| ||

| 15th April 2026 | view in browser | ||

| A delicate balance of optimism and risk | ||

| Markets enter the day with a cautiously constructive tone as easing geopolitical tensions weigh on oil and support risk sentiment, while underlying inflation uncertainty and mixed global data keep the outlook balanced. | ||

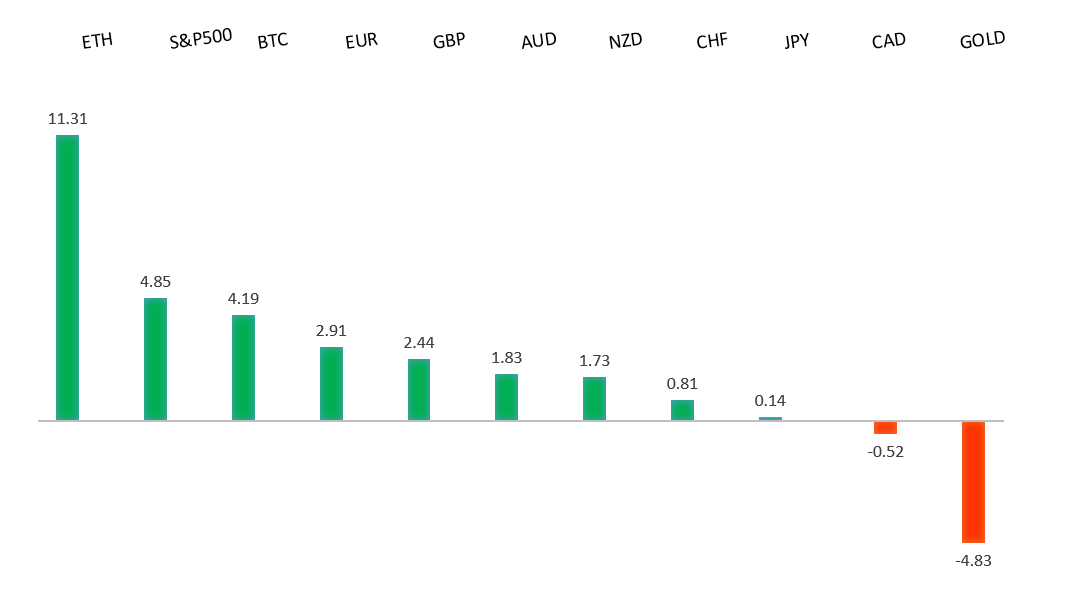

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1835 - 23 February high - Medium R1 1.1812 - 14 April high - Medium S1 1.1650 - 9 April low - Medium S2 1.1589 - 8 April low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has been supported by a combination of broad-based US dollar weakness and shifting expectations around relative central bank policy, with markets increasingly pricing a less hawkish Federal Reserve alongside a more persistent tightening bias from the ECB in response to ongoing inflation pressures, particularly those linked to energy. As geopolitical risks tied to the Iran situation are seen as peaking, the dollar’s safe-haven appeal has diminished, allowing EURUSD to push higher, while the euro has also benefited from the view that Europe may be more responsive in addressing inflation compared to the US. At the same time, evolving energy dynamics and the potential for a changing relationship between oil and the dollar have reinforced the euro’s relative appeal. Looking ahead, Eurozone industrial production data and ECB President Christine Lagarde’s speech will be worth keeping an eye on for further clues around the growth outlook and policy trajectory. | ||

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 160.46 - 30 March/2026 high - Strong R1 160.03 - 7 April high - Medium S1 157.89 - 8 April low - Medium S2 157.51 - 19 March low - Strong | ||

| USDJPY: fundamental overview | ||

| The Bank of Japan’s ultra-accommodative stance, reinforced by Governor Ueda’s cautious tone on normalization and emphasis on the need for sustained wage growth, continues to anchor Japanese yields and preserve the attractiveness of yen-funded carry trades, particularly against a still relatively high US rate environment. At the same time, the yen’s traditional sensitivity to risk aversion has diminished, with markets viewing geopolitical tensions as less likely to escalate into a severe disruption, thereby limiting haven inflows. Stable energy conditions have also helped reduce downside pressure from Japan’s terms of trade, but have not been enough to offset the broader yield differential dynamic, leaving the yen largely driven by external rate expectations and lacking a strong domestic catalyst. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7188 - 11 March/2026 high - Strong R1 0.7148 - 14 April high - Medium S1 0.6990 - 13 April low - Medium S2 0.6833 - 30 March low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar has been driven by a mix of improving global sentiment and a softer US dollar, with easing geopolitical tensions around the Middle East helping to support higher beta currencies and lift AUD toward recent highs. At the same time, the domestic backdrop remains mixed, with inflation still running above target and the RBA maintaining a cautious but relatively hawkish stance, even as signs of slowing momentum emerge across business activity and parts of the labor market. Notably, the currency has been able to shrug off Tuesday’s weak round of Australian confidence data, suggesting external factors are currently dominating. China has also played a role, offering a stabilizing but less dynamic growth impulse as softer trade trends point to weaker external demand. | ||

| Suggested reading | ||

| It’s Hard To Sell When Things Are Great, Buy When Awful, J. Calhoun, Alhambra (April 12, 2026) We’re All Financial Nihilists Now, A. Schrager, Known Unknowns (April 13, 2026) | ||