| ||

| 25th August 2025 | view in browser | ||

| Powell hints at rate cuts as economy cools | ||

| Federal Reserve Chair Jerome Powell’s recent Jackson Hole speech signaled a dovish shift, strongly suggesting a potential rate cut at the September FOMC meeting. | ||

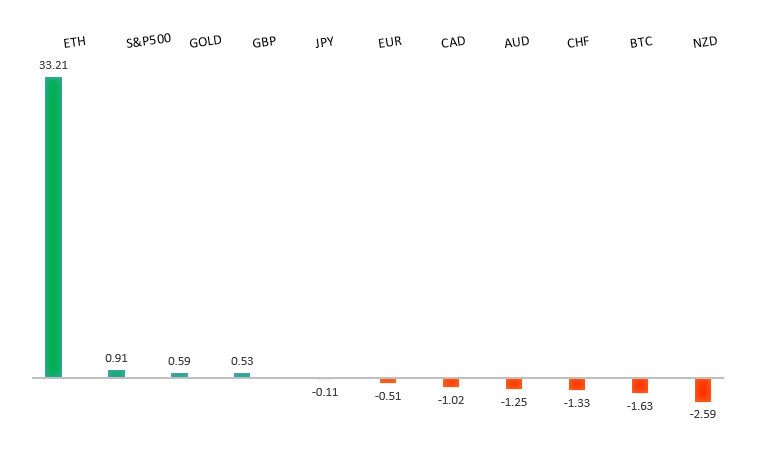

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1000. | ||

| ||

| R2 1.1789 - 24 July high - Medium R1 1.1743 - 22 August high - Medium S1 1.1583 - 22 August low - Medium S2 1.1392 - 1 August low - Strong | ||

| EURUSD: fundamental overview | ||

| Federal Reserve Chair Powell is leaning toward rate cuts to support employment, with markets expecting an 84% chance of a cut in September and three by early 2026, while the European Central Bank remains cautious, holding rates at 2.15% and 2% with a “wait-and-see” approach due to stable 2% inflation and steady growth. Eurozone wage growth at 3.95% year-on-year exceeds ECB forecasts, but officials anticipate moderation and see no urgent need for further cuts, supported by a resilient labor market that grew 4.1% since 2021. ECB President Lagarde emphasized labor market strength but noted uncertainties from automation and AI, while warning against political interference in central bank decisions. Upcoming Eurozone data, including economic confidence and German business and consumer surveys, will provide further insights. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 152.00. | ||

| ||

| R2 150.92 - 1 August high - Strong R1 148.52 - 12 August high - Medium S1 146.21 - 14 August low - Medium S2 145.85 - 24 July low - Strong | ||

| USDJPY: fundamental overview | ||

| Strong U.S. economic data recently lowered expectations for a Federal Reserve rate cut in September, dropping from a near-certain 100% to 72%, though Fed Chair Powell’s Jackson Hole speech surprised markets by supporting rate cuts due to labor market concerns, weakening the dollar against G10 currencies. Meanwhile, Japan’s persistent inflation and tight labor market, with core inflation at 3.1%, have fueled speculation of a Bank of Japan rate hike by October, as Governor Kazuo Ueda highlighted wage growth and structural inflation drivers. Markets anticipate gradual BOJ policy tightening, boosting Japanese yields and the yen, while upcoming U.S. rate cuts may drive capital flows to Japan. Key Japanese data this week, including unemployment, Tokyo inflation, industrial production, retail sales, and consumer confidence, will provide further insight. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6600 - Figure - Medium R1 0.6569 - 14 August high - Medium S1 0.6414 - 22 August low - Medium S1 0.6373 - 23 June low - Strong | ||

| AUDUSD: fundamental overview | ||

| Federal Reserve Chair Powell’s dovish comments at the Jackson Hole symposium, emphasizing employment risks and potential rate cuts, led to a drop in Treasury yields and a risk-on market sentiment, boosting the Australian dollar as AUD-US yield spreads widened. Markets have largely priced in the Reserve Bank of Australia’s recent dovish stance, limiting further downside for the Australian Dollar unless new surprises emerge. Attention now turns to Australia’s July CPI report on August 27, which could influence near-term Aussie movements, though the RBA is likely to hold rates steady in September, with a potential cut in November, while U.S. data will play a bigger role in Aussie trends. | ||

| Suggested reading | ||

| AI Is Providing Disruption That Education Really Needs, S. McBride, RiskHedge (August 22, 2025) Markets Are Pleased Powell Didn’t Ignite a Fire In the ‘Hole’, P. O’Hare, Briefing (August 22, 2025) | ||