| ||

| 6th February 2026 | view in browser | ||

| US labor cracks shake risk | ||

| Markets open with FX largely steady and sterling firmer, but renewed weakness in US labor data has rattled risk sentiment, deepening US equity underperformance and refocusing attention on growth, policy, and emerging AI-driven labor risks. | ||

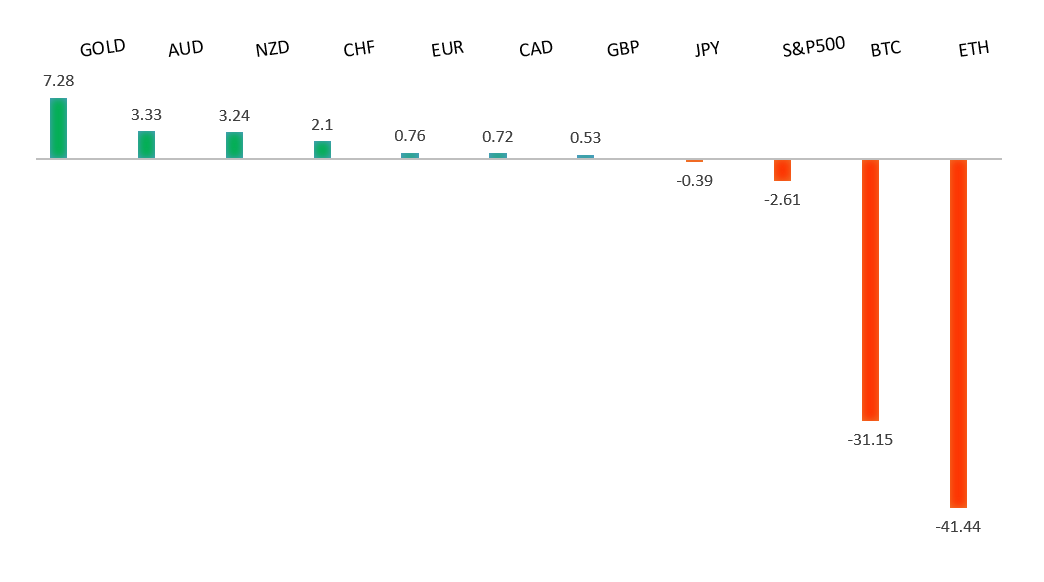

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

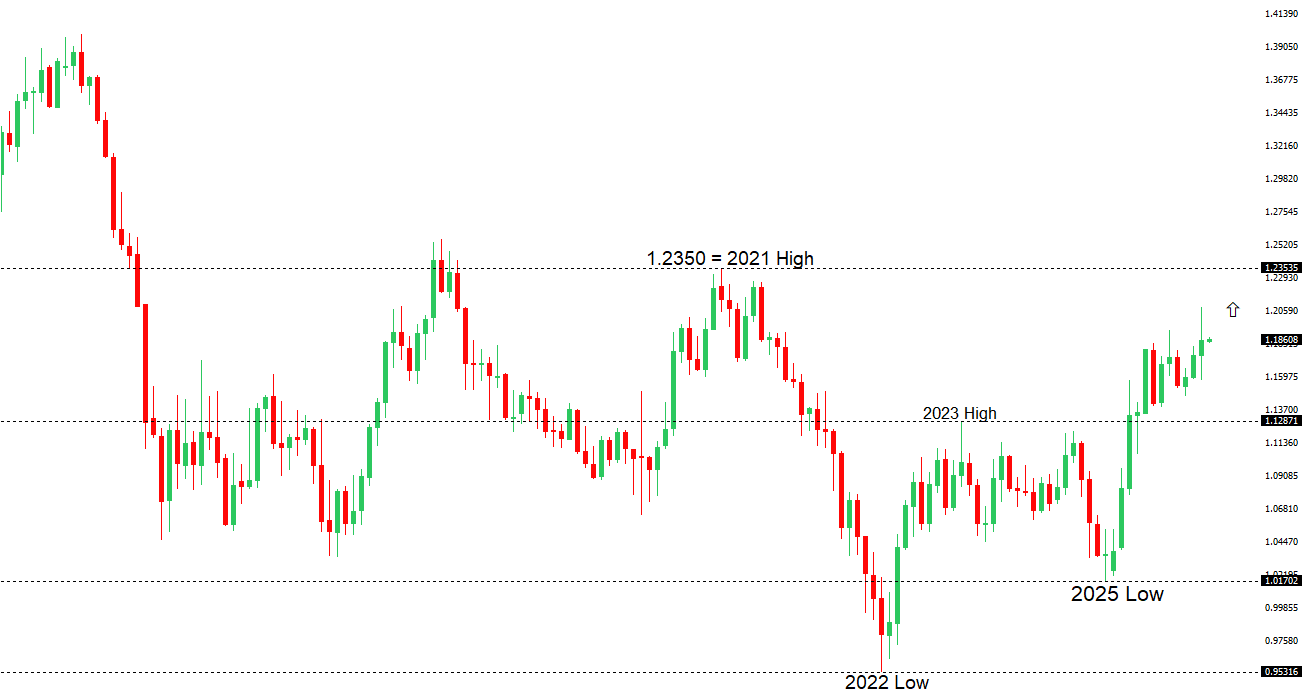

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1500. | ||

| ||

| R2 1.2083 - 27 Janaury/2026 high - Strong R1 1.1875 - 2 February high - Medium S1 1.1765 - 6 February low - Medium S2 1.1728 - 23 January low - Medium | ||

| EURUSD: fundamental overview | ||

| The euro is modestly higher on the day but still set for a weekly loss as markets reassess growth and policy amid renewed trade risks. The European Central Bank left rates unchanged at 2% and struck a patient, data-dependent tone, saying policy is in a “good place” even as uncertainty rises from fresh tariff threats by President Trump and ongoing geopolitical tensions. With inflation soft but growth holding up—helped by fiscal support in Germany—markets see little chance of near-term ECB moves, while expectations of further easing from the Federal Reserve underpin a constructive medium-term EURUSD outlook, with several banks still looking for a gradual move back toward the low-1.20s over the next year as rate gaps narrow and reserve managers diversify into euros on dips. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. The recent break below 154.39 strengthens the outlook. | ||

| ||

