| ||

| 19th March 2026 | view in browser | ||

| Central banks take the stage | ||

| The Fed and BOJ held rates steady amid rising inflation and geopolitical uncertainty, lifting the USD and yields, while focus now shifts to today’s ECB and BOE decisions and busy European docket against a backdrop of firm oil prices and mixed global growth signals. | ||

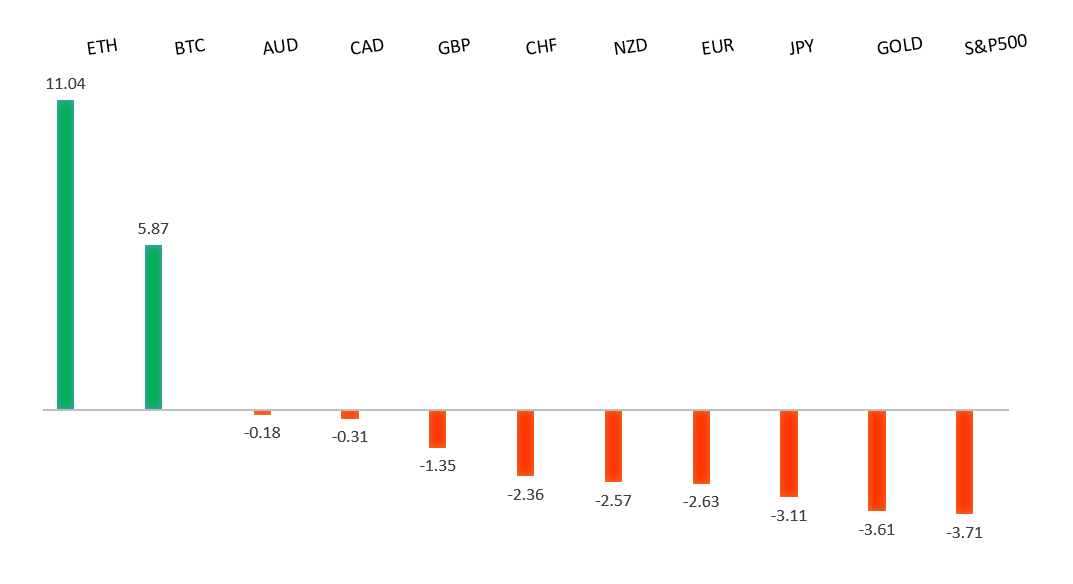

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1668 - 10 March high - Strong R1 1.1575 - 12 March high - Medium S1 1.1411 - 13 March/2026 low - Medium S2 1.1400 - Figure - Strong | ||

| EURUSD: fundamental overview | ||

| The euro is edging slightly higher after yesterday’s drop, which was driven by safe-haven demand for the dollar amid rising Middle East tensions and a less dovish Fed outlook. While February inflation surprised to the upside, it was largely due to temporary factors like Italy’s Winter Olympics, with underlying price pressures still contained—giving the ECB reason to stay cautious. At the same time, renewed energy price spikes tied to geopolitical risks are worsening Europe’s trade outlook and reviving inflation concerns, creating a challenging mix of slower growth and higher prices. Although markets are pricing in tighter ECB policy, the euro remains under pressure as investors weigh higher rates against rising stagflation risks and energy dependence. | ||

