| ||

| 14th April 2026 | view in browser | ||

| Diplomacy hopes lift mood, oil slips | ||

| Markets enter the day on a cautiously constructive footing as easing geopolitical tensions weigh on oil and the dollar, though sentiment remains tempered by hawkish central bank signals and mixed global data. | ||

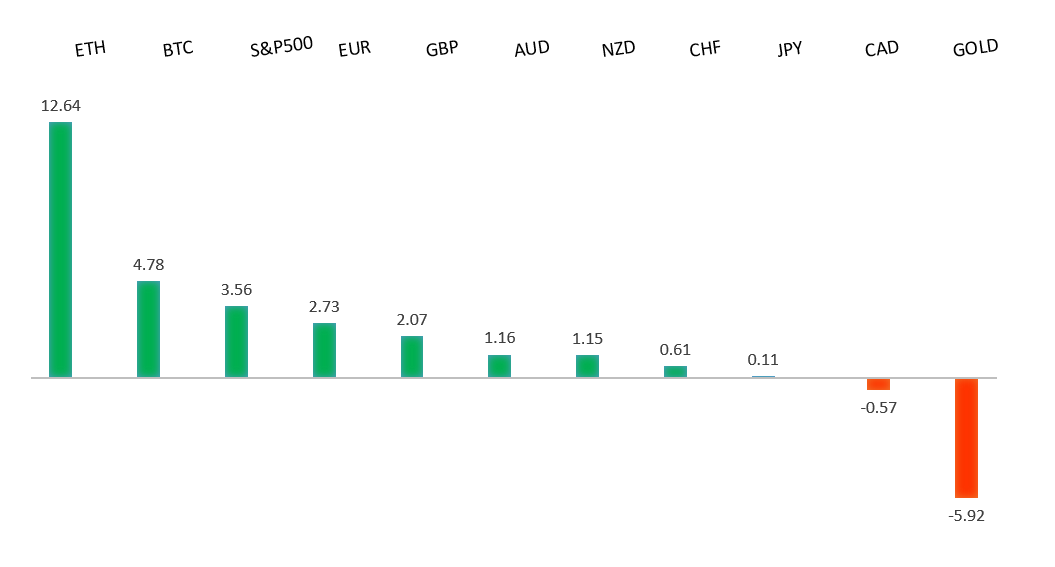

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1835 - 23 February high - Medium R1 1.1796 - 2 March high - Medium S1 1.1650 - 9 April low - Medium S2 1.1589 - 8 April low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has been supported primarily by broad US dollar weakness, extending its gains as markets continue to reassess the Fed outlook amid easing geopolitical tensions and softer oil prices, which have helped stabilize global risk sentiment. While the Eurozone macro backdrop remains fragile, with growth still subdued and the economy sensitive to external shocks, the currency has found relative strength as investors look past near-term softness and focus on a less aggressive policy divergence with the Fed. At the same time, ongoing ECB communication has leaned cautious but steady, reinforcing a data-dependent stance rather than signaling imminent easing, which has helped underpin the euro. | ||

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 160.46 - 30 March/2026 high - Strong R1 160.03 - 7 April high - Medium S1 157.89 - 8 April low - Medium S2 157.51 - 19 March low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen has been trading off a mix of shifting rate expectations and broader global sentiment, with markets increasingly focused on the Bank of Japan after it held rates at 0.75% in March but signaled a tightening bias, fueling speculation of a potential hike as soon as April amid building inflation pressures. At the same time, improved risk sentiment on tentative optimism around a U.S.–Iran resolution has tempered traditional safe-haven demand for the yen, even as ongoing uncertainty keeps downside contained. External drivers remain key, with US rate dynamics in focus ahead of PPI data and a heavy slate of Fed speakers, which could influence yield differentials and near-term direction, leaving the yen caught between a gradually shifting domestic policy backdrop and still-dominant global macro forces. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7188 - 11 March/2026 high - Strong R1 0.7103 - 14 April high - Medium S1 0.6963 - 8 April low - Medium S2 0.6833 - 30 March low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar has been driven by a mix of domestic weakness and shifting global sentiment, with a sharp collapse in Australian business confidence highlighting downside risks to growth and offsetting the impact of still-hawkish rhetoric from the RBA, which continues to flag elevated inflation and the need for tighter policy. Externally, easing geopolitical tensions and softer oil prices have supported a broader improvement in risk sentiment, offering some relief to the AUD, though gains have been limited by ongoing concerns around China’s external sector, where weaker export data points to softer global demand. At the same time, relative currency dynamics have also played a role, with the euro finding support on a weaker US dollar backdrop despite a fragile Eurozone economy still grappling with sluggish growth and energy sensitivity, leaving AUD performance more muted in comparison as markets balance domestic softness against global macro crosscurrents. | ||

| Suggested reading | ||

| Thoughts From The Road: Japan, H. McVey, KKR (April 1, 2026) Satoshi Nakamoto: Mystery Behind Creator of BTC, C. Newkey-Burden, The Week (April 9, 2026) | ||