| ||

| 23rd June 2026 | view in browser | ||

| Hawkish Fed and firm dollar weigh on sentiment | ||

| Markets are starting the day on a cautious footing as a hawkish Fed, persistent dollar strength and ongoing currency stress across Asia offset easing Middle East supply fears and keep pressure on risk sentiment. | ||

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

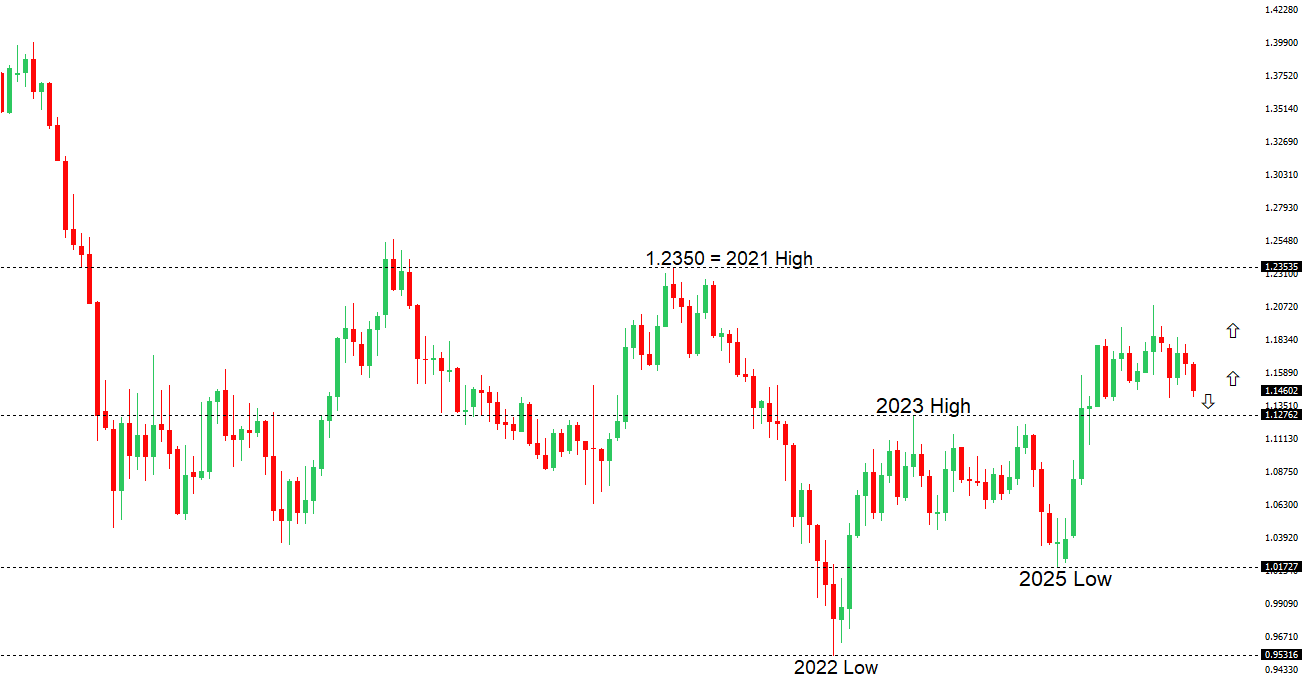

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1622 - 15 June high - Medium R1 1.1529 - 18 June high - Medium S1 1.1418 - 19 June low - Medium S2 1.1411 - 13 March/2026 low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro remains under modest pressure as the U.S. Dollar continues to benefit from a more hawkish Federal Reserve outlook following last week’s FOMC meeting. Markets have significantly increased expectations for additional Fed tightening under Chair Kevin Warsh, supporting U.S. yields and widening the policy divergence with the ECB. At the same time, lingering uncertainty surrounding the reported U.S.-Iran peace initiative has encouraged some safe-haven demand for the Dollar after conflicting signals emerged from Washington and Tehran regarding nuclear monitoring commitments. On the euro side, expectations that the ECB is nearing the end of its tightening cycle have limited upside momentum, even as policymakers continue to stress vigilance on inflation. Traders are now focused on the latest PMI data from Germany, the broader Eurozone, and the United States for fresh insight into relative growth trends, with signs of softer Eurozone activity likely to reinforce the current bias favoring the Dollar over the single currency. | ||

