| ||

| 25th August 2025 | view in browser | ||

| Political turmoil in France pressures Euro | ||

| The euro faced significant pressure on Monday due to political uncertainty in France, where Prime Minister François Bayrou called for a confidence vote on September 8 to support his government’s unpopular debt reduction plan, risking its collapse after just nine months. | ||

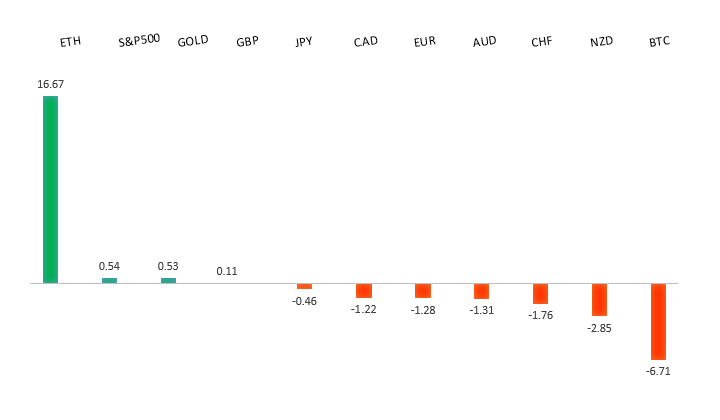

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1000. | ||

| ||

| R2 1.1789 - 24 July high - Medium R1 1.1743 - 22 August high - Medium S1 1.1583 - 22 August low - Medium S2 1.1392 - 1 August low - Strong | ||

| EURUSD: fundamental overview | ||

| The European Central Bank is adopting a cautious “wait-and-see” approach, keeping interest rates steady at 2.15% for main refinancing and 2% for the deposit facility, as inflation hits the 2% target and may dip lower due to a strong euro and falling energy prices. Unlike the U.S. Federal Reserve, which is leaning toward easing, the ECB is hesitant to cut rates further unless growth or inflation weakens significantly, with markets expecting minimal chance of a cut before year-end. Recent data shows the eurozone economy, particularly Germany, displaying modest growth and resilience, with the German IFO business climate index rising to 89.0 in August, the highest since 2023, despite ongoing structural challenges and trade disruptions. ECB officials, including President Christine Lagarde, remain optimistic about steady growth and minimal impact from U.S. tariffs, with no immediate plans for additional rate cuts unless risks materialize. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 152.00. | ||

| ||

| R2 150.92 - 1 August high - Strong R1 148.52 - 12 August high - Medium S1 146.21 - 14 August low - Medium S2 145.85 - 24 July low - Strong | ||

| USDJPY: fundamental overview | ||

| At the Jackson Hole symposium, Bank of Japan Governor Kazuo Ueda expressed confidence that Japan’s tight labor market will drive wage growth and sustain inflation, citing demographic constraints as a key factor for medium-term inflation stickiness. Despite core inflation at 3.1%, Ueda remained cautious, noting it’s still below the BOJ’s target, though markets are increasingly expecting a rate hike by October, with odds rising above 42%. Upcoming Tokyo inflation data and other economic indicators could further support these expectations, while narrowing U.S.-Japan yield spreads and a dovish Fed shift may pressure the USDJPY exchange rate. Meanwhile, Prime Minister Shigeru Ishiba’s rising approval ratings suggest political stability, potentially reinforcing the BOJ’s gradual policy normalization, though weak department store sales and a cooling Services Producer Price Index highlight ongoing challenges for Japan’s retail sector and economic recovery. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6600 - Figure - Medium R1 0.6569 - 14 August high - Medium S1 0.6414 - 22 August low - Medium S1 0.6373 - 23 June low - Strong | ||

| AUDUSD: fundamental overview | ||

| Westpac suggests maintaining long positions in AUDUSD, as factors like China’s economic stimulus and risks to the US dollar’s credibility support a gradual rise in the Australian dollar. China’s policies, including liquidity injections and lower interest rates, boost demand for Australian exports, strengthening the Australian Dollar. Meanwhile, the US dollar faces challenges from political instability and erratic policies. Australia’s upcoming CPI reports, particularly in August, could influence the AUD’s near-term path, but the Reserve Bank of Australia is likely to hold rates steady in September, with potential cuts in November 2025 and February 2026. | ||

| Suggested reading | ||

| If Trump Economy Is “Booming,” Then It Doesn’t Need The Fed, J. Tamny, Forbes (August 24, 2025) Why the Fed’s Long Pause May Extend the Market Rally, F. Yue, MarketWatch (August 25, 2025) | ||