| ||

| 4th February 2026 | view in browser | ||

| Yen weak, Dollar soft, risk cautiously on | ||

| Markets open with the yen under pressure on Japan election and stimulus risks, the dollar modestly softer into key U.S. data, Europe awaiting PMIs and CPI, bonds holding firm, oil steady on inventory draw hopes, and risk sentiment cautiously positive with equity futures slightly higher. | ||

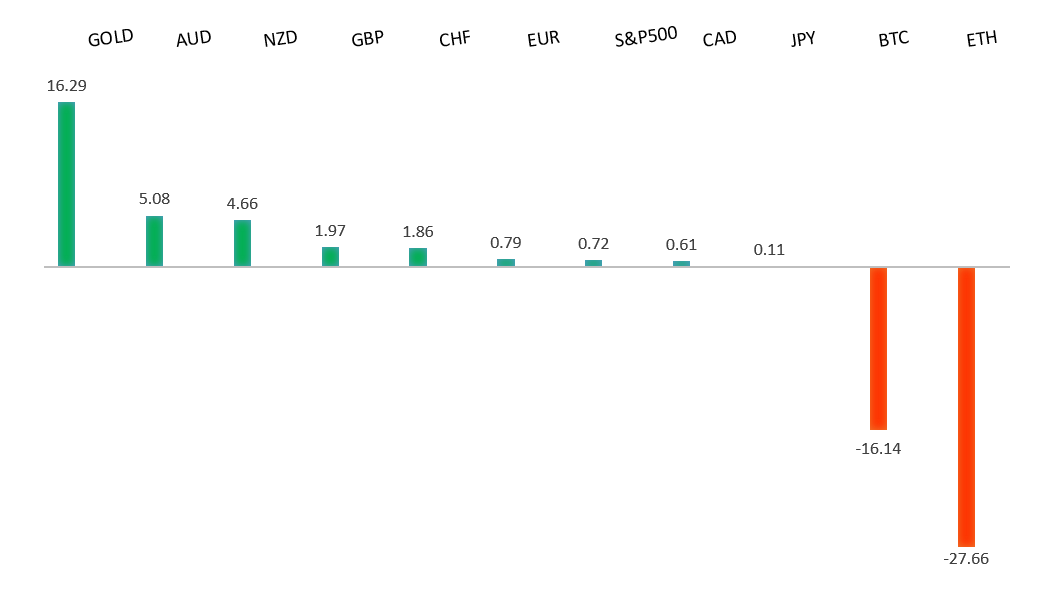

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

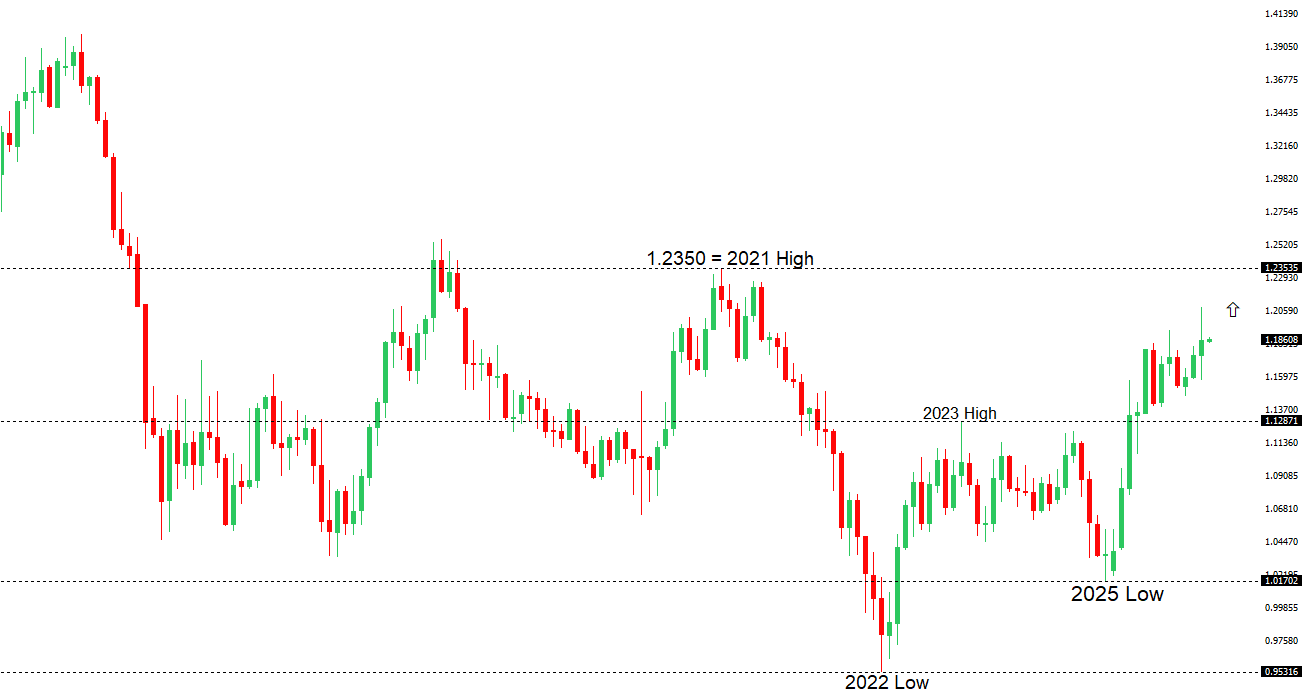

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1500. | ||

| ||

| R2 1.2083 - 27 Janaury/2026 high - Strong R1 1.1875 - 2 February high - Medium S1 1.1776 - 2 February low - Medium S2 1.1728 - 23 January low - Medium | ||

| EURUSD: fundamental overview | ||

| The euro has edged modestly higher, but overall trading is rangebound as investors reassess euro-area growth and policy amid rising uncertainty. Eurozone banks unexpectedly tightened lending in late 2025—especially in Germany and France—raising rates and collateral demands while rejecting more loans, threatening to slow the recovery into 2026. At the same time, trade and geopolitical risks, including higher U.S. tariffs, are weighing on corporate confidence, with the ECB viewing recent euro strength as driven more by mistrust of U.S. politics and external headwinds than strong domestic growth. Heading into this week’s meeting, the ECB is expected to keep rates on hold, and with sticky inflation, resilient labor markets, and weaker credit supply, policymakers are likely to stick to a steady approach—leaving rate differentials broadly stable and supporting the euro without signaling a major policy shift. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. The recent break below 154.39 strengthens the outlook. | ||

| ||

| R2 157.42 - 19 January low - Strong R1 157.00 - Figure - Medium S1 154.55 - 2 February low - Medium S2 151.97 - 28 January/2026 low - Strong | ||

| USDJPY: fundamental overview | ||

