| ||

| 9th January 2026 | view in browser | ||

| Geopolitics, inflation and payrolls | ||

| Global markets kick off with geopolitics in focus as the US deepens involvement in Venezuela’s oil revival and eyes regional security, while investors also parse today’s key US labor data for clues on growth and rates. At the same time, easing inflation across Europe and mixed economic signals globally are keeping central banks cautious and market expectations finely balanced. | ||

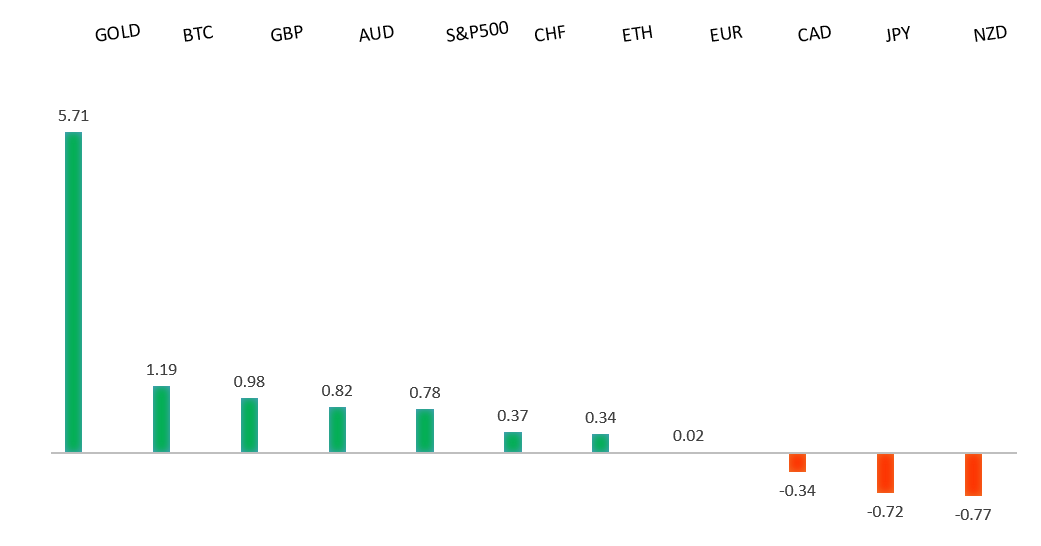

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

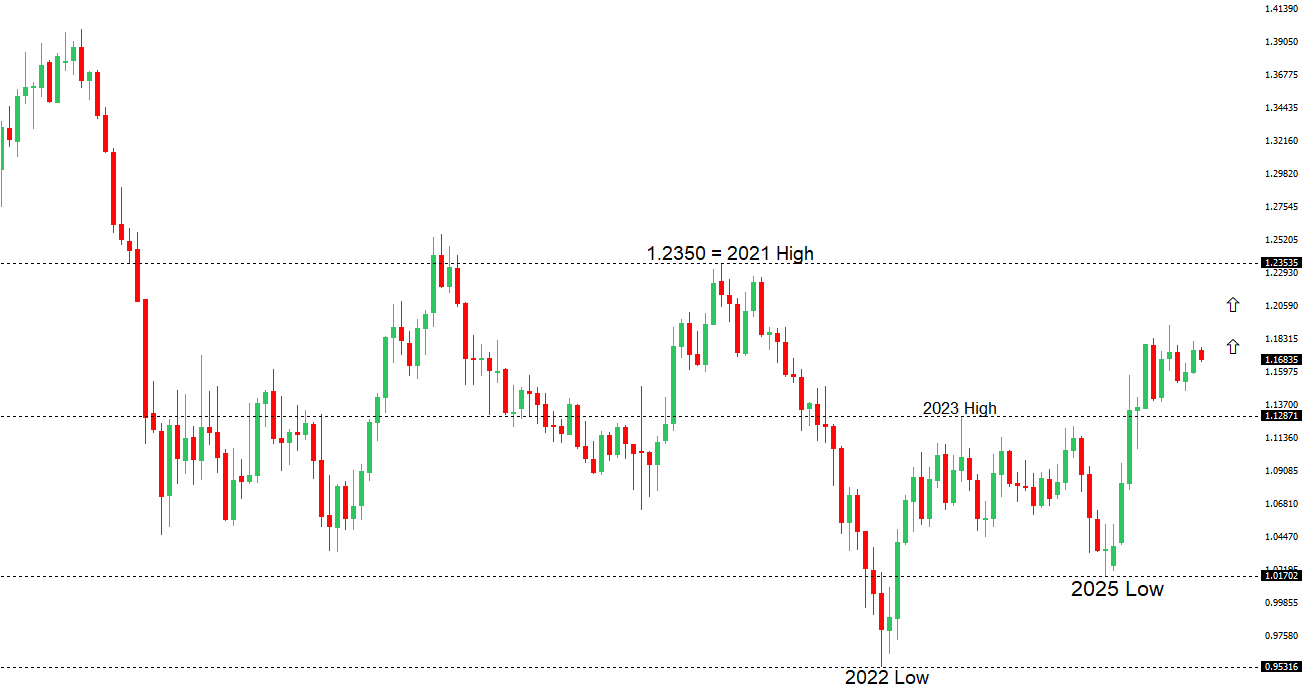

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1400. | ||

| ||

| R2 1.1919 - 17 September/2025 high -Strong R1 1.1765 - 2 Janaury/2026 high - Medium S1 1.1642 - 8 January /2026 low - Medium S2 1.1615 - 9 December low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has been quietly consolidating, hovering near a four-week low as a firmer dollar and pre-NFP positioning weighed on sentiment. Eurozone data, however, remain relatively supportive: unemployment fell to 6.3% in November, job creation continued into December, growth in Q4 was the strongest since 2023, and inflation expectations stayed anchored just above 2%, suggesting the ECB is likely to keep rates on hold for longer. German factory orders also surprised to the upside, while geopolitical tensions rose after criticism from President Macron toward Washington and fresh Russian strikes on Ukraine. | ||