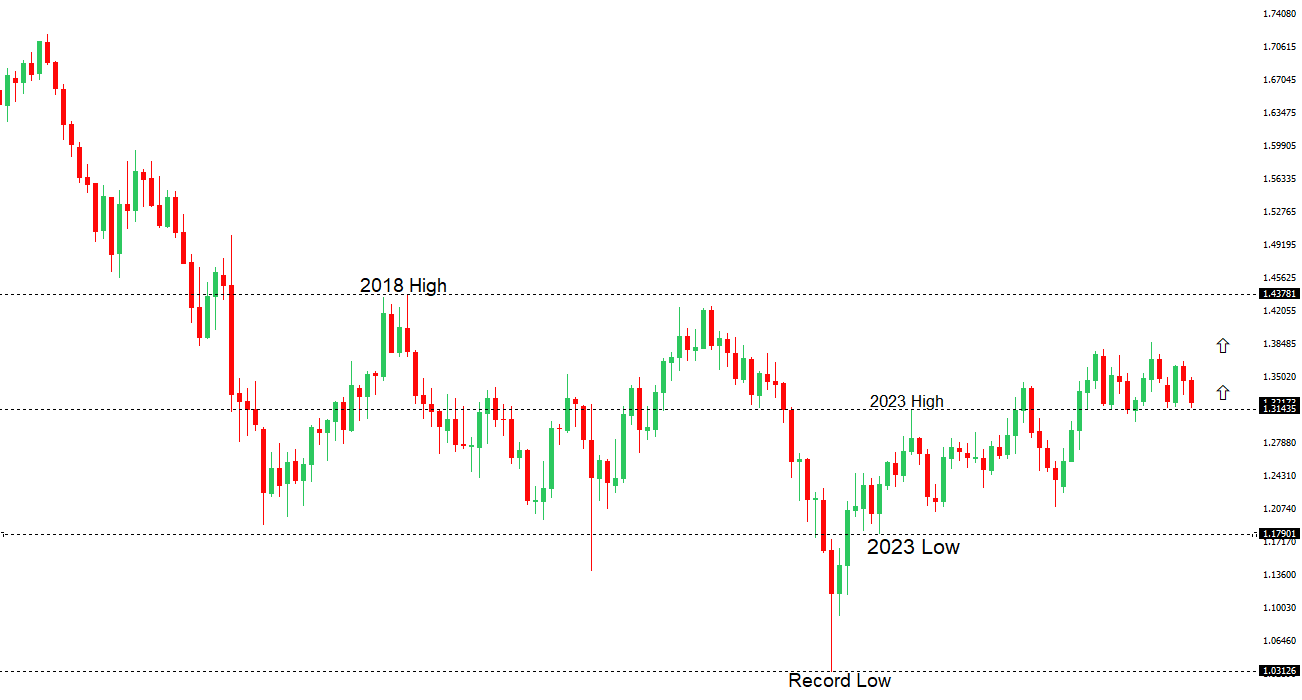

| GBPUSD: technical overview | ||

| The Pound remains exceptionally well supported on dips into the 1.3000 area, with the price largely consolidating above the psychological barrier and previous resistance turned support in the form of the 2023 high. Look for the market to continue be well supported on dips ahead of the next major upside extension through the yearly high at 1.3870 and towards a retest of the 2018 high at 1.4377 further up. Only a monthly close below 1.3000 negates. | ||

| ||

| R2 1.3509 - 25 May high - Strong R1 1.3325 - 18 June high - Medium S1 1.3163 - 19 June low - Medium S2 1.3159 - 31 May/2026 low - Strong | ||

| GBPUSD: fundamental overview | ||

| The pound has held up relatively well in the face of Prime Minister Keir Starmer’s resignation, suggesting much of the risk may have already been priced in and reflecting resilience from still-elevated UK inflation and expectations that the Bank of England will remain relatively cautious about easing policy. At the same time, a broader risk-off tone in global markets, driven by uncertainty surrounding the US-Iran peace process and lingering geopolitical concerns, has supported the US dollar and weighed on GBPUSD into Tuesday. Investors are also mindful of the Federal Reserve’s increasingly hawkish stance, which has reinforced US yield support and widened the policy divergence narrative. Attention now turns to the latest UK and US PMI data for a clearer read on economic momentum and whether sterling can continue to weather political headwinds better than many of its G10 peers. | ||

