| ||

| 13th April 2026 | view in browser | ||

| Steady but cautious amid ongoing geopolitical risks | ||

| Markets are trading cautiously as Middle East tensions keep oil elevated and support the dollar, reinforcing policy divergence led by resilient US data, while FX, equities, and commodities remain largely driven by geopolitics and energy dynamics amid a relatively light economic calendar. | ||

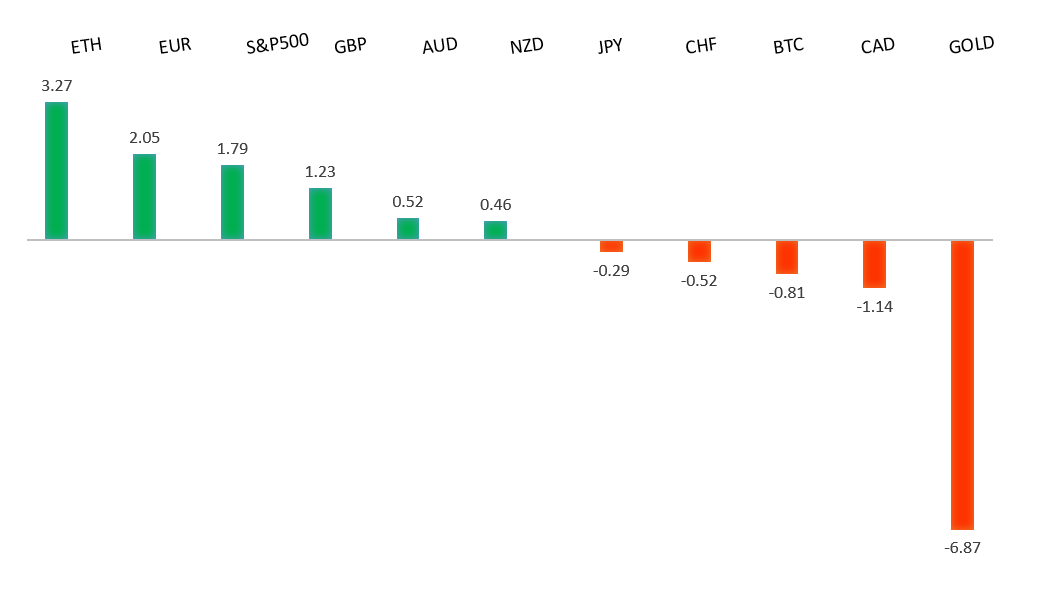

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1740 - 10 April high - Strong R1 1.1700 - Figure - Medium S1 1.1590 - 8 April low - Medium S2 1.1504 - 3 April low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has come under a little pressure as the week gets going, primarily by persistent geopolitical tensions in the Middle East, including the ongoing disruption in the Strait of Hormuz and uncertain ceasefire talks, which have kept oil prices elevated and raised upside risks to eurozone inflation while weighing on regional growth prospects. Stronger-than-expected US economic data, particularly the resilient March labor market report, has reinforced expectations of higher-for-longer Federal Reserve rates amid rising US inflation pressures, widening the policy divergence with the ECB. The ECB’s latest projections show upward revisions to 2026 inflation due to energy costs but a downward revision to growth, with the central bank maintaining rates unchanged while adopting a cautious stance that limits aggressive easing hopes. These fundamentals, combined with broader safe-haven demand for the dollar, have driven the euro’s softer tone. | ||

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 160.46 - 30 March/2026 high - Strong R1 160.03 - 7 April high - Medium S1 157.89 - 8 April low - Medium S2 157.51 - 19 March low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen has softened since the Friday close, pressured by heightened geopolitical tensions in the Middle East and ongoing risks around the Strait of Hormuz, which have lifted energy prices and worsened Japan’s terms of trade as a major importer. At the same time, persistent policy divergence with the Federal Reserve—supported by resilient US data and firmer rate expectations—continues to underpin the dollar, while the Bank of Japan maintains a cautious normalization path amid fragile domestic growth. Together, these dynamics, alongside the dollar’s dominance in attracting safe-haven flows in a higher-yield environment, have reinforced the yen’s weaker tone. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7188 - 11 March/2026 high - Strong R1 0.7095 - 9 April high - Medium S1 0.6963 - 8 April low - Medium S2 0.6833 - 30 March low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar has softened since the Friday close, weighed by ongoing geopolitical tensions in the Middle East and risks around the Strait of Hormuz, which have kept oil prices elevated and dampened global risk sentiment, supporting safe-haven demand for the US dollar. As a high-beta currency, the AUD has been particularly sensitive to this shift, with broader risk aversion offsetting any support from firm commodity prices. At the same time, stronger-than-expected US data, particularly resilient labor market figures, have reinforced higher-for-longer Federal Reserve expectations, widening policy divergence with the Reserve Bank of Australia. China-related sentiment remains an additional headwind, with ongoing uncertainty around the growth outlook limiting upside for Australia’s export-driven economy and further weighing on the currency. | ||

| Suggested reading | ||

| The Investment That Can Shield You in Uncertain Times, J. Zweig, WSJ (April 10, 2026) What 1,000-year-old companies know about resilience, E. Markowitz, Big Think (April 1, 2026) | ||