| ||

| 16th April 2026 | view in browser | ||

| Risk on as geopolitics cool | ||

| Markets are pushing further into risk-on territory with equities at record highs on easing geopolitical tensions and resilient global data, even as underlying inflation and conflict risks keep central banks firmly in wait-and-see mode. | ||

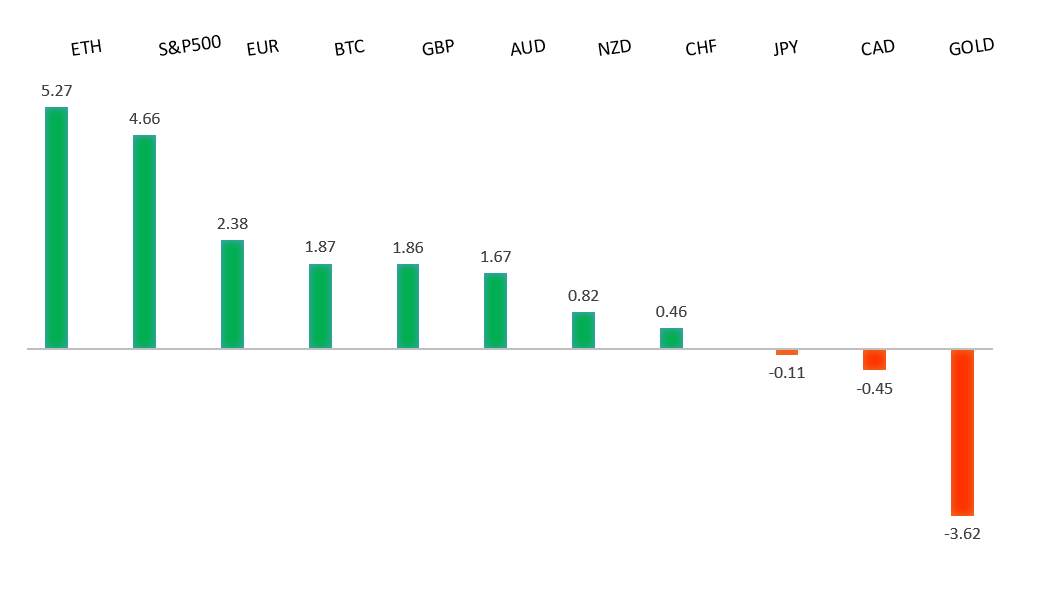

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1835 - 23 February high - Medium R1 1.1824 - 16 April high - Medium S1 1.1754 - 14 April low - Medium S2 1.1650 - 9 April low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has been supported by a combination of external dollar weakness and a relatively steady eurozone backdrop, pushing EURUSD through 1.1800. On the geopolitical front, improved risk sentiment—driven by expectations of further US-Iran negotiations and hopes of avoiding near-term escalation—has reduced safe-haven demand for the dollar, indirectly lifting the euro. This has been reinforced by softer-than-expected US producer price data, which came in well below consensus and tempered Fed tightening expectations, weighing on the USD despite still-solid labor market readings and persistent energy-driven inflation pressures. On the European side, the absence of major negative surprises, alongside steady inflation dynamics around 2.5% and a broadly patient/neutral stance from the ECB, has helped the euro hold firm. Markets appear comfortable that policymakers can remain data-dependent while assessing external shocks, allowing EUR strength to be driven primarily by the shift in relative macro expectations versus the US. | ||

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 160.46 - 30 March/2026 high - Strong R1 160.03 - 7 April high - Medium S1 157.89 - 8 April low - Medium S2 157.51 - 19 March low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen has shown tentative resilience, with USDJPY easing back toward the lower end of its recent range amid a softer US dollar and persistent intervention jitters from Tokyo. Improved geopolitical sentiment—fueled by hopes for progress in US-Iran diplomacy and potential de-escalation steps, including rare Israel-Lebanon talks—has reduced safe-haven demand for the dollar, while a partial retreat in oil prices from recent highs has further tempered expectations for aggressive Fed tightening. At the same time, renewed verbal warnings from Finance Minister Katayama regarding excessive volatility and speculative moves have reinforced market expectations of potential intervention, providing intermittent support to the yen. However, any meaningful or sustained JPY appreciation remains capped by Japan’s acute vulnerability to energy supply disruptions around the Strait of Hormuz, where ongoing restrictions continue to weigh on import costs, the trade balance, and the broader economy despite efforts to tap reserves and diversify routes. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7284 - 3 June high/2022 - Strong R1 0.7198 - 16 April/2026 high - Medium S1 0.7077 - 14 April low - Medium S2 0.6963 - 8 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar has strengthened notably amid a clear improvement in global risk sentiment, with easing geopolitical tensions and a partial retreat in oil prices from recent highs supporting demand for higher-beta currencies and extending the AUDUSD run to a fresh yearly high. The move has been reinforced by a softer US dollar backdrop, as cooling inflation signals and a more cautious Fed tone have tempered expectations for aggressive further tightening, even as policymakers stay alert to lingering oil-driven inflation risks. On the domestic side, Australia’s labor market continues to display resilience, with unemployment holding steady at 4.3% in the latest March data, reinforcing the view that the Reserve Bank of Australia can maintain a tightening bias and helping anchor rate differentials in the Aussie’s favor. | ||

| Suggested reading | ||

| Market Timing Doesn’t Matter As Much As You Think, B. Carlson, AWOCS (April 14, 2026) Why World’s Superrich Are Swapping Dubai for Milan, C. Newkey-Burden, The Week (April 10, 2026) | ||