| ||

| 5th February 2026 | view in browser | ||

| Central banks take center stage | ||

| Markets open with central banks in focus as the European Central Bank and the Bank of England are set to hold rates, the dollar’s bounce looks corrective rather than trend-changing, and investors balance soft European growth signals with resilient US labor data and strong Asia-Pacific bond demand. | ||

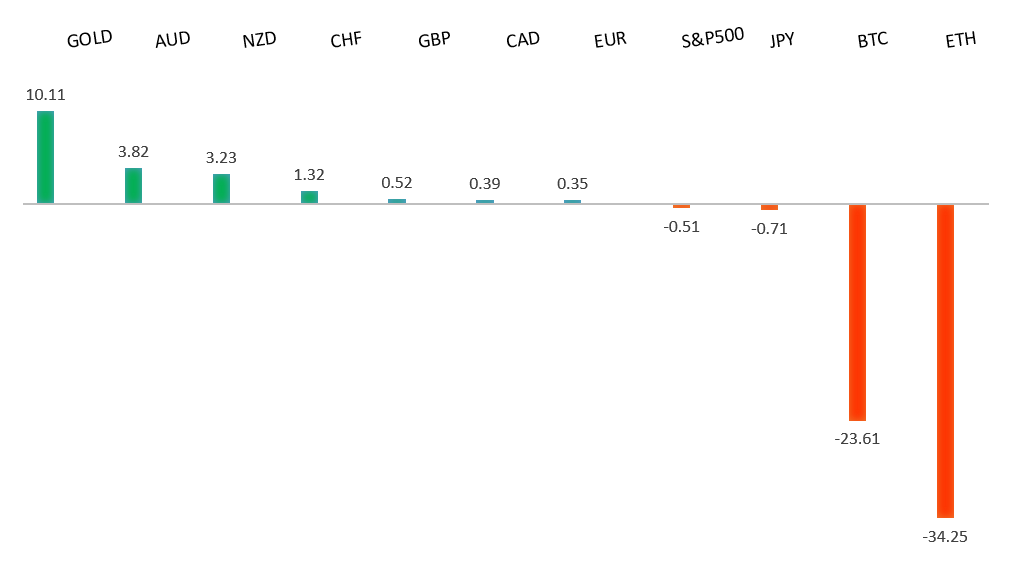

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

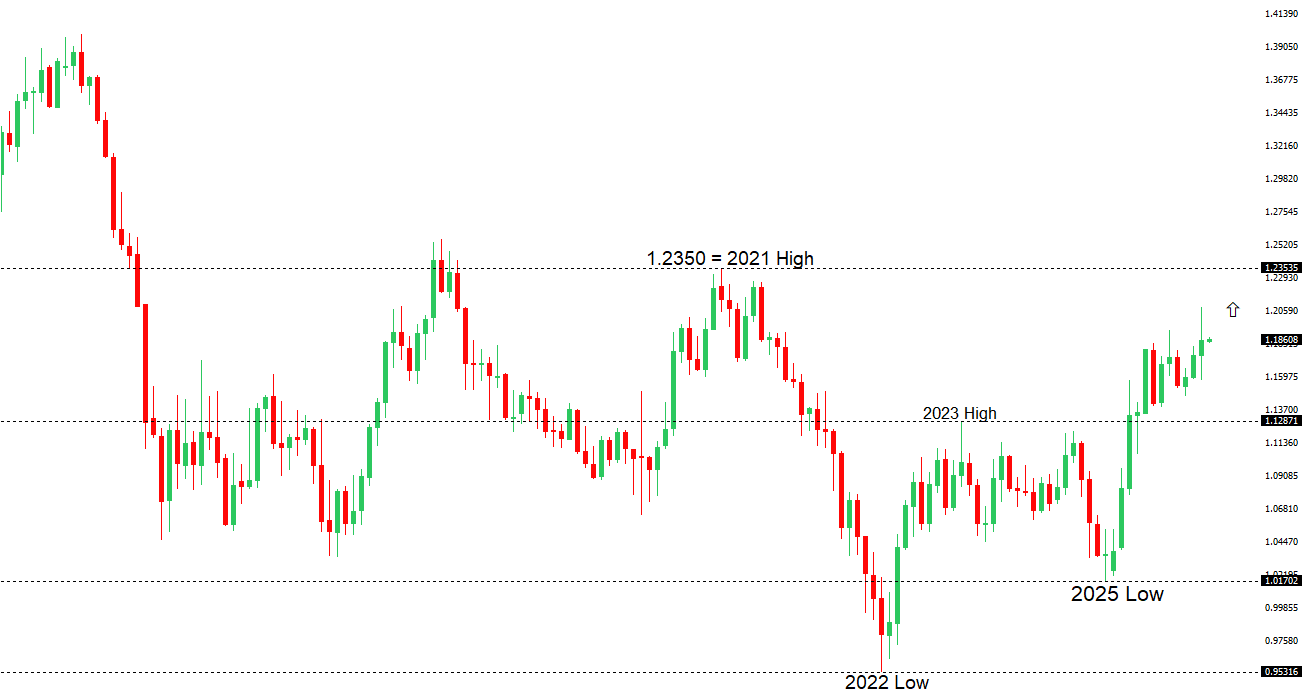

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1500. | ||

| ||

| R2 1.2083 - 27 Janaury/2026 high - Strong R1 1.1875 - 2 February high - Medium S1 1.1776 - 2 February low - Medium S2 1.1728 - 23 January low - Medium | ||

| EURUSD: fundamental overview | ||

| The euro has slipped modestly as a firmer dollar and lingering uncertainty around Europe’s growth and policy outlook weigh on sentiment. Softer inflation—now below target and likely to stay there for some time—has strengthened the case for eventual rate cuts, helped by easing wages, cheaper imports, and lower energy prices. While most analysts see risks tilted toward easing, expectations of steadier medium-term growth (supported by fiscal stimulus) are keeping policymakers in wait-and-see mode and limiting bets on aggressive cuts. Beyond the current pullback, however, the broader outlook for the euro remains constructive, with narrowing rate differentials, recovering eurozone demand, and anticipated U.S. rate cuts supporting forecasts for a gradual move higher against the dollar. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. The recent break below 154.39 strengthens the outlook. | ||

| ||

| R2 157.42 - 19 January low - Strong R1 157.07 - 5 February high - Medium S1 154.55 - 2 February low - Medium S2 151.97 - 28 January/2026 low - Strong | ||

| USDJPY: fundamental overview | ||

