| ||

| 6th January 2026 | view in browser | ||

| Manufacturing soft, markets resilient, risks elevated | ||

| Global markets head into the new day with mixed macro signals and elevated geopolitical risk. In the US, manufacturing activity contracted more sharply in December, reflecting weaker production and inventories, while the Fed appears close to a policy pause as markets price a high probability of rates staying on hold amid slowing labor momentum and easing growth concerns. | ||

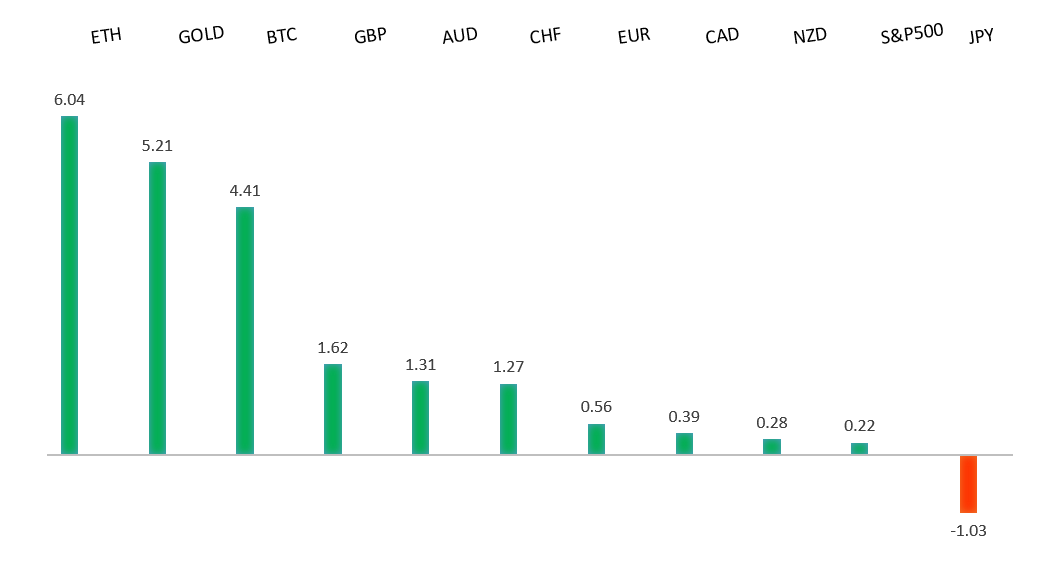

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

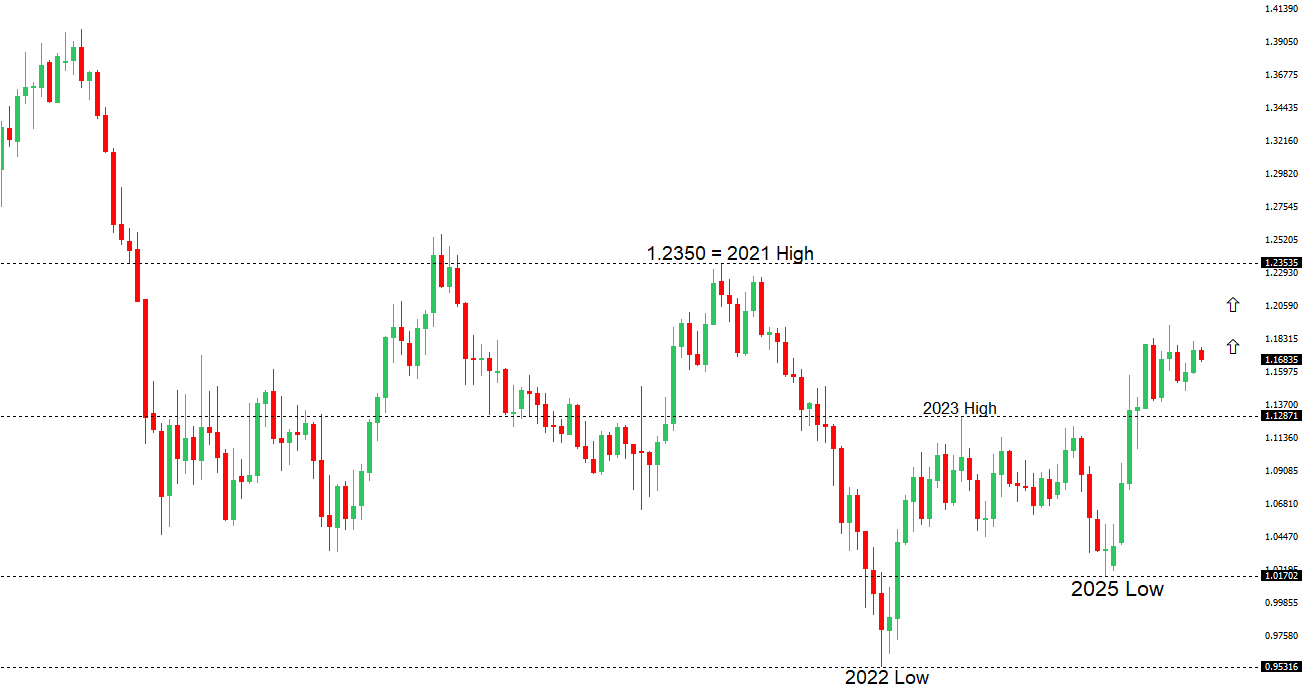

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1400. | ||

| ||

| R2 1.1919 - 17 September/2025 high -Strong R1 1.1765 - 2 Janaury/2026 high - Medium S1 1.1659 - 5 January /2026 low - Medium S2 1.1615 - 9 December low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro is stabilizing after recent lows as the dollar’s rebound faded, with technical signals suggesting the broader bullish trend in EURUSD remains intact despite short-term pressure from safe-haven dollar demand. While geopolitical developments, including Venezuela, have added a brief bearish bias, they could ultimately support the euro longer term by contributing to lower oil prices and a softer, more diversified global reliance on the dollar. Near term, dollar moves should dominate amid heavy US data, with weaker manufacturing data increasing expectations of Fed rate cuts. Looking ahead to 2026, a more dovish Fed, improving eurozone growth, and a still-hawkish ECB—unconcerned about inflation undershooting—continue to underpin a constructive outlook for the euro. | ||

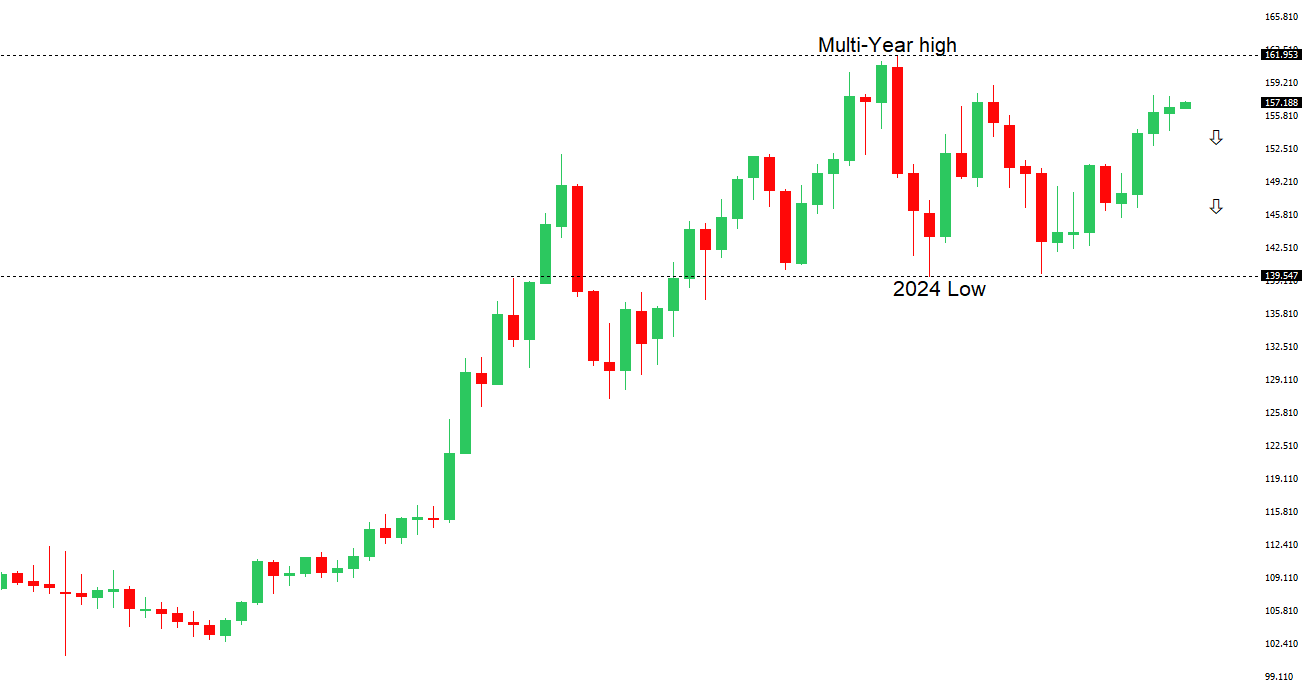

