| ||

| 20th March 2026 | view in browser | ||

| Dollar drifts lower as ECB turns hawkish | ||

| The US Dollar remains under pressure as markets weigh potential ECB rate hikes driven by inflation risks from the Iran conflict, while softer oil prices and a lighter data calendar help support European currencies and keep focus on whether dollar weakness persists into the week’s close. | ||

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1668 - 10 March high - Strong R1 1.1617 - 19 March high - Medium S1 1.1411 - 13 March/2026 low - Medium S2 1.1400 - Figure - Strong | ||

| EURUSD: fundamental overview | ||

| Euro bulls are trying to reassert. The ECB kept rates unchanged at 2.00% and is taking a cautious, data-dependent approach as the Iran conflict pushes up energy prices, raising inflation risks while weighing on growth. While the ECB believes it is better prepared than in 2022 and expects inflation to rise temporarily before returning to target, markets are pricing in rate hikes—creating a disconnect. For now, the euro is finding some support, but near-term direction will be driven by rate expectations, energy price volatility, and geopolitical headlines. | ||

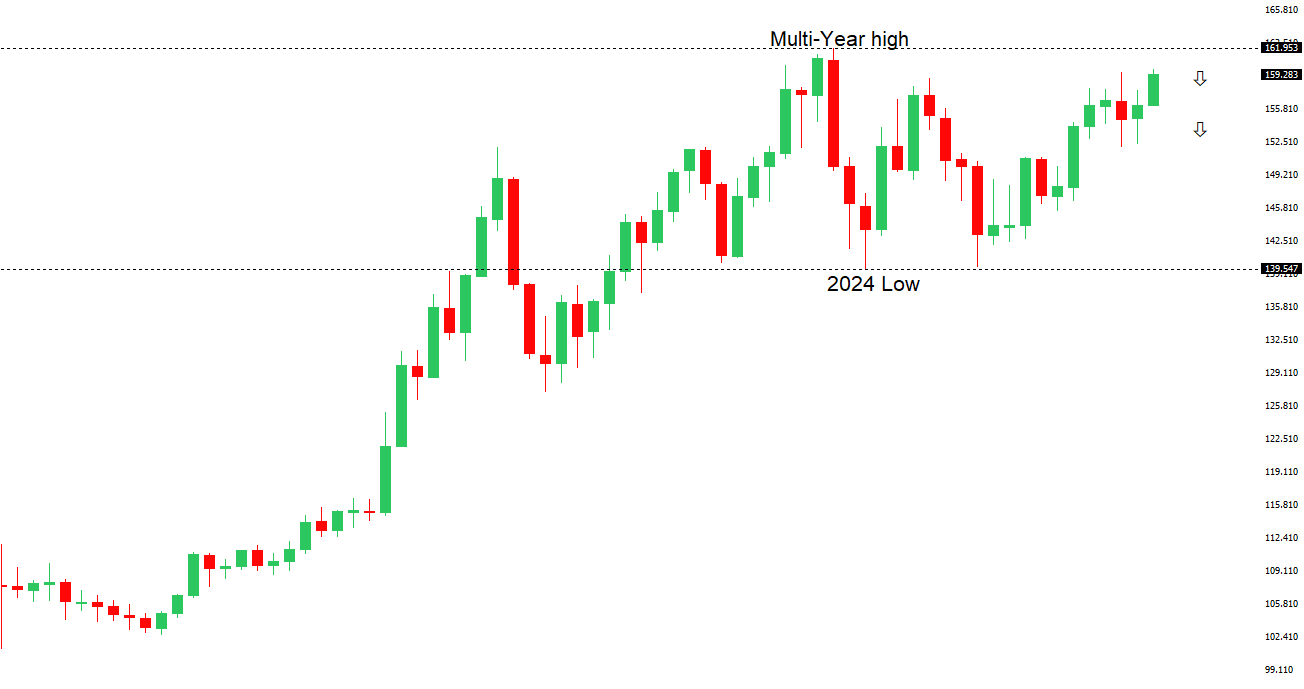

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 160.00 - Psychological - Strong R1 159.91 - 18 March/2026 high - Medium S1 157.27 - 10 March low - Medium S2 156.45 - 5 March low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen is slightly weaker in thin holiday trading, as Japan observes the Vernal Equinox. A meeting between President Trump and PM Takaichi highlighted ongoing tensions in the US-Japan alliance—particularly around military coordination and burden-sharing—despite progress on economic and energy cooperation. Meanwhile, the Bank of Japan kept rates unchanged but signaled a potential hike as soon as April, with policymakers increasingly focused on inflation risks tied to oil and yen weakness. With rising wages, above-target inflation, and the threat of FX intervention near 160, the outlook for USDJPY is becoming more balanced, making aggressive yen bearish positioning less attractive ahead of the next BOJ meeting. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7200 - Figure - Medium R1 0.7188 - 11 March/2026 high - Medium S1 0.6944 - 3 March low - Medium S2 0.6897 - 6 February low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar is heading for a roughly 1.6% weekly gain, remaining close to last week’s near four-year high. Recent labor data shows a still-tight but gradually cooling jobs market, with strong employment growth driven entirely by part-time roles and a rise in participation pushing unemployment slightly higher. Overall, conditions remain firm enough to keep pressure on the RBA to stay hawkish, with markets expecting further rate hikes amid persistent inflation risks. This backdrop should help support the AUD on dips, though softer full-time hiring may limit more aggressive upside. | ||

| Suggested reading | ||

| Can Companies Buy Their Way Into the S&P 500?, S. Wei, Project Syndicate (March 18, 2026) Betting On the Other Side of AI Disruption: Highly Underrated, S. McBride, RiskHedge (March 18, 2026) | ||