| ||

| 30th April 2026 | view in browser | ||

| Hawkish Fed meets rising war risk | ||

| Markets head into Thursday on a defensive footing, with a hawkish Fed tone driving risk-off dollar strength alongside escalating Iran-related geopolitical risks that are pushing oil higher, as attention turns to ECB and BoE decisions for signals on how central banks balance rising inflation pressures against weakening growth. | ||

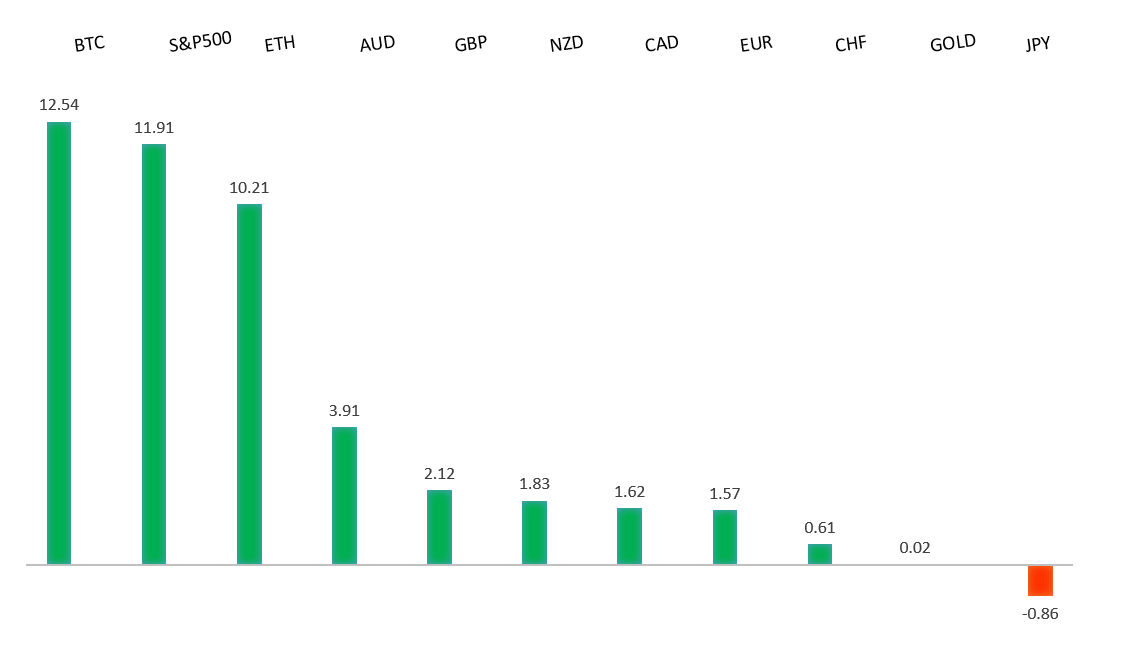

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1850 - 17 April high - Strong R1 1.1755 - 27 April high - Medium S1 1.1650 - 9 April low - Medium S2 1.1589 - 8 April low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has weakened following the FOMC decision, primarily on the back of a stronger US dollar as the Fed delivered a hawkish-leaning hold that reinforced concerns around persistent inflation and reduced expectations for near-term easing. That shift in tone, alongside notable dissent within the Fed, has supported US yields and driven a repricing in favor of the dollar, weighing on EURUSD. At the same time, the euro faces a heavy data and event calendar, including the ECB decision alongside upcoming euro area GDP, inflation and employment releases, with expectations for soft growth and still-elevated price pressures reinforcing a cautious policy backdrop relative to the Fed and leaving the single currency vulnerable in the near term. | ||

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 162.00 negates. | ||

| ||

| R2 161.95 - 2024 high - Very Strong R1 161.00 - Figure - Medium S1 159.51 - 29 April low - Medium S2 158.96 - 28 April low - Medium | ||

| USDJPY: fundamental overview | ||

| The yen has weakened sharply following the FOMC decision, with USDJPY pushing toward multi-year highs as a stronger US dollar and higher US yields reflect the Fed’s hawkish-leaning hold and emphasis on elevated inflation. The move has been reinforced by geopolitical developments, including ongoing Strait of Hormuz blockade risks, which have lifted oil prices and exacerbated Japan’s terms-of-trade pressures as an energy importer. At the same time, while the Bank of Japan maintains a gradual normalization bias, the combination of weaker yen dynamics feeding into inflation and cautious policy messaging has limited support for the currency, leaving near-term price action driven primarily by Fed-BoJ policy divergence, elevated energy costs and rising sensitivity around potential intervention as levels approach those that have previously drawn official concern. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7222 - 17 April/2026 high - Strong R1 0.7200 - 27 April high - Medium S1 0.7101 - 30 April low - Medium S2 0.6963 - 8 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar has come under pressure following the FOMC decision, with AUDUSD sliding as a stronger US dollar reflects the Fed’s hawkish-leaning hold and emphasis on resilient growth and elevated inflation risks tied to energy. The split vote within the Fed and Powell’s messaging have reinforced expectations for a higher-for-longer policy stance, driving a repricing in favor of the dollar and weighing on high-beta currencies like the Aussie. This has been compounded by the broader macro backdrop, where rising oil prices linked to Middle East tensions are adding to global uncertainty and tightening financial conditions. In this context, the Australian dollar is trading more as a proxy for global risk sentiment and policy divergence, leaving it vulnerable to further downside as long as the dollar remains supported and markets reassess the path of US rates. | ||

| Suggested reading | ||

| Another Financial Crisis? Dollar Swaps Are A Bad Sign, W. Munchau, UnHerd (April 27, 2026) The Gulf War’s Economic Fallout: This Is Not The ’70s, M. Ezrati, Quillette (April 27, 2026) | ||