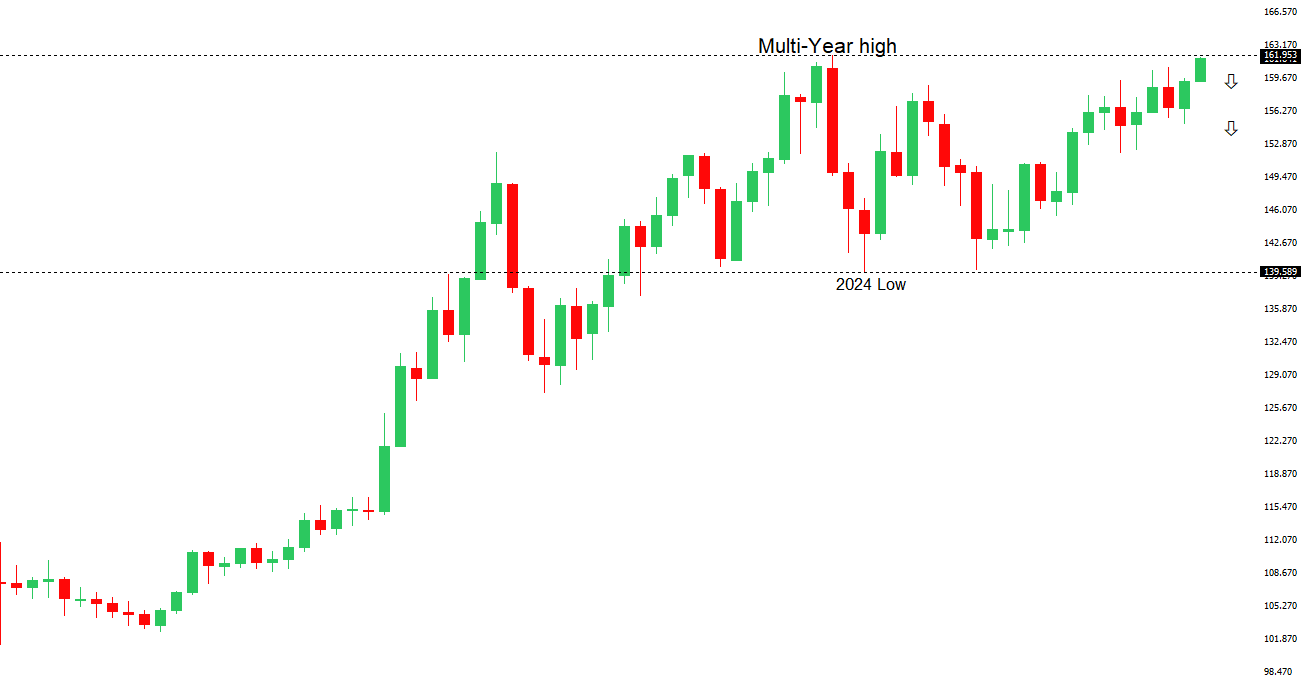

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped below 162.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 162.00 negates. | ||

| ||

| R2 161.96 - Multi-Year high/2024 - Very Strong R1 161.93 - 22 June/2026 high - Strong S1 160.41 - 18 June low - Medium S2 159.54 - 11 June low - Strong | ||

| USDJPY: fundamental overview | ||

| The Yen remains under pressure as markets continue to focus on the wide interest rate differential between the U.S. and Japan, with the Federal Reserve maintaining a hawkish bias while the Bank of Japan remains cautious about tightening policy further. Although Japanese inflation remains above the BOJ’s 2% target, recent core-core inflation measures have continued to ease, reinforcing concerns that underlying domestic price pressures are moderating even as higher energy costs linked to Middle East tensions threaten to push headline inflation higher. This leaves the BOJ facing a difficult balancing act, as policymakers are reluctant to tighten aggressively in response to imported cost-push inflation that could undermine the fragile wage-price cycle and economic recovery. Meanwhile, escalating geopolitical risks and concerns over potential disruptions to energy supplies through the Strait of Hormuz have supported safe-haven demand for the U.S. Dollar, helping USDJPY hold near multi-year highs despite persistent intervention warnings from Japanese officials and growing speculation that authorities could step into the market if Yen weakness accelerates further. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7201 - 29 May high - Strong R1 0.7089 - 15 June high - Medium S1 0.6944 - 3 March low - Medium S2 0.6900 - Figure - Medium | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar remains under pressure, weighed down primarily by a stronger US dollar as markets continue to price a more hawkish Federal Reserve following last week’s FOMC meeting and Chair Kevin Warsh’s emphasis on price stability. Escalating geopolitical uncertainty surrounding the US-Iran situation and concerns over the Strait of Hormuz have also supported safe-haven demand for the greenback and undermined risk-sensitive currencies such as the Aussie. That said, the broader AUD backdrop remains relatively constructive. Australia’s economy continues to show resilience, inflation remains above target, and the Reserve Bank of Australia has maintained a cautious, mildly hawkish stance, keeping the prospect of further tightening on the table if price pressures persist. Supporting this view, preliminary June PMI data surprised to the upside, with manufacturing improving to 51.2 and services recovering to 49.9, signalling stabilization in domestic activity. Meanwhile, China remains more of a stabilizing influence than a growth engine, helping to prevent a sharper deterioration in sentiment toward Australia’s outlook. For now, however, AUDUSD is being driven more by global risk appetite, Fed expectations, and geopolitical developments than by domestic fundamentals, leaving the currency vulnerable despite generally supportive medium-term fundamentals. | ||

| Suggested reading | ||

| Could AI chatbots undo the harms of social media?, J. Burn-Murdoch, Financial Times (June 18, 2026) It Turns Out Kevin Warsh Has Other Plans for Interest Rates, M. Rzepczynski, Marketwatch (June 19, 2026) | ||