| ||

| 13th August 2025 | view in browser | ||

| Markets brace for Trump-Putin summit | ||

| On Wednesday, the U.S. dollar ended lower, still influenced by Tuesday’s mild CPI data. Markets are now looking ahead to Friday’s Trump-Putin summit in Alaska. | ||

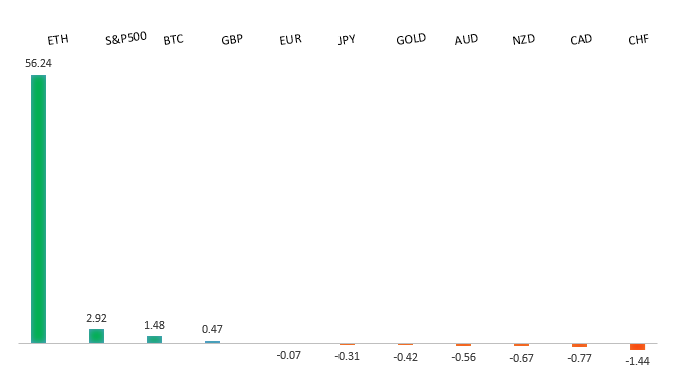

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1000. | ||

| ||

| R2 1.1789 - 24 July high - Medium R1 1.1731 - 13 August high - Medium S1 1.1528 - 5 August low - Medium S2 1.1392 - 1 August low - Strong | ||

| EURUSD: fundamental overview | ||

| The U.S. July CPI data, aligning with expectations, supports predictions of a Federal Reserve rate cut in September, with markets anticipating three cuts by January 2026. Treasury Secretary Bessent urged a significant rate reduction, suggesting the Fed would have acted sooner with earlier access to revised jobs data. Meanwhile, the ECB is likely to hold rates steady in September, with some speculation of a future hike as Germany’s fiscal stimulus grows, highlighting divergent Fed and ECB policies that favor the euro. Hedge funds are increasing bets on the Euro via call options, focusing on upcoming U.S. economic events. ECB officials, including Bundesbank President Nagel, see current rates as appropriate and are cautious about further cuts unless the economy worsens, while also monitoring the impact of new EU-U.S. trade tariffs. The Trump-Putin summit’s outcome could sway the euro, with a peace deal potentially boosting it, but significant concessions or a breakdown in talks could weaken the currency and eurozone markets. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 152.00. | ||

| ||

| R2 150.92 - 1 August high - Strong R1 148.52 - 12 August high - Medium S1 146.62 - 5 August low - Medium S2 145.85 - 24 July low - Strong | ||

| USDJPY: fundamental overview | ||

| Expectations of a U.S. Federal Reserve rate cut in September, fueled by the July CPI data and comments from U.S. Treasury Secretary Bessent urging Japan to tighten monetary policy, have narrowed the yield gap between U.S. and Japanese 2-year bonds, causing USDJPY to fall from its August 12 high. Japan’s upcoming Q2 GDP data, expected to show a rebound to 0.4% growth driven by strong wage growth, tourism spending, and private investment, could further strengthen the yen and support the Bank of Japan’s confidence in raising rates. Despite political uncertainty and low demand for Japanese government bonds signaling investor caution, the BOJ’s hawkish stance on inflation risks suggests a potential rate hike by year-end, though political instability and calls for continued fiscal stimulus may delay policy changes. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6600 - Figure - Medium R1 0.6563 - 13 August high - Medium S1 0.6419 - 1 August low - Medium S1 0.6373 - 23 June low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Reserve Bank of Australia recently cut its cash rate by 25 basis points to 3.60%, expressing optimism about inflation and economic stability, though some analysts are skeptical due to weak productivity and strong wage growth, which could sustain inflation and limit further cuts. While markets expect 1-2 more RBA rate cuts by early 2026, persistent inflation or rising asset prices might force a pause, and the Australian dollar could maintain strength against the US dollar, as markets anticipate more aggressive US Federal Reserve cuts (65bps) compared to the RBA (40bps). Meanwhile, China’s unexpected contraction in lending may accelerate its consumer subsidy program, potentially boosting the AUD through economic spillovers, and upcoming Australian labor data could reinforce expectations of only one more rate cut in 2025, supporting the AUD’s upward trend. | ||

| Suggested reading | ||

| Trump, tariffs and the battle for blue-collar America, J. Sinclair, Financial Times (August 13, 2025) We Are Bullish, But Not Because the Fed Might Cut, Fisher Investments (August 11, 2025) | ||