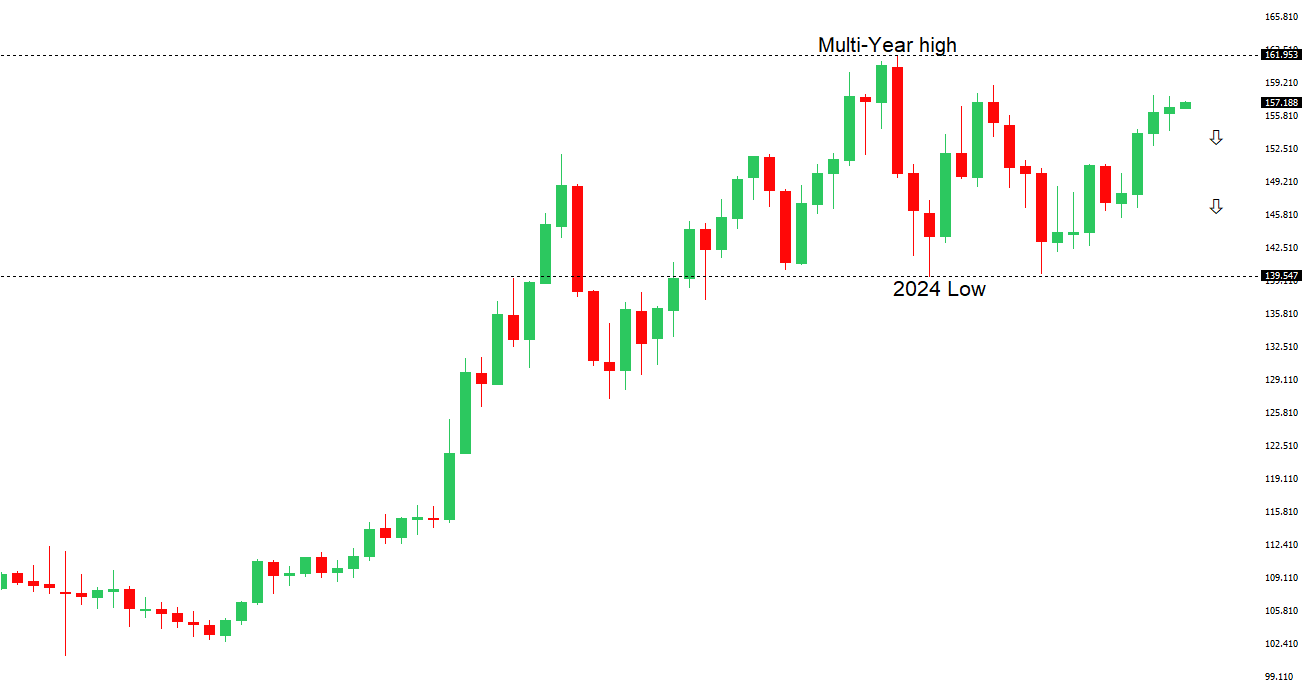

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 ahead of a fresh down-leg back towards the 2024 low at 139.58. A break below 154.39 will strengthen the outlook. | ||

| ||

| R2 157.90 - 20 November/2025 high - Strong R1 157.44 - 9 January /2026 high - Medium S1 155.55 - 24 December low - Medium S2 154.39 - 16 December low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen is under mild pressure but still holding within a narrow weekly range despite softer-than-expected wage data, as investors await fresh direction from upcoming US labor figures. The BOJ’s latest regional report reassured markets that Japan’s economy is still recovering and that further gradual rate hikes remain likely, supported by expectations of another strong round of wage increases. However, potential Chinese restrictions on rare-earth exports to Japan could weigh on manufacturing and slow the BOJ’s tightening path, reinforcing forecasts from major banks that the yen may weaken toward 160 per dollar or beyond over the medium term. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6800 - Figure - Medium R1 0.6767 - 7 January/2026 high - Medium S1 0.6660 - 31 December low - Medium S2 0.6592 - 18 December low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar has been under pressure, extending its pullback from a 15-month high, as weaker-than-expected November trade data and softer gold prices weighed on sentiment. The smaller trade surplus signals softer demand for key exports like iron ore, coal and LNG, while markets have slightly scaled back expectations for an RBA rate hike in early 2026. That said, the broader backdrop remains supportive for the AUD, with strong commodity prices, a rising Bloomberg Commodity Index, and the RBA signaling that rate cuts are likely over — a stance that contrasts with expected Fed easing and could help the AUD regain upside momentum. | ||

| Suggested reading | ||

| A Simple Metric To Predict Future Stock Returns, L. Swedroe, Morningstar (January 8, 2026) Rebuilding Ukraine Could Be Top Euro Investment Theme, J. Klement, Reuters (January 7, 2026) | ||