| ||

| 11th February 2026 | view in browser | ||

| Dovish Fed bets drive global repricing | ||

| Global markets open with a risk-cautious tone as softer US data accelerates a dovish Fed repricing and dollar weakness, investors rotate toward real-earnings exposure, and policymakers from Australia to China grapple with the late-cycle tension between slowing demand and still-uncomfortable inflation dynamics. | ||

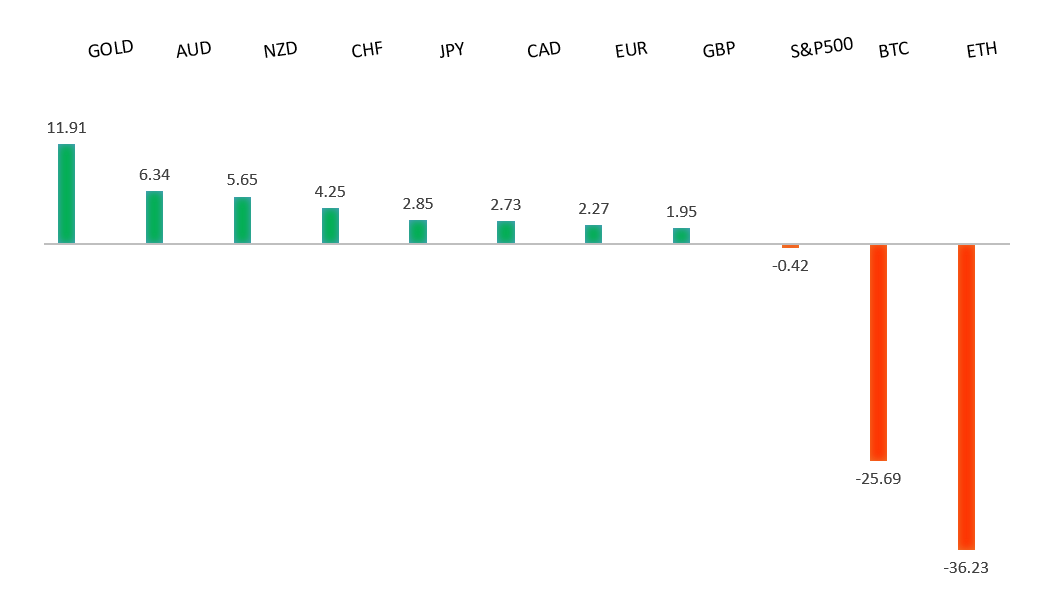

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

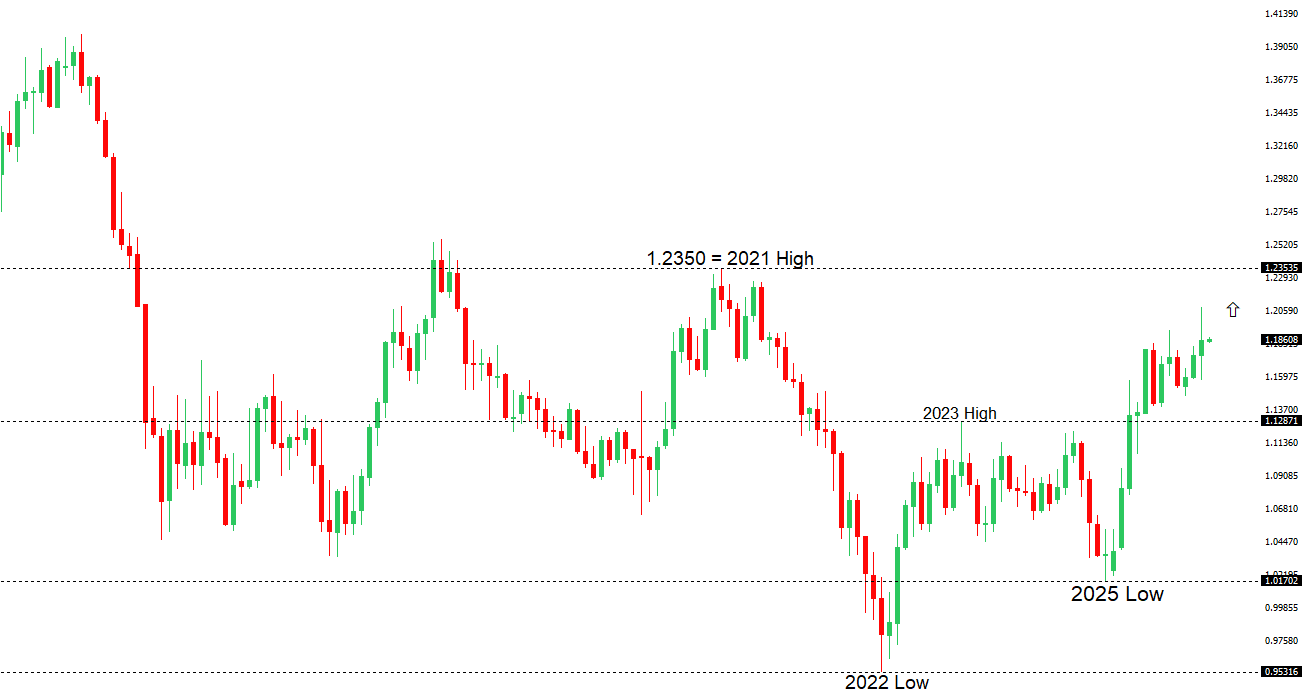

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1500. | ||

| ||

| R2 1.2083 - 27 Janaury/2026 high - Strong R1 1.1929 - 10 February high - Medium S1 1.1765 - 6 February low - Medium S2 1.1728 - 23 January low - Medium | ||

| EURUSD: fundamental overview | ||

| The euro is modestly firmer, retracing Tuesday’s dip while holding most of the sharp rebound from the 1.1766 area, though it has eased slightly after pushing back above 1.19. Recent European Central Bank commentary has played down the euro’s rise as manageable and already factored into baseline forecasts, with inflation near target and little urgency to push back against currency strength. While some officials flag a stronger euro, Chinese imports, and US tariffs as downside risks that could keep inflation undershooting, others warn trade fragmentation may prove inflationary over time—leaving risks finely balanced. Meanwhile, elevated speculative long EUR positioning suggests the currency could be vulnerable to pullbacks if data or ECB messaging disappoints. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. The recent break below 154.39 strengthens the outlook. | ||

| ||