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 ahead of a fresh down-leg back towards the 2024 low at 139.58. A break below 154.39 will strengthen the outlook. | ||

| ||

| R2 157.90 - 20 November/2025 high - Strong R1 157.30 - 5 January /2026 high - Medium S1 155.55 - 24 December low - Medium S2 154.39 - 16 December low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen was broadly steady as high 10-year JGB yields near multi-decade peaks keep attention on fiscal risks and expectations of further BOJ tightening, with markets pricing up to two more 25bp hikes. We expect a mildly yen-supportive tone over the next one to two weeks, favoring consolidation or modest appreciation rather than a clear USDJPY breakout, unless U.S. yields rise sharply or BOJ hawkishness fades. Authorities in both Japan and the U.S. remain uneasy with yen weakness beyond 160, and moves above 158 would raise intervention risks, creating asymmetric pressure against sharp dollar gains. While upcoming wage data may show softer headline growth and weaker real earnings, underlying wage momentum remains firm due to labor shortages and minimum-wage hikes, supporting the BOJ’s view that inflation pressures persist. Recent declines in Japan’s monetary base also reflect the BOJ’s shift away from ultra-easy policy as rates rise and bond purchases are tapered. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6800 - Figure - Medium R1 0.6732 - 6 January/2026 high - Medium S1 0.6660 - 31 December low - Medium S2 0.6592 - 18 December low - Strong | ||

| AUDUSD: fundamental overview | ||

| | ||

| Suggested reading | ||

| Slower Progress Since ’71? Floating Dollar Begs for Attention, J. Tamny, Forbes (January 4, 2026) Important Things That Investors Re-Learned In ’25, Fisher Investments (December 31, 2025) | ||