, The Steve Gruber Show (December 28, 2025) | ||