| ||

| 4th August 2025 | view in browser | ||

| Rate cut fever grips markets after weak US jobs | ||

| Global markets kick off the week on the back foot following a sharp repricing of U.S. rate expectations after Friday’s soft jobs data and ISM employment reading, which came in at its lowest since mid-2020. | ||

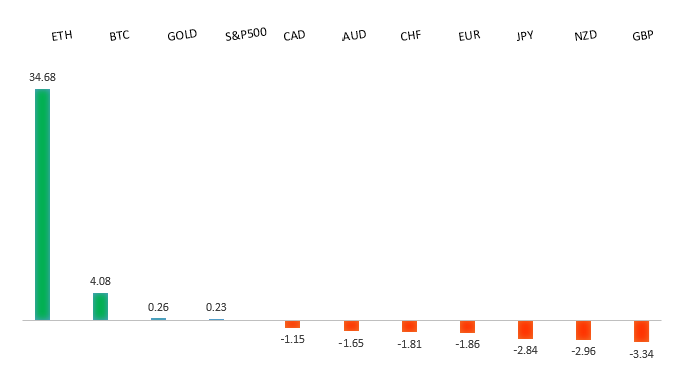

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1000. | ||

| ||

| R2 1.1703 - 25 July low - Medium R1 1.1600 - Figure - Medium S1 1.1392 - 1 August low - Medium S2 1.1210 - 29 May low - Strong | ||

| EURUSD: fundamental overview | ||

| Last week’s slightly higher German inflation and stable Euro area inflation aligned with ECB targets, suggesting the ECB may be nearing the end of its rate-cutting cycle. A weaker US jobs report last Friday triggered a sharp EURUSD rebound, as hopes for earlier Fed rate cuts grew, with some analysts predicting a potential 50bps cut in September if US labor markets weaken further. The euro outperformed most G10 currencies, boosted by unwinding short positions, while ECB official Christodoulos Patsalides highlighted the eurozone’s resilience despite global tensions and a US-EU trade deal, emphasizing data-dependent ECB policy. One institutional shop noted potential eurozone growth challenges from the trade deal’s 15% tariff but expect the euro to rise against a weakening dollar as global portfolios diversify. This week’s key Eurozone data includes the August Sentix Investor Confidence, June PPI, June Retail Sales, and the ECB Economic Bulletin, offering insights into monetary policy and economic projections. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 152.00. | ||

| ||

| R2 150.92 - 1 August high - Strong R1 149.00 - Figure - Medium S1 147.06 - 4 August low - Medium S2 145.85 - 24 July low - Strong | ||

| USDJPY: fundamental overview | ||

| Last week, the USDJPY rose due to Japan’s political instability, a hawkish U.S. Federal Reserve, and the Bank of Japan’s unchanged 0.5% interest rate despite a higher 2.7% inflation forecast for 2025. A disappointing U.S. jobs report reversed this trend, triggering a dollar sell-off and erasing the week’s gains as traders exited long USDJPY positions. Looking ahead, markets will monitor Japan’s upcoming wage and household spending data, BOJ meeting minutes, and a 30-year JGB auction, alongside U.S. employment and inflation indicators, for signals on future rate changes. Political uncertainty in Japan and potential Fed policy shifts could further influence yen volatility, with USDJPY maintaining a bullish bias above 145.76-145.86, though a dovish Fed shift may weaken the dollar against G10 currencies. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6688 - 7 November 2024 high - Strong R1 0.6625 - 24 July/2025 high - Medium S1 0.6419 - 1 August low - Medium S1 0.6373 - 23 June low - Strong | ||

| AUDUSD: fundamental overview | ||

| Last Friday, G10 currencies, particularly the Yen and Euro, rallied against the dollar due to weaker-than-expected U.S. labor data, boosting expectations for a Federal Reserve rate cut in September, though Trump’s tariff announcements tempered gains for antipodean currencies, which saw the smallest increase. In Australia, Q2 CPI data came in slightly below expectations, supporting a likely 25bps rate cut by the RBA in August, with inflation aligning with RBA projections and the unemployment rate at 4.3% still near full employment. Strong June retail sales (up 1.2% MoM) and building approvals (up 11.9% MoM) suggest resilient consumer spending and a potential housing sector recovery, but Bloomberg notes spending growth was driven by discounts and may not be sustainable, with markets anticipating at least two RBA rate cuts this year unless economic strength prompts a pause. | ||

| Suggested reading | ||

| The World’s 50 Most Valuable Private Companies, M. Lu, Visual Capitalist (July 31, 2025) Top 10 Jobs Least And Most Threatened By AI, N. Rothschild, Axios (July 31, 2025) | ||