| ||

| 25th February 2026 | view in browser | ||

| Buck eases amid Trump spotlight and cautious central banks | ||

| The US dollar begins the day on softer footing amid focus on Trump’s headline-driven political developments, cautious Fed signals, dovish-leaning BOJ expectations, and mixed global data. | ||

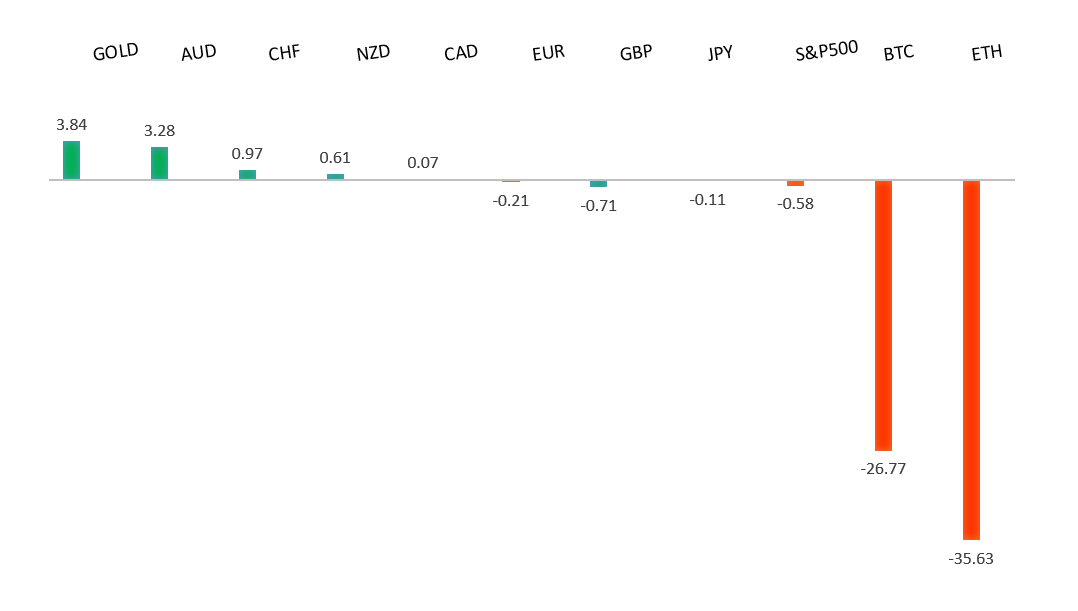

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1500. | ||

| ||

| R2 1.2081 - 27 Janaury/2026 high - Strong R1 1.1929 - 10 February high - Medium S1 1.1742 - 19 February low - Medium S2 1.1728 - 23 January low - Medium | ||

| EURUSD: fundamental overview | ||

| The euro is up slightly but remains under pressure near its 50-day average, weighed down by US tariff threats, trade uncertainty, and geopolitical tensions, while the dollar continues to draw support from elevated US yields and expectations the Fed will keep rates higher for longer. Germany’s March GfK consumer confidence is expected to improve modestly, helped by stronger income expectations and easing inflation, though sentiment remains weak and gains are likely to be limited amid economic and geopolitical uncertainty. Meanwhile, Chancellor Friedrich Merz is reshaping Germany’s China strategy toward a pragmatic “de-risking” approach—seeking fair, rules-based trade and reduced dependencies while maintaining cooperation and positioning Europe’s relationship with China as balanced, resilient, and mutually respectful. | ||

