| ||

| 25th September 2025 | view in browser | ||

| Powell stays cautious on rate cuts | ||

| Federal Reserve Chair Jerome Powell, in a recent speech, expressed caution about aggressively cutting interest rates, citing persistent inflation concerns and a need for a data-dependent approach, despite acknowledging a slowing labor market. | ||

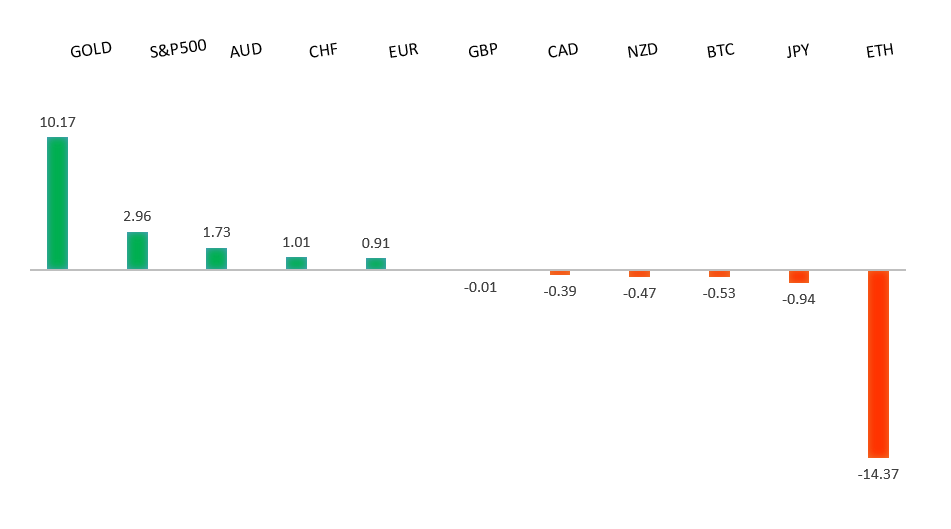

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1919 - 16 September/2025 high -Strong R1 1.1849 - 18 September high - Medium S1 1.1700 - Figure - Medium S2 1.1660 - 11 September low - Medium | ||

| EURUSD: fundamental overview | ||

| German business confidence unexpectedly declined in September 2025, with the Ifo expectations index dropping to 89.7, reflecting skepticism about Chancellor Friedrich Merz’s economic recovery plans, as borrowed funds were directed more toward consumption than modernization. The manufacturing sector faces challenges from external pressures like U.S. tariffs on EU goods, while structural issues such as pension reform and bureaucracy remain unaddressed, dimming hopes for a robust recovery. Meanwhile, German consumer confidence is expected to slightly improve to -23.3 in October but remains low due to concerns over the economy, job security, and inflation. The European Central Bank is advancing plans for a digital euro by 2029 to enhance payment sovereignty, though legislative hurdles and member-state agreements are still needed. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 152.00. | ||

| ||

| R2 150.92 - 1 August high - Strong R1 149.14 - 3 September high - Medium S1 146.28 - 16 September low - Medium S2 145.48 - 17 September low - Strong | ||

| USDJPY: fundamental overview | ||

| Sanae Takaichi, a key contender in Japan’s LDP leadership race, has softened her previously dovish stance on monetary policy, emphasizing that while the government sets broad economic goals, the Bank of Japan should independently determine policy details. She cautions against rapid rate hikes due to potential harm to corporate investment but acknowledges Japan’s stable bond market, driven by strong domestic ownership. Despite her shift, analysts expect the BOJ to proceed with rate hikes as early as October, supported by persistent inflation above the 2% target and solid wage growth, with upcoming Tokyo CPI data likely to reinforce this outlook. Meanwhile, Japan’s Finance Ministry will cut super-long bond issuance to ease market pressure, a move seen as slightly positive for bond market stability and the yen, though broader fiscal credibility remains a concern amid political uncertainty. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6707 - 17 September/2025 high - Strong R1 0.6660 - 18 September high - Medium S1 0.6546 - 8 September low - Medium S1 0.6483 - 2 September low - Strong | ||

| AUDUSD: fundamental overview | ||

| RBA Governor Michele Bullock indicated that Australia’s economy is performing as expected or slightly better, with inflation within the 2–3% target and unemployment near full employment. The RBA remains focused on controlling inflation, leading to a cautious market outlook, though a November rate cut is still anticipated. A recent “productive” Xi-Trump call has improved US-China relations, potentially boosting high-beta currencies like the Australian dollar if tensions continue to ease. Despite a 2.7% decline in job vacancies and a net job loss in August, the RBA is likely to maintain a balanced approach, with economists expecting only a modest 50 basis point rate cut due to limited labor market slack. | ||

| Suggested reading | ||

| Bangladesh’s missing billions, stolen in plain sight, Financial Times (September 11, 2025) Amid Divide Within the FOMC, Making Sense of ‘Dot Plot’, N. Goodkind, Barron’s (September 19, 2025) | ||