| ||

| 28th April 2026 | view in browser | ||

| BOJ hawkish hold backs the yen despite oil shock | ||

| Global markets have been trading a softer‑dollar, risk‑on narrative over the past 24 hours, supported by a hawkish‑leaning BOJ hold, elevated ECB‑area inflation expectations, and a large API crude‑oil draw that keeps energy‑driven inflation and geopolitical risk at the core of the macro backdrop. | ||

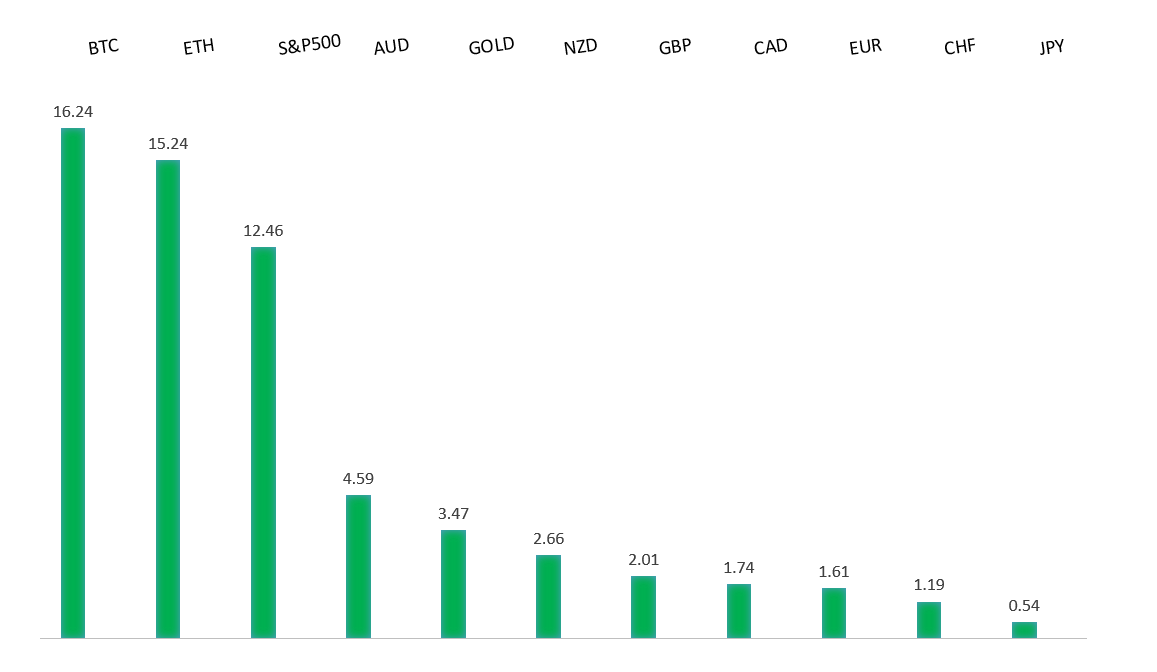

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1850 - 17 April high - Strong R1 1.1800 - Figure - Medium S1 1.1669 - 23 April low - Medium S2 1.1650 - 9 April low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has found support from a mix of inflation repricing and cautious ECB expectations, as persistent Middle East tensions and risks around Strait of Hormuz disruptions have pushed energy prices higher, reinforcing concern about imported inflation in the euro area. While the ECB is still expected to hold rates steady this week, firmer energy-driven inflation risks and sticky core price pressures have encouraged markets to scale back expectations for an aggressive easing path, lending support to the single currency. At the same time, the energy shock complicates the growth outlook, with upcoming euro area GDP data expected to show softer momentum, reinforcing a stagflation-leaning macro backdrop. That tension between inflation vigilance and growth fragility has kept the ECB cautious and helped underpin the euro even as broader downside risks to the regional economy remain in focus. | ||

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 160.46 - 30 March/2026 high - Strong R1 160.03 - 7 April high - Medium S1 158.00 - Figure - Medium S2 157.51 - 19 March low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen has been supported by the BOJ’s hawkish hold, with the bank keeping rates at 0.75% but delivering a 6‑3 split and dissent from three members who wanted a 25 bps hike, while lifting its FY2026 inflation forecast to 2.8%. That has boosted expectations for a more confident path toward further tightening, even as the BOJ still signals caution around the pace of normalization. Support has also come from Tokyo’s reiterated willingness to intervene if the yen weakens abruptly, though Middle East tensions and still‑elevated oil prices are limiting how far the yen can extend gains. With global risk and energy‑price dynamics remaining key watchpoints, the mix of gradual policy normalization, firmer inflation, and geopolitical risk has helped keep the yen bid but capped against a still‑wide U.S.‑Japan yield gap. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7222 - 17 April/2026 high - Strong R1 0.7200 - 27 April high - Medium S1 0.7111 - 23 April low - Medium S2 0.6963 - 8 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar has been supported by a softer U.S. dollar, resilient risk appetite, and the view that the RBA will maintain a relatively hawkish bias against a still-firm domestic inflation backdrop. Support has also come from stabilizing China-linked growth expectations and firm commodity dynamics, with Australia’s terms‑of‑trade outlook remaining constructive despite elevated geopolitical risk. Higher energy prices have reinforced caution about how quickly the RBA can pivot dovish, while the narrowing of expected policy divergence versus the Fed has helped keep Australia’s yield profile attractive. With global growth and geopolitical risks still key watchpoints, the mix of policy support, commodity resilience, and improved external demand sentiment has helped keep the Aussie bid. | ||

| Suggested reading | ||

| The Most Criminally Underrated Investment Idea Today, S. McBride, RiskHedge (April 24, 2026) Aren’t We Making Too Big a Deal About Fed’s Balance Sheet?, J. Tamny, Forbes (April 26, 2026) | ||