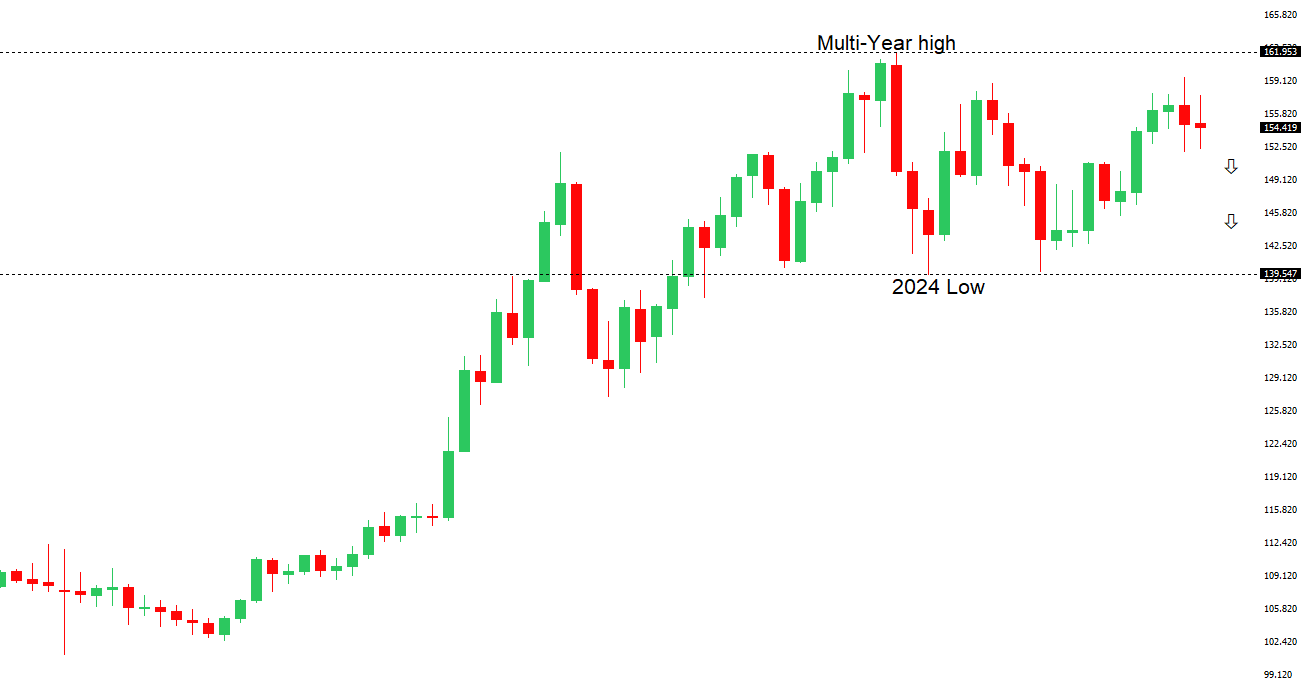

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. The recent break below 154.39 strengthens the outlook. | ||

| ||

| R2 157.66 - 9 February high - Strong R1 156.30 - 10 February high - Medium S1 154.00 - 23 February low - Medium S2 151.97 - 28 January/2026 low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen is holding steady, but recent political developments point to continued near-term weakness. Prime Minister Takaichi’s nomination of reflation-leaning academics to the BOJ board and her cautious stance on further rate hikes have lowered expectations for near-term tightening, reinforcing the view that Japan’s real yields will remain deeply negative. Combined with soft demand from China and ongoing US–Japan rate differentials, this backdrop favors dollar strength, with USDJPY likely biased higher in the coming weeks, though excessive yen weakness could trigger verbal intervention. Meanwhile, steady services inflation supports gradual policy normalization over time but offers no urgency for the BOJ to accelerate hikes. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7158 - 2023 high - Strong R1 0.7147 - 12 February/2026 high - Strong S1 0.7007 - 9 February low - Medium S2 0.6897 - 6 February low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar has been bid up after stronger-than-expected January CPI reinforced the view that the RBA may still tighten policy this year. Headline CPI rose 0.4% MoM, bringing the annual rate to 3.8%, above expectations and still well above the RBA’s 2–3% target, highlighting persistent inflation, especially in services. Markets now see a modest chance of another rate hike as soon as March, with slightly higher expectations for further tightening into May. The RBA expects inflation to peak around mid-2026 before gradually easing, though strong demand, higher travel and fuel costs, and ongoing labor market pressures continue to keep price growth elevated for now. | ||

| Suggested reading | ||

| Muted Response To Nothing Really Happening, J. Calhoun, Alhambra Investments (February 22, 2026) Stock Market Drives Economy, But For How Much Longer?, R. Forsyth, Barron’s (February 20, 2026) | ||