| USDJPY is up over 2% in five sessions as investors stay cautious ahead of Japan’s election and a more fragile domestic backdrop. Hedge funds have rebuilt bearish yen positions as the pair drifts toward 156–157, helped by earlier weak-currency remarks from Sanae Takaichi and bullish options flows, while longer-term asset managers remain largely sidelined and favor options over outright longs. Stronger services PMI data has done little for the yen, as markets focus instead on limits to support from Bank of Japan, with authorities leaning mainly on verbal warnings from officials like Satsuki Katayama to curb excessive moves. Overall, markets may be reluctant to chase USDJPY much higher into the vote and a possible earlier BOJ hike, though one Japanese bank cautions that a post-election spike toward 160 could trigger intervention, potentially during the thinner liquidity around Japan’s Feb 11 holiday. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. Setbacks should now be well supported ahead of 0.6300. | ||

| ||

| R2 0.7158 - 2023 high - Strong R1 0.7095 - 29 January/2026 high - Strong S1 0.6901 - 27 January low - Medium S2 0.6834 - 23 January low - Medium | ||

| AUDUSD: fundamental overview | ||

| The Aussie dollar is down about 0.4%, easing back from last week’s near three-year high after a strong January, even as December trade data showed a wider surplus that missed expectations. The Reserve Bank of Australia surprised markets by restarting rate hikes with a unanimous 25bp increase to 3.85%, citing persistent inflation in services and housing alongside tight labor conditions, though Governor Michele Bullock stressed the path ahead remains cautious and data-dependent. Markets have since pared back expectations of an aggressive hiking cycle, now pricing just one further move toward ~4.1% by mid-year, with strategists divided between a “one-and-done” view and calls for at least one more hike. Near term, AUDUSD is likely to retain a modest upside bias, with dips attracting buyers while the RBA stays focused on inflation and the Federal Reserve moves gradually toward easing—keeping 0.71–0.72 in sight, barring setbacks from China or renewed U.S. dollar strength. | ||

| Suggested reading | ||

| Why International Stocks May Win Gold Again in 2026, D. Lefkovitz, Morningstar (February 4, 2026) Bank Profits, Eliminate Risk, Preserve Upside In One Move, C. Reilly, RiskHedge (February 2, 2026) | ||