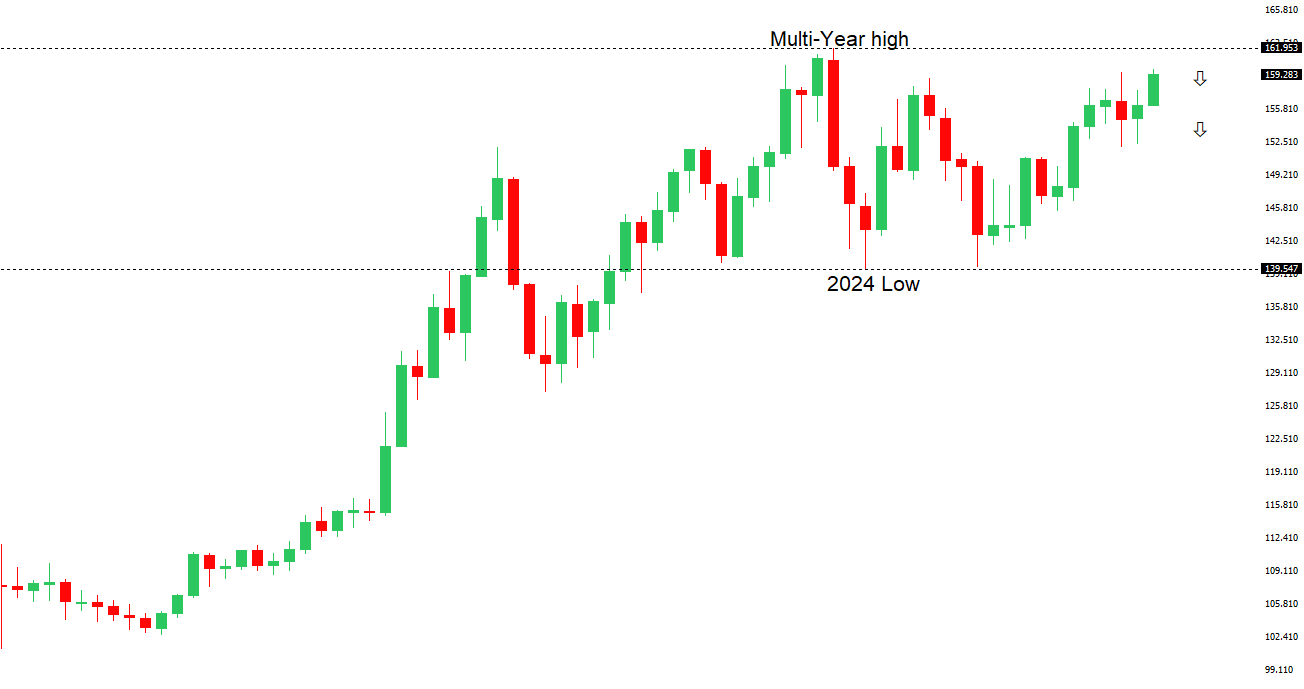

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 160.00 - Psychological - Strong R1 159.91 - 18 March/2026 high - Medium S1 157.27 - 10 March low - Medium S2 156.45 - 5 March low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen strengthened modestly in Asia but remained near the 160 level after the Bank of Japan kept rates unchanged at 0.75% in an 8–1 vote, with one member again pushing for a hike due to inflation risks. The BoJ maintained its accommodative stance while noting uncertainty around Middle East tensions and oil prices, and said future tightening will depend on growth and inflation trends. Rising fuel costs—driven by yen weakness and heavy reliance on imported energy—are adding pressure, even as subsidies aim to limit the impact. Inflation is expected to dip below 2% in the near term before gradually returning to target, with markets now focused on Governor Ueda’s remarks and political developments for further direction. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7200 - Figure - Medium R1 0.7188 - 11 March/2026 high - Medium S1 0.6944 - 3 March low - Medium S2 0.6897 - 6 February low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar edged higher, recovering slightly after the prior session’s sharp drop as markets absorbed a mixed jobs report. While employment rose, the gain was driven by part-time roles and accompanied by a higher unemployment rate, signaling some cooling but not enough to alter expectations for further RBA tightening. Markets still see a strong chance of another rate hike, supporting the AUD alongside Australia’s yield advantage over other major economies. Overall, the currency outlook remains constructive in the near term, though increasingly sensitive to global growth risks, commodity trends, and shifts in central bank policy. | ||

| Suggested reading | ||

| The rise of deepfakes and how to stop them, M. Heikkila, Financial Times (March 19, 2026) The Economy Has Four Problems That the Fed Can’t Fix, N. Goodkind, Barron’s (March 18, 2026) | ||