| ||

| 30th June 2026 | view in browser | ||

| Quarter-end flows challenge the dollar, not the narrative | ||

| Quarter-end rebalancing and improving risk sentiment have sparked a modest pullback in the US dollar against the euro and pound, but markets remain anchored by the broader themes of Fed hawkishness, resilient US growth and easing energy prices as attention turns to central bank signals and key economic data later this week. | ||

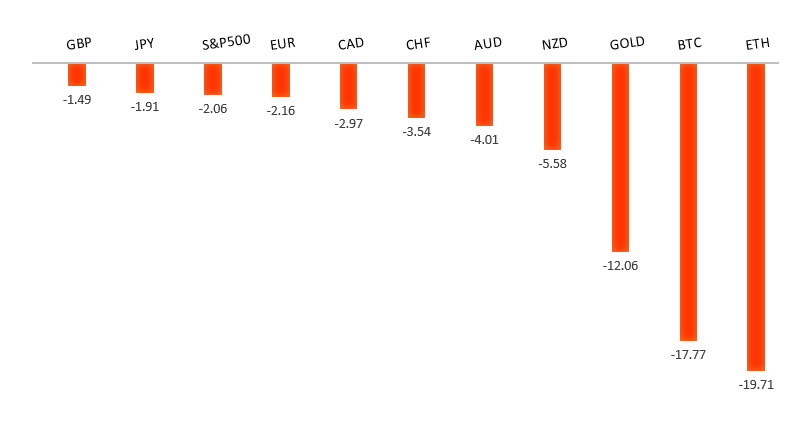

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1529 - 18 June high - Medium R1 1.1440 - 23 June high - Medium S1 1.1325 - 24 June/2026 low - Medium S2 1.1300 - Figure - Medium | ||

| EURUSD: fundamental overview | ||

| The euro has regained some footing as broad US Dollar weakness, improving regional sentiment and renewed confidence in the Eurozone investment story offset lingering geopolitical uncertainty. Markets are increasingly focused on this week’s ECB Forum in Sintra, where ECB President Christine Lagarde struck a notably hawkish tone by warning that future inflation shocks are likely to become more frequent while emphasizing that the Eurozone’s greater economic resilience gives the ECB room to raise rates again if necessary without threatening financial stability. That has reinforced expectations that the ECB will remain willing to keep policy restrictive should inflation reaccelerate, lending support to the single currency. Meanwhile, stronger-than-expected Eurozone economic sentiment has helped ease concerns over the region’s growth outlook ahead of key German inflation and retail sales data, with a firmer-than-expected HICP reading likely to further bolster the euro by supporting higher-for-longer rate expectations. Beyond monetary policy, falling energy prices following signs of easing tensions around the Strait of Hormuz have improved the outlook for European growth and corporate earnings, while renewed investor diversification away from concentrated US AI exposure has driven fresh inflows into European equities, providing an additional tailwind for the euro even as markets continue to monitor upcoming US labor market data for the next catalyst in EURUSD. | ||

| GBPUSD: technical overview | ||

| The Pound remains exceptionally well supported on dips into the 1.3000 area, with the price largely consolidating above the psychological barrier and previous resistance turned support in the form of the 2023 high. Look for the market to continue be well supported on dips ahead of the next major upside extension through the yearly high at 1.3870 and towards a retest of the 2018 high at 1.4377 further up. Only a monthly close below 1.3000 negates. | ||

| ||

| R2 1.3325 - 18 June high - Medium R1 1.3274 - 22 June high - Medium S1 1.3140 - 24 June/2026 low - Medium S2 1.3100 - Figure - Medium | ||

| GBPUSD: fundamental overview | ||

| The pound has found renewed support as broad US Dollar weakness offsets lingering domestic uncertainty, allowing GBPUSD to recover toward multi-day highs. Sterling has also benefited from easing concerns over UK fiscal policy after expected incoming Prime Minister Andy Burnham pledged to maintain Chancellor Rachel Reeves’ fiscal rules and adhere to Labour’s existing fiscal framework, reassuring investors following a prolonged period of political instability. At the same time, improving sentiment surrounding a temporary easing in US-Iran tensions has supported broader risk appetite and weighed on the safe-haven US Dollar. However, upside for the pound remains tempered by expectations that the Bank of England will continue easing policy gradually as UK growth slows and inflation pressures continue to moderate. Attention now turns to a busy week of catalysts, including the UK’s first-quarter GDP data, the ECB’s Sintra Forum, comments from new Fed Chair Kevin Warsh, and crucial US labor market data, all of which will shape expectations for the relative policy outlook between the Bank of England and the Federal Reserve. | ||

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped below 162.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 162.00 negates. | ||

| ||

| R2 163.00 - Figure - Medium R1 161.99 - Multi-Year high/29 June 2026 - Very Strong S1 160.41 - 18 June low - Medium S2 159.54 - 11 June low - Strong | ||

| USDJPY: fundamental overview | ||

| The Yen remains under pressure as the wide interest rate differential between Japan and the United States continues to favor the US Dollar, although gains in USDJPY have become more cautious as the pair trades just below the closely watched 162.00 level. Markets remain highly alert to the risk of official intervention after repeated warnings from Japanese authorities that they stand ready to respond to excessive one-sided currency moves, helping to temper further Yen weakness. At the same time, investors are focused on this week’s key US data—including ISM surveys, JOLTS, ADP employment and, most importantly, Thursday’s US nonfarm payrolls report—which will shape expectations for the Federal Reserve’s policy path after markets further increased pricing for additional tightening. Domestically, stronger Japanese commercial sales and retail activity have offered some evidence of resilient demand, while renewed trade tensions with China following additional export controls on Japanese firms have added to geopolitical uncertainty and reinforced a modest risk premium for the Yen. Even so, persistent capital outflows, bearish market positioning and the dominant influence of broad US Dollar strength continue to outweigh supportive domestic factors, leaving USDJPY trading near multi-decade highs while intervention risks remain elevated. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7089 - 15 June high - Strong R1 0.6979 - 11 June low - Medium S1 0.6875 - 26 June low - Medium S2 0.6833 - 30 March low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian Dollar remains under pressure, with AUDUSD slipping below 0.6900 as investors continue to reassess the Reserve Bank of Australia’s policy outlook despite lingering inflation concerns. Attention is firmly on the release of the RBA’s June meeting minutes, which are expected to provide greater insight into how high the bar is for another rate hike after the Bank unanimously left the cash rate unchanged at 4.35% while retaining an explicit tightening bias. Although policymakers continue to stress that inflation remains too high and have kept the option of further tightening alive, slowing economic growth and signs that previous rate increases are working have tempered expectations for imminent action, leaving markets questioning how hawkish the RBA will ultimately prove to be. At the same time, China remains a key swing factor for the Aussie, with upcoming PMI data expected to offer an important read on demand from Australia’s largest trading partner, where stronger activity would support the currency while softer figures would reinforce downside risks. Broader external factors are also playing a major role, with shifting expectations around US monetary policy, global risk sentiment and developments in the Middle East continuing to drive day-to-day price action. While easing geopolitical tensions have helped stabilize overall market sentiment, the combination of cautious RBA expectations, a still-resilient US Dollar backdrop and fading speculative positioning has left the Australian Dollar struggling to regain momentum despite domestic economic fundamentals remaining relatively resilient. | ||

| Suggested reading | ||

| A renewable energy revolution, L. Boulton Financial Times (June 29, 2026) A Wave of Fed Interest Rate Cuts That May Never Come, R. Ross, Marketwatch (June 25, 2026) | ||