| R2 157.42 - 19 January low - Strong R1 157.34 - 5 February high - Medium S1 154.55 - 2 February low - Medium S2 151.97 - 28 January/2026 low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen edged firmer into the close as investors stayed cautious ahead of Japan’s Lower House election, wary of fiscal risks and reluctant to push USDJPY higher despite solid demand at a 30-year JGB auction. While stronger bond buying helped long-end yields ease, it hasn’t meaningfully supported the yen, with markets still focused on the prospect of looser fiscal policy and only gradual BOJ normalization. Meanwhile, December household spending fell much more than expected, underscoring fragile consumer demand and reinforcing expectations that the BOJ will struggle to tighten aggressively—supportive for JGBs but a headwind for sustained yen strength. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. Setbacks should now be well supported ahead of 0.6300. | ||

| ||

| R2 0.7158 - 2023 high - Strong R1 0.7095 - 29 January/2026 high - Strong S1 0.6897 - 6 February low - Medium S2 0.6834 - 23 January low - Medium | ||

| AUDUSD: fundamental overview | ||

| The Aussie dollar is stabilizing after Thursday’s sharp drop, supported by Australia’s recent rate hike, still-elevated inflation, and a backdrop of higher yields, steady growth, and a positive current account—all of which argue for a firmer currency over time. Near-term pressure from the global tech selloff has weighed on high-beta FX, but markets continue to price further RBA tightening, while China’s steady mid-4% growth outlook and resilient commodity demand remain key external supports. With the yuan expected to strengthen modestly and capital flows rotating toward higher-yielding, resource-linked currencies, AUDUSD has scope to move back toward 0.71, especially given that the Aussie still looks undervalued versus long-run fair-value estimates once risk sentiment settles. | ||

| Suggested reading | ||

| The Real European Financial Threat To The US, P. Subachhi, FT Alphaville (February 6, 2026) Consumers Sending the Investor Clear Market Message, M. Hulbert, Marketwatch (February 3, 2026) | ||