| R2 156.30 - 10 February high - Medium R1 154.52 - 11 February high - Medium S1 152.7 - 29 January low - Medium S2 151.97 - 28 January/2026 low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen has strengthened modestly as softer US data and a weaker dollar allow it to pull back from recent extremes, while optimism around PM Takaichi’s post-election agenda has raised hopes for more durable growth and gradual BOJ normalization. Near term, the yen is still expected to trade with a soft bias rather than slide sharply, despite foreign inflows into Japanese equities that may actually weigh on the currency due to hedging. Further out, however, tighter fiscal discipline, a more constructive JGB backdrop, and a cautious BOJ could help the yen move away from its weakest levels, especially as risks grow around an overcrowded yen carry trade that could unwind if volatility rises. Recent data add nuance: Japan’s January machine tool orders surged on strong overseas demand, highlighting solid global momentum but still-weak domestic activity. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. Setbacks should now be well supported ahead of 0.6300. | ||

| ||

| R2 0.7158 - 2023 high - Strong R1 0.7128 - 11 February/2026 high - Strong S1 0.7005 - 9 February low - Medium S2 0.6897 - 6 February low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar outperformed in Asia, rising about 0.7% to just below a three-year high after RBA Deputy Governor Hauser signaled lingering inflation risks and a still-restrictive policy stance, reinforced by firm housing credit growth. While borrowing remains resilient, softer consumer and business surveys—alongside a December pullback in household spending—point to easing momentum and growing cost-of-living strain. Markets continue to price a year-end cash rate near 4.25%, but expectations are shifting toward a more gradual RBA path if inflation cools further. Positioning shows increased optimism for AUD on yield support, though the currency remains highly sensitive to upcoming inflation, labor, and wage data. | ||

| Suggested reading | ||

| Rather Than Chasing Yesterday’s Winners, Buy Tomorrow’s, E. Fry, InvestorPlace (February 9, 2026) The Robot Revolution Is Real, A. Root, Barron’s (February 8, 2026) | ||