| ||

| 22nd June 2026 | view in browser | ||

| From escalation risk to negotiation risk | ||

| Markets are starting the week with a cautiously risk-positive tone as encouraging progress in U.S.-Iran negotiations eases immediate fears of a major energy supply disruption, weighing on oil and the dollar while investors balance improving geopolitical sentiment against a still hawkish Federal Reserve backdrop. | ||

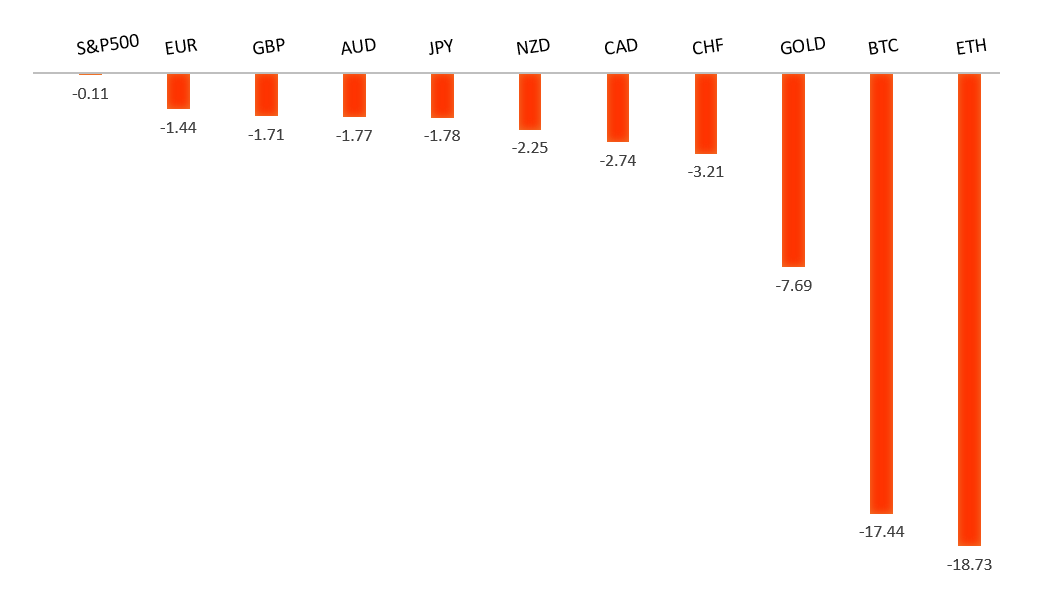

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

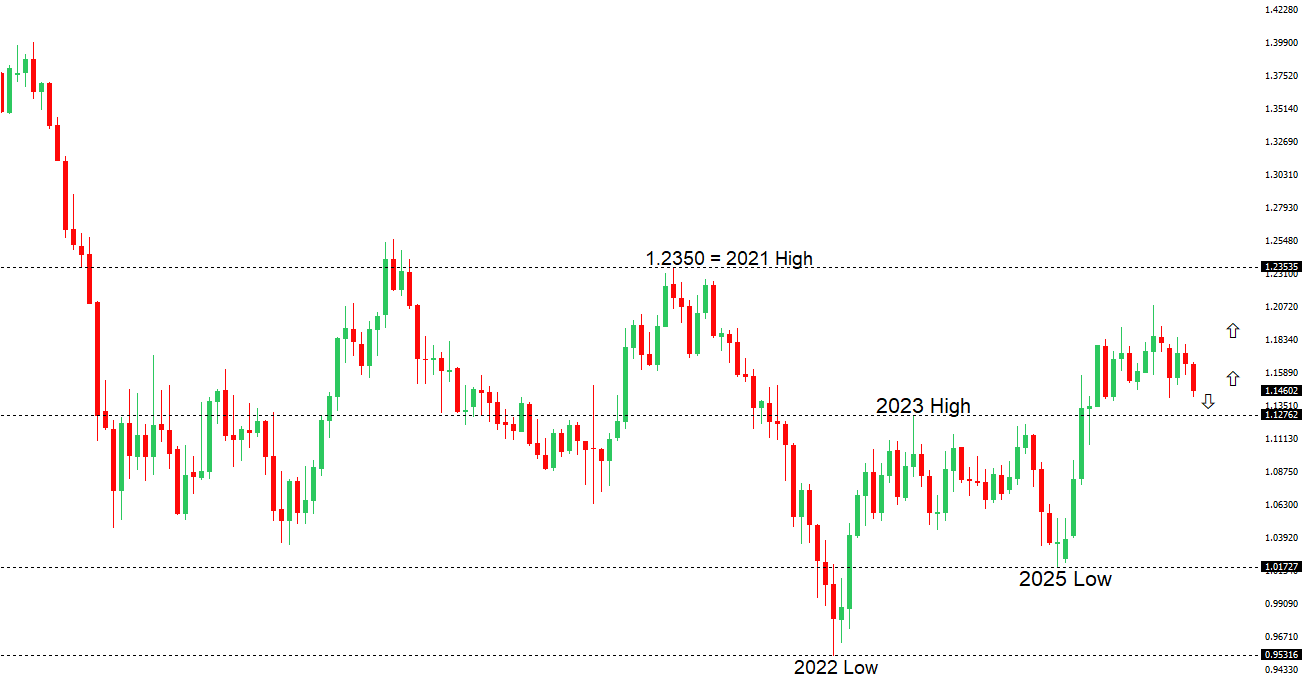

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1622 - 15 June high - Medium R1 1.1529 - 18 June high - Medium S1 1.1418 - 19 June low - Medium S2 1.1411 - 13 March/2026 low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro remains supported by a relatively resilient ECB outlook, but is struggling to make further gains against a broadly stronger U.S. Dollar. Recent ECB communication, including signals that policymakers remain cautious about declaring victory over inflation, has helped underpin the single currency and reinforced expectations that rates will stay restrictive for longer. However, EURUSD continues to face headwinds from the post-Fed repricing toward a more hawkish U.S. policy path under Chair Warsh, with markets increasingly factoring in the possibility of additional tightening later this year. Geopolitical developments surrounding the Middle East and uncertainty around the durability of any U.S.-Iran peace agreement have also supported safe-haven demand for the Dollar at times, limiting upside in the euro. As a result, the pair remains caught between a still relatively firm ECB backdrop and a U.S. Dollar that continues to draw support from higher yields, policy divergence, and cautious risk sentiment. | ||

