| ||

| 19th February 2026 | view in browser | ||

| Fed caution keeps dollar supported | ||

| The US dollar is firming as Fed officials signal caution on rate cuts amid persistent inflation risks, while global markets digest key economic data, resilient labor trends in Australia, and potential shifts in central bank leadership and policy direction in both the US and Japan. | ||

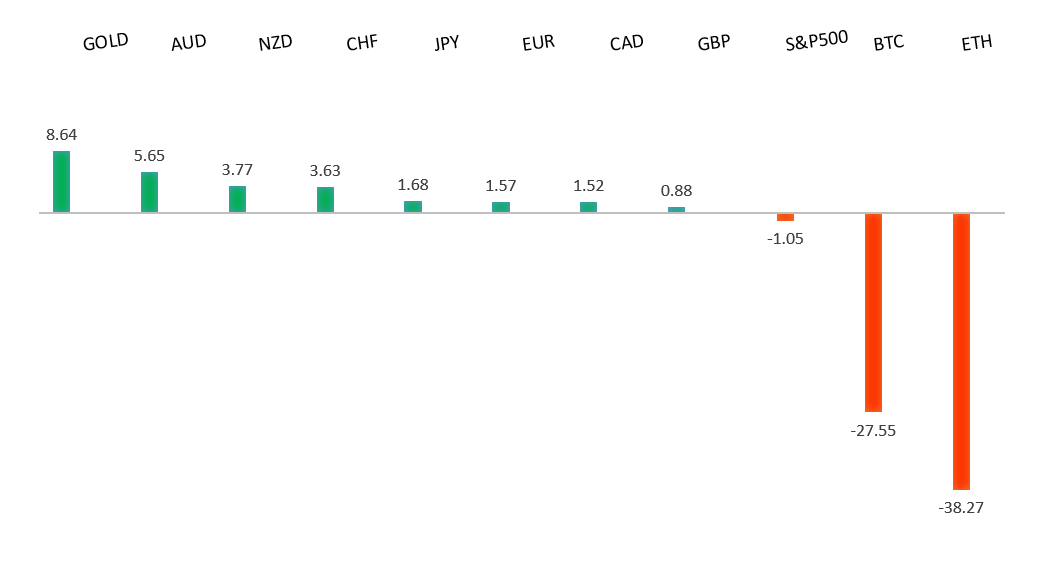

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1500. | ||

| ||

| R2 1.2081 - 27 Janaury/2026 high - Strong R1 1.1929 - 10 February high - Medium S1 1.1765 - 6 February low - Medium S2 1.1728 - 23 January low - Medium | ||

| EURUSD: fundamental overview | ||

| The euro slipped back below 1.18 after hawkish Fed minutes but remains supported above its 50-day moving average, suggesting only a modest near-term softening rather than a shift in trend. The euro faces some headwinds from increasingly dovish ECB signals, elevated positioning, and already strong valuation levels, which may limit upside for now. Still, many analysts view recent weakness as a correction within a broader 2026 uptrend driven mainly by expected dollar softness, with ECB policy likely to remain steady and rate differentials relatively stable in the near term. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. The recent break below 154.39 strengthens the outlook. | ||

| ||

| R2 156.30 - 10 February high - Medium R1 155.35 - 19 February high - Medium S1 152.24 - 12 February low - Medium S2 151.97 - 28 January/2026 low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen has weakened due to hawkish Fed minutes, rising US yields, and firmer oil prices, which increase Japan’s import costs. However, the medium-term outlook still leans modestly supportive for the yen, as expectations of gradual BOJ tightening, narrowing US-Japan rate differentials, and crowded short-yen positioning create conditions for potential strength, especially on dollar pullbacks. Fiscal concerns and JGB volatility could cause intermittent weakness, but improving capex data, policy normalization expectations, and closer US-Japan coordination reinforce a constructive bias for the yen overall, with near-term volatility likely around key policy developments and levels in USDJPY. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7158 - 2023 high - Strong R1 0.7147 - 12 February/2026 high - Strong S1 0.7005 - 9 February low - Medium S2 0.6897 - 6 February low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar has held onto its recent gains near 0.7100 and remains February’s top-performing G10 currency, though stretched positioning suggests limited room for further near-term upside. Analysts expect any pullbacks driven by weaker data or risk aversion to be temporary, with medium-term support coming from the RBA’s relatively hawkish stance as strong labor costs and still-tight employment conditions keep inflation risks elevated. Recent labor data reinforced this view, showing solid full-time job growth and steady unemployment, but signs of slowing employment momentum point to gradual cooling later in 2026. Overall, the AUD remains supported in the short term by yield differentials and policy divergence, though future gains may depend on whether economic strength can be sustained. | ||

| Suggested reading | ||

| Investors Are Getting The US Debasement Trade Wrong, J. Klement, Reuters (February 16, 2026) Miami Still Isn’t The Next Silicon Valley. It’s Weirder, M. Russell, Business Insider (February 18, 2026) | ||