| ||

| 8th January 2026 | view in browser | ||

| Soft data, steady policy | ||

| Global macro conditions remain cautious but relatively stable as economies head into the new day. The U.S. continues to show strong productivity and underlying resilience, though a softening labor market is keeping the Fed firmly in wait-and-see mode, with markets leaning toward steady rates and potential cuts later in 2026. | ||

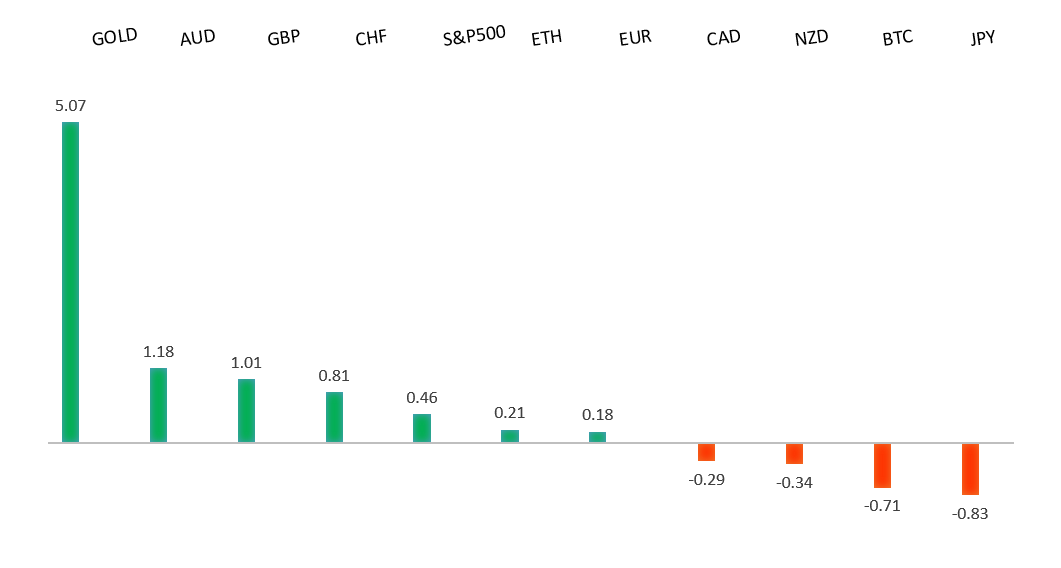

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

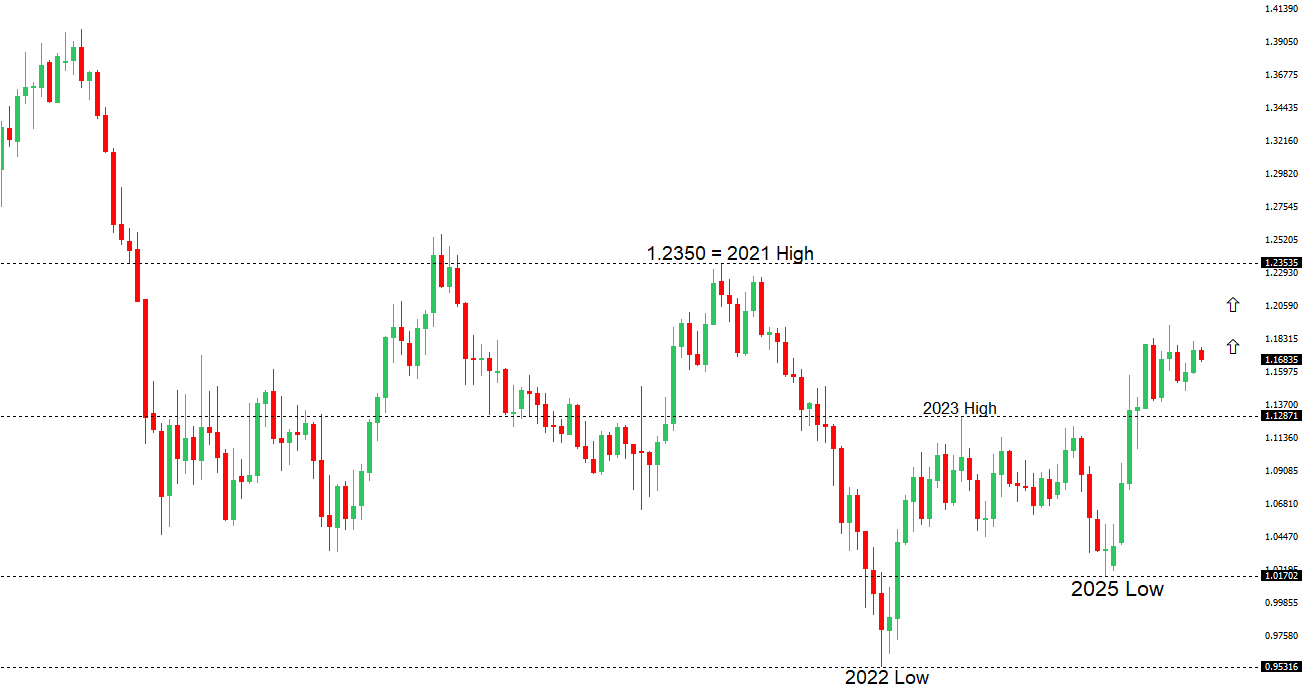

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1400. | ||

| ||

| R2 1.1919 - 17 September/2025 high -Strong R1 1.1765 - 2 Janaury/2026 high - Medium S1 1.1659 - 5 January /2026 low - Medium S2 1.1615 - 9 December low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has been largely quiet in recent sessions as broader USD data and upcoming US labor releases continued to dominate price action. Eurozone December inflation returned to the ECB’s 2% target, easing underlying pressures and reinforcing expectations that rates will remain on hold, with policymakers still cautious and ECB hawks likely to resist near-term cuts. In Germany, weak November retail sales highlighted the fragile state of the consumer, while unemployment remained steady as expected. Geopolitically, Trump’s comments on Greenland drew criticism both domestically and from European leaders, who reaffirmed support for Danish sovereignty and stressed NATO-led cooperation on Arctic security. | ||