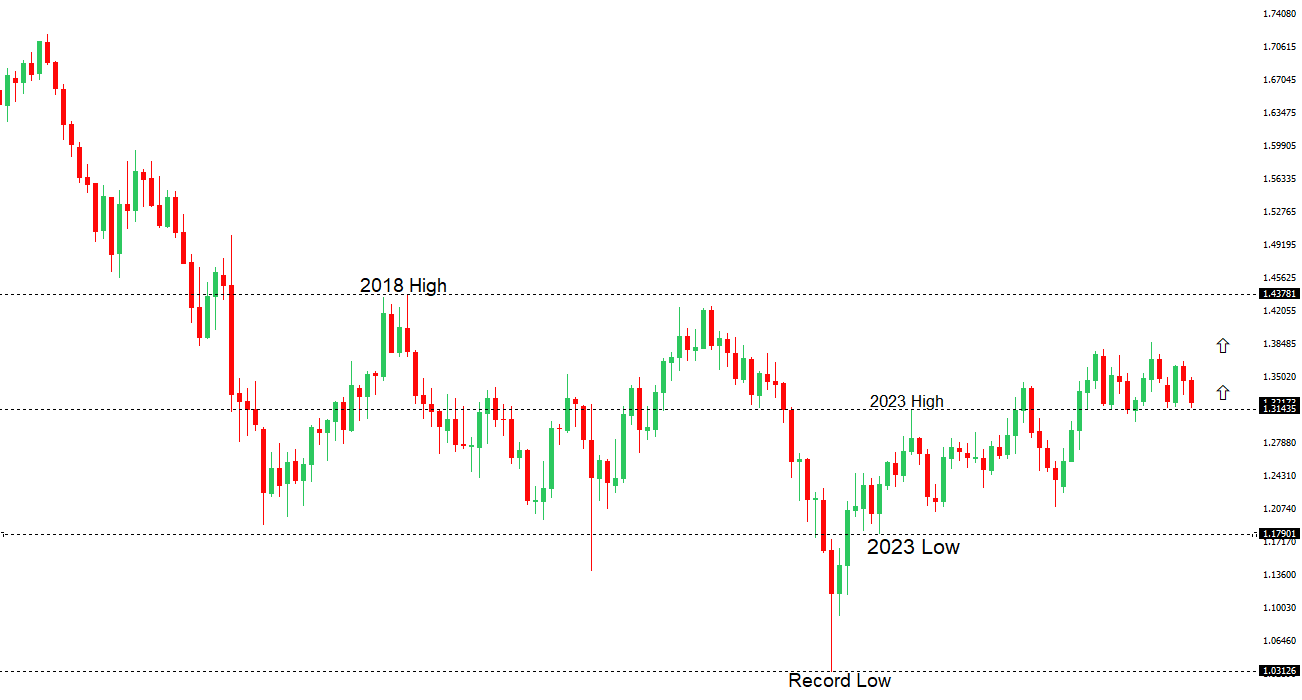

| GBPUSD: technical overview | ||

| The Pound remains exceptionally well supported on dips into the 1.3000 area, with the price largely consolidating above the psychological barrier and previous resistance turned support in the form of the 2023 high. Look for the market to continue be well supported on dips ahead of the next major upside extension through the yearly high at 1.3870 and towards a retest of the 2018 high at 1.4377 further up. Only a monthly close below 1.3000 negates. | ||

| ||

| R2 1.3509 - 25 May high - Strong R1 1.3325 - 18 June high - Medium S1 1.3163 - 19 June low - Medium S2 1.3159 - 31 May/2026 low - Strong | ||

| GBPUSD: fundamental overview | ||

| The pound starts the week on the defensive, with GBPUSD slipping back toward the 1.3200 area as investors digest a combination of renewed UK political uncertainty and a more supportive backdrop for the US dollar. Reports suggesting Prime Minister Keir Starmer could outline a timetable for his departure have injected fresh political risk into UK assets, weighing on sterling despite the UK’s relatively resilient economic backdrop. At the same time, the dollar continues to draw support from the Federal Reserve’s hawkish shift under Chair Warsh, with markets now pricing a meaningful chance of additional rate hikes in the months ahead following last week’s policy meeting and emphasis on price stability. While recent UK data, including stronger retail sales and firmer labor market indicators, has helped reinforce expectations that the Bank of England will remain cautious about easing policy, those supportive domestic fundamentals are currently being overshadowed by political headlines and widening policy divergence concerns as investors reassess the outlook for UK growth, rates, and leadership. | ||

