| ||

| 4th September 2025 | view in browser | ||

| Fed signals cuts amid labor concerns | ||

| Long-end Treasury yields dropped sharply after failing to break 5%, triggered by weaker-than-expected US job openings data that heightened concerns about the labor market. | ||

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1000. | ||

| ||

| R2 1.1789 - 24 July high - Medium R1 1.1743 - 22 August high - Medium S1 1.1583 - 22 August low - Medium S2 1.1392 - 1 August low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro is holding remains well supported, most recently on the back of a weakening US dollar after disappointing US jobs data increased expectations for Federal Reserve rate cuts. In Europe, inflation rose slightly to 2.1% in August, reinforcing predictions that the European Central Bank will maintain current interest rates at its upcoming meeting, though ECB officials have differing views on future rate adjustments. European stocks rebounded, with tech and luxury sectors leading gains, but bond markets remain cautious amid fiscal concerns, particularly in France, where political uncertainty looms ahead of a confidence vote. Eurozone economic activity shows modest growth, with manufacturing improving but Germany’s economy facing challenges from stagnating manufacturing and contracting services. | ||

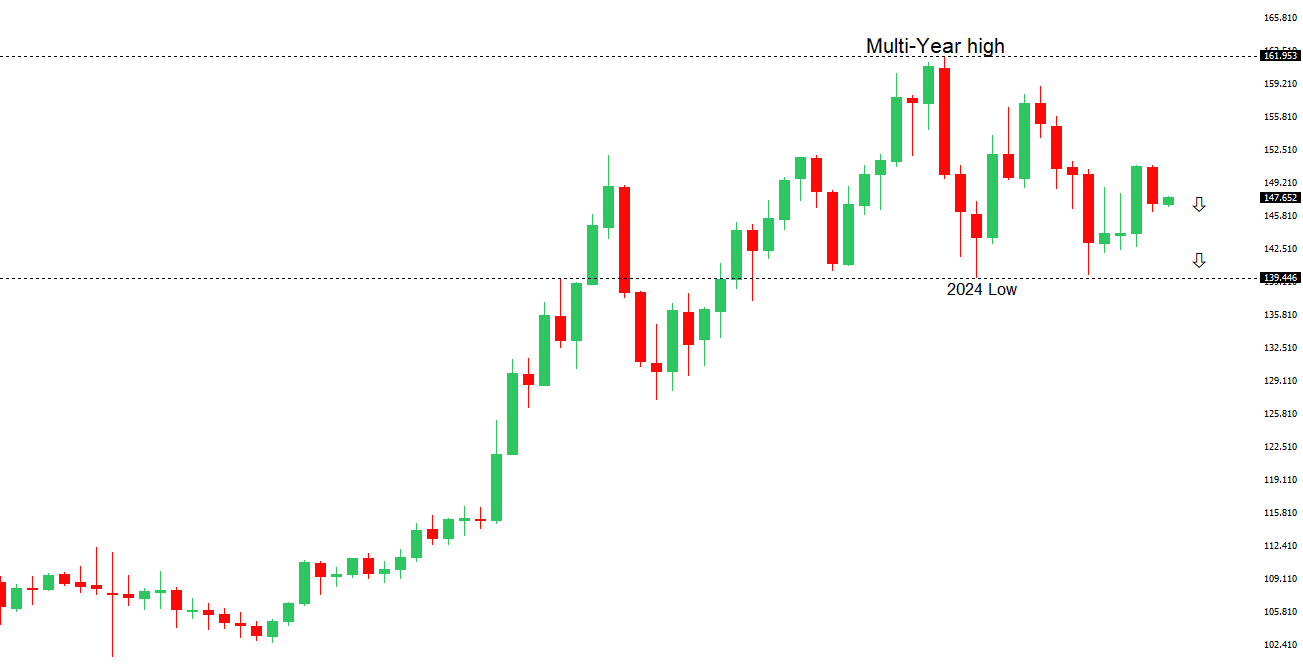

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 152.00. | ||

| ||

| R2 150.92 - 1 August high - Strong R1 149.14 - 3 September high - Medium S1 146.21 - 14 August low - Medium S2 145.85 - 24 July low - Strong | ||

| USDJPY: fundamental overview | ||

| Political uncertainty in Japan, driven by speculation over Prime Minister Shigeru Ishiba’s future and resignations within his party after a poor election performance, is weakening the yen and unsettling financial markets. The Nikkei 225 and Topix indices fell, with the Nikkei down 0.88% and Topix down 1.07%, while bond yields hit near-record highs amid fears of increased fiscal spending. Despite a meeting between Ishiba and Bank of Japan Governor Kazuo Ueda temporarily strengthening the yen, the BOJ’s monetary policy remains unchanged, with rates expected to stay at 0.5% at the next meeting. Upcoming wage data and potential leadership changes, including a possible successor favoring low rates, add further complexity to Japan’s economic outlook. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6600 - Figure - Medium R1 0.6569 - 14 August high - Medium S1 0.6414 - 22 August low - Medium S1 0.6373 - 23 June low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar remained stable, supported by stronger-than-expected economic growth of 0.6% in Q2, surpassing forecasts and driven by increased household spending. Despite this, the S&P/ASX 200 fell 1.8%, with financials and tech stocks leading the decline. Robust growth has led markets to scale back expectations for Reserve Bank of Australia rate cuts, with a quarter-point cut still anticipated in November, while bond yields rose to a one-and-a-half-month high. RBA Governor Michele Bullock highlighted rising consumer spending due to easing inflation and higher house prices but noted global trade uncertainties, particularly U.S. tariffs, as a concern. Sustaining growth may hinge on improving productivity, which remains low at 0.2% annually, challenging the RBA’s inflation target. | ||

| Suggested reading | ||

| A Comical Sound of Silence About Yield Curve, J. Calhoun, Alhambra (September 1, 2025) 7 Reasons to Stop Freaking Out Over the Fed, D. Lefkovitz, Morningstar (September 3, 2025) | ||