| ||

| 13th May 2026 | view in browser | ||

| Higher yields and geopolitical tension keep risk appetite in check | ||

| Markets are being driven by a reinforcing loop of sticky inflation and elevated yields supporting the dollar, while geopolitical tensions around energy supply and cautious US-China dynamics are keeping risk assets fragile and commodities volatile. | ||

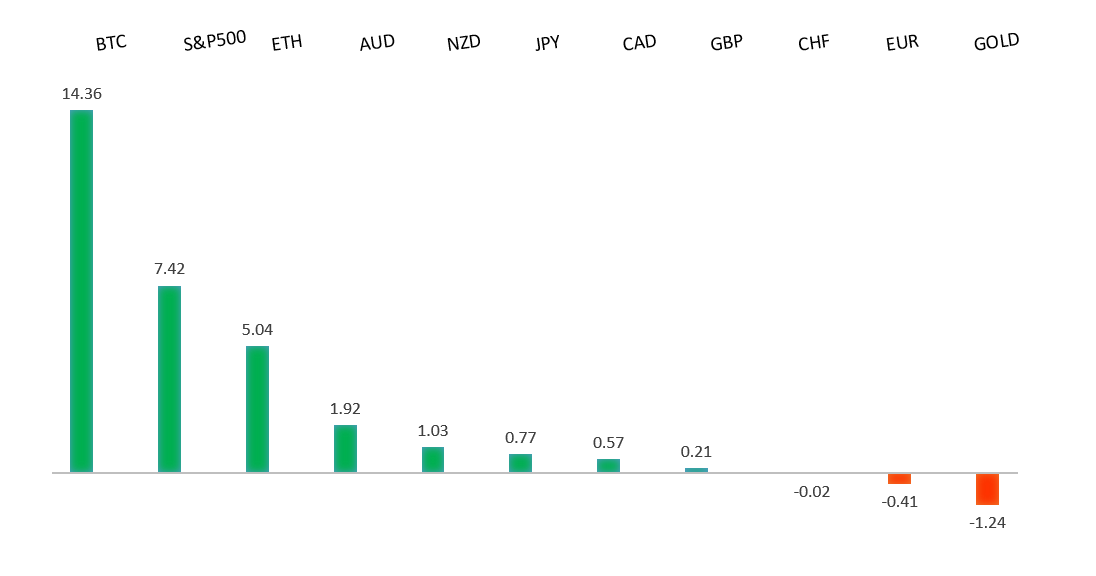

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1850 - 17 April high - Strong R1 1.1797 - 6 May high - Medium S1 1.1650 - 9 April low - Medium S2 1.1589 - 8 April low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has come under renewed pressure, slipping back below the 1.1750 level, primarily as stronger-than-expected US inflation data has reinforced the divergence in policy expectations between the Federal Reserve and the ECB. A hotter April US CPI print (3.8% YoY, the highest since May 2023) has revived bets that the Fed may need to keep rates higher for longer or even tighten further, boosting the dollar and weighing on EURUSD. On the European side, while ECB rhetoric has turned more hawkish—with policymakers like Joachim Nagel and Martin Kocher flagging rising risks from energy prices and geopolitical tensions—the market still sees a more gradual tightening path relative to the US. Even with pricing for a near-term ECB hike firming, the euro is struggling to gain traction as relative yield dynamics, ongoing geopolitical uncertainty tied to energy markets, and softer growth momentum in the Eurozone continue to act as headwinds against a backdrop of resilient US data. | ||

