| ||

| 26th September 2025 | view in browser | ||

| Strong U.S. data challenges rate cut hopes | ||

| Recent U.S. economic data, including a robust 3.8% GDP growth in Q2, a surprising 2.9% rise in durable goods orders, and lower-than-expected jobless claims at 218,000, indicate a strong economy, reducing the urgency for rapid Federal Reserve rate cuts. | ||

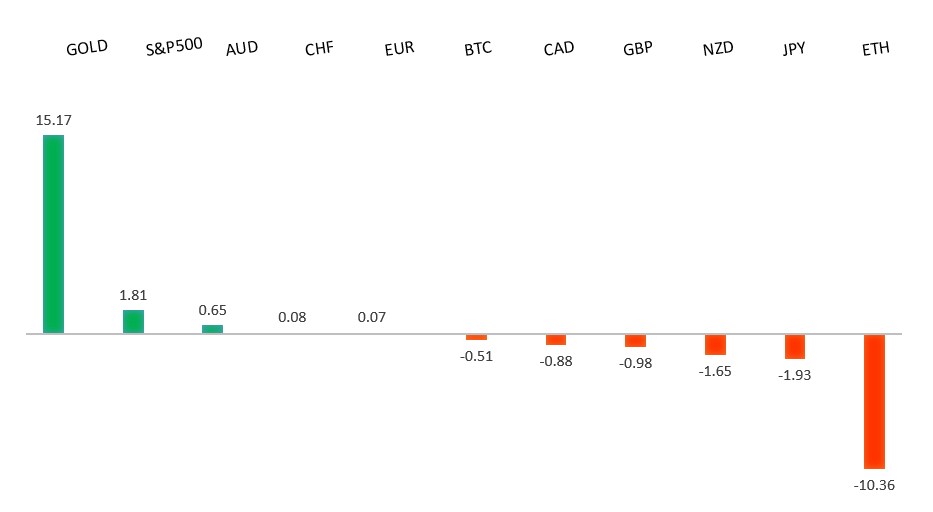

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1919 - 16 September/2025 high -Strong R1 1.1820 - 23 September high - Medium S1 1.1646 - 25 September low - Medium S2 1.1574 - 27 August low - Strong | ||

| EURUSD: fundamental overview | ||

| Some economists now predict the European Central Bank will likely maintain its 2.00% deposit rate through 2025 and 2026, as inflation remains under control, though a small rate cut is possible. Bloomberg Economics notes that while hawkish views currently dominate, trade uncertainties, potential U.S. tariffs, and signs of economic weakness could shift ECB policy toward a rate cut, with timing being the main uncertainty. Recent German consumer confidence data shows slight improvement (-22.3 vs. forecast -23.3), driven by rising income expectations, but ongoing concerns about jobs and inflation keep sentiment fragile, impacting the broader eurozone outlook. Upcoming ECB data suggests inflation expectations are stabilizing near the 2% target, with 1-year CPI at 2.50% and 3-year at 2.40%, reflecting effective monetary policy and easing inflation pressures. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 152.00. | ||

| ||

| R2 150.92 - 1 August high - Strong R1 149.96 - 26 September high - Medium S1 147.46 - 23 September low - Medium S2 145.48 - 17 September low - Strong | ||

| USDJPY: fundamental overview | ||

| Tokyo’s September CPI held steady at 2.5% year-on-year, below the expected 2.8%, with core inflation measures also at 2.5%, down from 3.0% previously, signaling a slowdown in inflationary pressure. Despite inflation remaining above the Bank of Japan’s 2% target, the softening data reduces expectations for immediate rate hikes, though a 25 basis point increase by year-end remains possible. Japan’s 40-year bond auction saw strong demand, lowering yields to 3.31%, reflecting market stability amid political transitions and reduced volatility. The BOJ’s next moves may hinge on global economic trends, particularly U.S. jobs data, which could influence USDJPY, currently testing but struggling to break the 150 level. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6707 - 17 September/2025 high - Strong R1 0.6660 - 18 September high - Medium S1 0.6526 - 25 September low - Medium S1 0.6483 - 2 September low - Strong | ||

| AUDUSD: fundamental overview | ||

| Australia’s job vacancies fell by 2.7% quarter-on-quarter, a sharp contrast to the previous 2.8% rise, signaling a cooling labor market. August data showed a net loss of 5,400 jobs, with full-time jobs dropping significantly while part-time roles increased. Despite this, the Reserve Bank of Australia views the labor market as near full employment and is likely to maintain a cautious approach, balancing employment support with inflation, which is now at 3.6% within the target range. Economists predict limited rate cuts, possibly 50 basis points, but the upcoming RBA meeting will be key for hints on faster monetary easing. | ||

| Suggested reading | ||

| The Bond Market Isn’t Buying The AI Hype, M. Hulbert, MarketWatch (September 25, 2025) Five Pearls of Wisdom From a Legend of Financial Writing, R. Lieber, NY Times (September 23, 2025) | ||