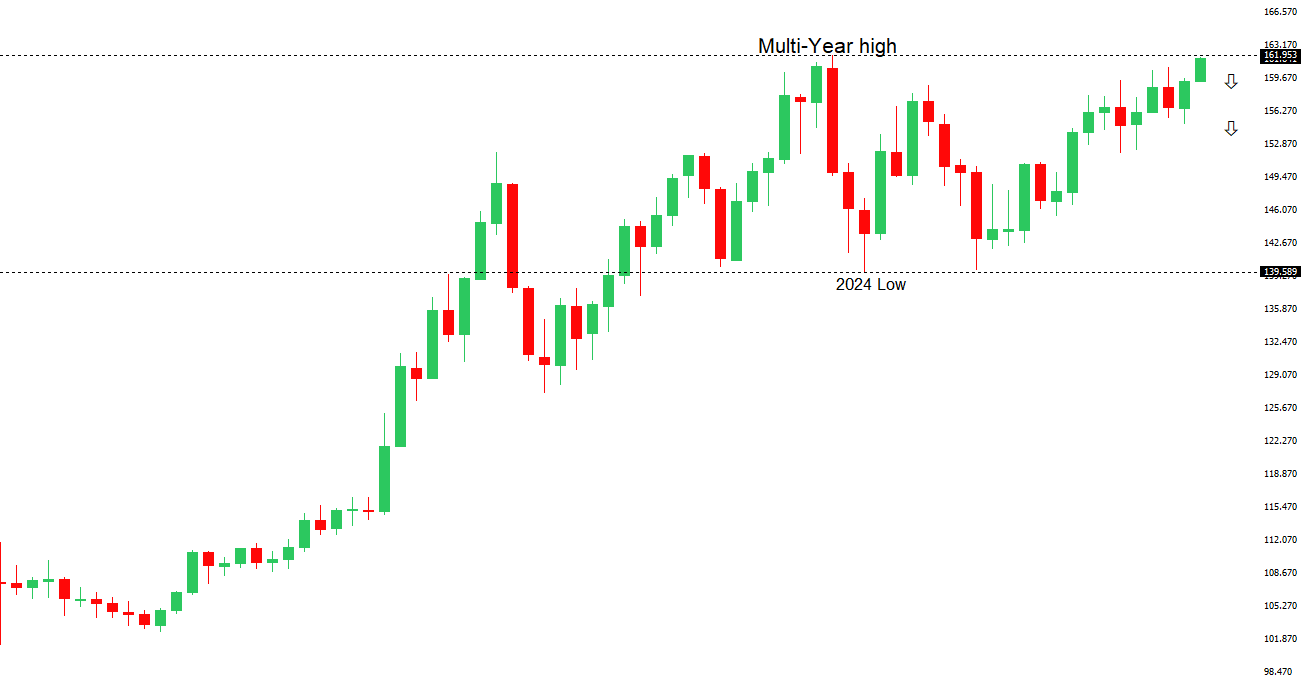

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped below 162.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 162.00 negates. | ||

| ||

| R2 161.96 - Multi-Year high/2024 - Very Strong R1 161.81 - 18 June/2026 high - Strong S1 160.41 - 18 June low - Medium S2 159.54 - 11 June low - Strong | ||

| USDJPY: fundamental overview | ||

| The Yen remains under pressure as the divergence between Bank of Japan and Federal Reserve policy continues to dominate price action. While the BOJ recently raised rates to 1.00% and Deputy Governor Himino has maintained a hawkish tone, warning that delaying further tightening risks an inflation overshoot as higher energy costs feed through the economy, markets remain skeptical that the central bank will be able to move aggressively given political resistance from Prime Minister Takaichi, who has publicly called for policy restraint and closer coordination with the government. At the same time, the Fed’s hawkish stance and expectations for additional US tightening have preserved a wide US-Japan yield differential, encouraging carry trades and supporting USDJPY. The Yen has also failed to benefit from intervention warnings from Japanese officials, with investors instead focusing on concerns that higher energy prices and ongoing Middle East tensions could weigh on Japan’s import-dependent economy. As a result, USDJPY remains near multi-year highs, with the balance of risks still tilted toward Yen weakness unless either US yields retreat materially or markets gain confidence that the BOJ can continue its normalization path despite growing political headwinds. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7201 - 29 May high - Strong R1 0.7089 - 15 June high - Medium S1 0.6979 - 11 June low - Medium S2 0.6963 - 8 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian Dollar remains caught between a still-supportive domestic rate backdrop and a stronger, more defensive US Dollar environment. On the one hand, the RBA’s decision to leave rates unchanged at 4.35% was interpreted as a hawkish pause rather than the end of the tightening cycle, with policymakers signalling that further rate hikes remain possible if inflation proves persistent. That continues to offer underlying support to the Aussie. On the other hand, renewed uncertainty surrounding the US-Iran peace process, including fresh threats from President Trump and lingering concerns around Middle East stability, has weighed on broader risk sentiment and reduced demand for growth-sensitive currencies such as the AUD. China-related developments have been largely neutral, with the PBOC leaving its Loan Prime Rates unchanged as expected, reinforcing a steady policy stance but offering little fresh catalyst for the China-proxy Australian Dollar. As a result, AUDUSD remains anchored around the 0.7000 area, with the currency balancing support from relatively high Australian yields against headwinds from a firmer US Dollar, elevated US rate expectations, and lingering geopolitical uncertainty. | ||

| Suggested reading | ||

| Why ‘pump anxiety’ promps surge in EV sales, K. Inagaki, Financial Times (June 18, 2026) Are Today’s Earnings Gains Sustainable?, M. Rzepczynski, Disciplined Global Macro (June 18, 2026) | ||