| ||

| 10th December 2025 | view in browser | ||

| Global macro at an inflection point | ||

| Global macro is entering a clear inflection point. In the US, the Fed is widely expected to deliver what may be its last 25bp cut for some time, but deeply mixed data and a sharply divided committee mean forward guidance will turn more cautious, with Powell forced to balance slowing labor momentum against stubborn inflation risks. | ||

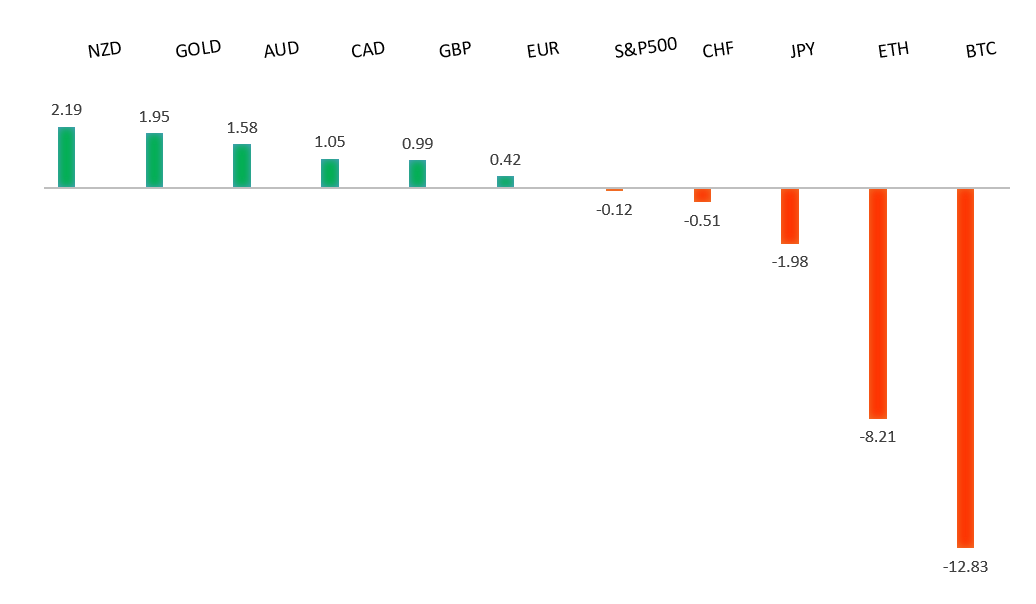

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1729 - 17 October high -Strong R1 1.1682 - 4 December high - Medium S1 1.1547 - 26 November low - Medium S2 1.1469 - 5 November low - Strong | ||

| EURUSD: fundamental overview | ||

| Fabio Panetta says the global monetary system is likely to become more multi-polar, with several major currencies alongside a still-dominant dollar, offering diversification but also higher risks if policy coordination weakens. Europe is trying to strengthen the euro’s global role through better payments, liquidity tools, digital finance, and deeper capital markets, but markets are currently leaning hawkish on ECB policy after comments from Isabel Schnabel, largely pricing out rate cuts in 2026. Even so, some ECB officials still see scope for easing if inflation undershoots or growth weakens, especially as higher US tariffs, a stronger euro, and cheaper Chinese imports could prove disinflationary for the euro area. Geopolitical tensions add further pressure, with President Trump’s comments on Ukraine fueling fears of weaker US–EU coordination, which typically weighs on the euro by increasing risk premiums on European assets. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 ahead of a fresh down-leg back towards the 2024 low at 139.58. | ||

| ||

| R2 158.90 - 20 November/2025 high - Strong R1 157.00 - 28 Figure - Medium S1 154.34 - 5 December low - Strong S2 153.61 - 14 November low - Medium | ||

| USDJPY: fundamental overview | ||

| Governor Ueda signaled that the BOJ is increasingly confident Japan is nearing sustainable 2% inflation, reinforcing expectations of a rate hike to 0.75% at the December 18–19 meeting and a gradual path toward policy normalization. Despite this, the yen has weakened, with USDJPY rebounding from recent lows as markets focus on the upcoming FOMC meeting and the risk that a Fed rate cut comes with hawkish guidance. One Japanese bank notes that ongoing skepticism over whether the BOJ will raise rates to 1% or higher is limiting yen strength, as investors remain reluctant to take large long yen positions without a clearer, more explicitly hawkish signal from the BOJ. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6707 - 17 September/2025 high - Strong R1 0.6655 - 9 December high - Medium S1 0.6520 - 28 November low - Medium S2 0.6421 - 21 November low - Strong | ||

| AUDUSD: fundamental overview | ||

| The RBA left the cash rate unchanged at 3.60% as expected, but its statement and Governor Bullock’s comments signaled a mildly hawkish stance. By highlighting that inflation risks have tilted upward and stressing the Board’s willingness to act if needed, the RBA pushed back against expectations for early rate cuts and kept the door open to further hikes. Bullock reinforced this tone by saying cuts are not foreseeable and that conditions for future hikes were discussed, which supported the Australian dollar; going forward, the AUD should remain resilient, with a hawkish Fed also helping, while a surprise dovish Fed move could spark sharper upside through improved global risk sentiment. | ||

| Suggested reading | ||

| Quiet Millionaires Reveal the Source of Their Wealth, A. Bennett, New York Post (December 8, 2025) What Matters to Investors Going Into ’26, C. Rielly, RiskHedge(December 8, 2025) | ||