| USDJPY climbed about 0.4% in Asia, extending its rally to a fourth day and hovering near a 1½-week high, with the move driven more by yen weakness than dollar strength. Markets are focused on domestic risks in Japan—especially the prospect of expanded fiscal spending and tax cuts—which is reviving concerns over debt-funded growth even as activity data improved and the BOJ shows rising urgency about rate hikes amid persistent above-target inflation. Still, policymakers continue to signal only gradual tightening, keeping US-Japan yield gaps wide, while a soft 10-year JGB auction and elevated yields highlight investor caution ahead of elections and potential stimulus. Overall, traders appear reluctant to push USDJPY much higher given election uncertainty, the risk of an earlier BOJ hike, and sensitivity from authorities to further yen weakness. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. Setbacks should now be well supported ahead of 0.6300. | ||

| ||

| R2 0.7158 - 2023 high - Strong R1 0.7095 - 29 January/2026 high - Strong S1 0.6901 - 27 January low - Medium S2 0.6834 - 23 January low - Medium | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar is holding near multi-year highs after the surprise RBA rate hike, though the initial rally has cooled as markets shift into wait-and-see mode on whether more tightening follows. While the move briefly made AUD the top-performing G10 currency this year, policymakers struck a more cautious, data-dependent tone, prompting yields and AUDUSD to give back some gains as expectations for aggressive follow-up hikes were pared back. Strategists remain split between a “one-or-two-and-done” view and the risk of further tightening, but near term the Aussie retains a modest upside bias, with dips likely supported and a move toward 0.71–0.72 achievable if domestic data stay firm and the Fed begins gradual easing. | ||

| Suggested reading | ||

| Every Major Currency Appreciated Versus Dollar In ’25, B. Ritholz, The Big Picture (February 2, 2026) Tune Out All the Dollar Gloom. It’s Not That Weak, Fisher Investments (January 28, 2026) | ||