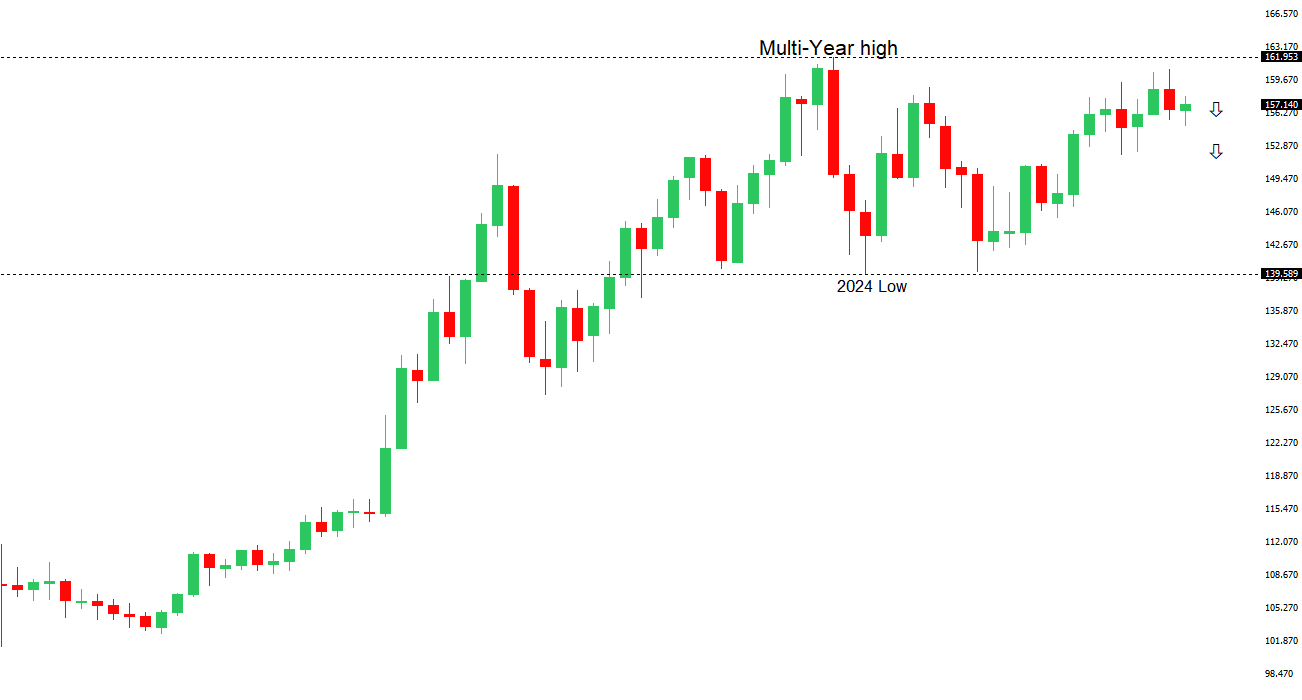

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 159.53 - 17 April low - Medium R1 157.93 - 6 May high - Medium S1 156.00 - Figure - Medium S2 155.02 - 6 May low - Strong | ||

| USDJPY: fundamental overview | ||

| The Yen has remained under pressure, even as the policy backdrop in Japan turns incrementally more hawkish, with markets still focused on the persistent yield differential versus the US. While the latest current account data showed a record surplus—highlighting strong external balances—this has failed to translate into Yen strength, suggesting capital outflows and rate differentials continue to dominate. The Bank of Japan’s April Summary of Opinions reinforced expectations for further rate hikes, with some policymakers open to near-term tightening amid inflation risks tied to higher energy prices, and external projections such as from the OECD pointing to a gradual normalization path toward 2% policy rates by 2027. However, this tightening trajectory remains slow and cautious relative to the still-restrictive stance of the Federal Reserve, where hotter US CPI data has pushed back expectations for rate cuts and reinforced “higher-for-longer” pricing. As a result, USDJPY continues to be driven primarily by US yields and global risk dynamics, with geopolitical tensions and safe-haven flows offering only limited and inconsistent support to the Yen. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7300 - Figure - Medium R1 0.7278 - 6 May/2026 high - Medium S1 0.7101 - 30 April low - Medium S2 0.6963 - 8 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian Dollar has been drawing support from a more hawkish shift at the Reserve Bank of Australia, with the central bank’s recent move to lift rates to 4.35% reinforcing a still-active tightening bias and underpinning yield support for the currency. At the same time, the Aussie continues to trade as a China proxy, leaving it sensitive to developments around US–China trade relations, with markets closely focused on the Trump–Xi summit and ongoing negotiations, where any constructive tone could further lift AUD sentiment. On the external side, stronger-than-expected US inflation has revived some Fed tightening expectations, lending the US Dollar intermittent support and tempering AUD upside, while near-term direction is also being shaped by incoming US data—particularly PPI—as well as broader risk appetite dynamics tied to global growth and trade headlines. | ||

| Suggested reading | ||

| When Money Isn’t Abundant, People Aren’t Stupid, J. Calhoun, Alhambra (May 10, 2026) It’s Not Over: Why the S&P 500 Is On the Way to 8,000, J. Sonenshine, Barron’s (May 8, 2026) | ||