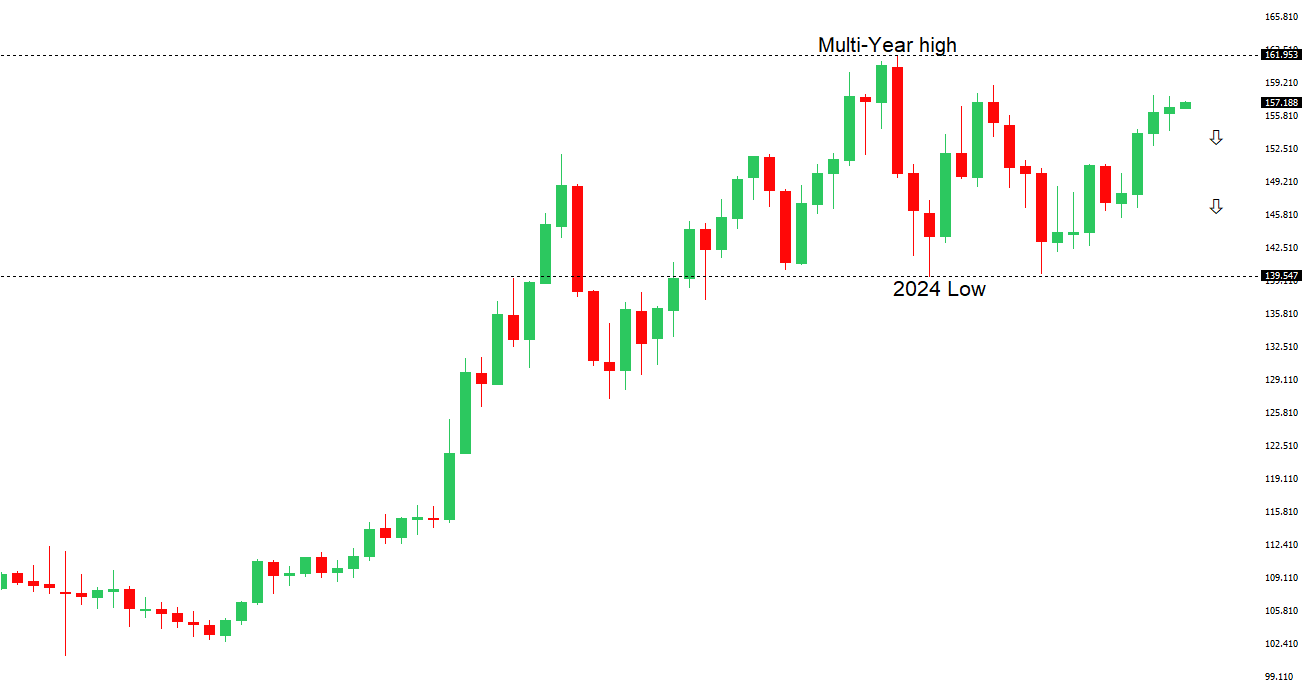

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 ahead of a fresh down-leg back towards the 2024 low at 139.58. A break below 154.39 will strengthen the outlook. | ||

| ||

| R2 157.90 - 20 November/2025 high - Strong R1 157.30 - 5 January /2026 high - Medium S1 155.55 - 24 December low - Medium S2 154.39 - 16 December low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen is little changed as attention remains on Japanese rates, with bond yields easing and markets still debating how quickly the BOJ can normalize policy. November wage data disappointed, with nominal pay growth slowing sharply and real wages falling faster than expected, weakening the case for near-term aggressive tightening and posing risks to household consumption. While some underlying measures suggest pay momentum remains intact, markets are likely to see the data as mildly negative for the yen. Adding to the uncertainty, rising Sino-Japanese trade tensions—especially around rare earths critical to manufacturing—could slow economic growth and reinforce expectations of a more gradual BOJ hiking path. Against this backdrop, global banks remain bearish on the yen into 2026, though sharp moves toward 158–160 could raise the risk of FX intervention without necessarily accelerating rate hikes. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6800 - Figure - Medium R1 0.6767 - 7 January/2026 high - Medium S1 0.6660 - 31 December low - Medium S2 0.6592 - 18 December low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar edged lower after weaker-than-expected November trade data showed a narrower surplus, with exports falling and imports rising, while softer gold prices also weighed. Markets have slightly pared back expectations for RBA tightening, now pricing only modest odds of a rate hike by early 2026, though medium-term inflation risks from subsidy removal and price resets continue to support the case for eventual tightening. A rising commodity complex, easing Fed policy expectations, and ongoing short-covering in AUD positioning have helped lift AUDUSD since mid-December, suggesting further gains could be driven by commodities and macro fundamentals rather than positioning alone. | ||

| Suggested reading | ||

| 4 Investing Ideas for 2026 From Great Money Minds, D. Lefkovitz, Morningstar (January 7, 2026) A Few Things I’m Pretty Sure About, M. Housel, Collaborative Fund (January 6, 2026) | ||