| ||

| 19th June 2026 | view in browser | ||

| A hawkish anchor in a restless world | ||

| Markets enter the new day with the U.S. dollar supported by the Fed’s hawkish shift and renewed Middle East uncertainty after U.S.-Iran talks stalled, keeping pressure on major currencies, underpinning oil prices, and leaving investors cautious toward risk assets despite resilient economic data and stronger-than-expected UK retail sales. | ||

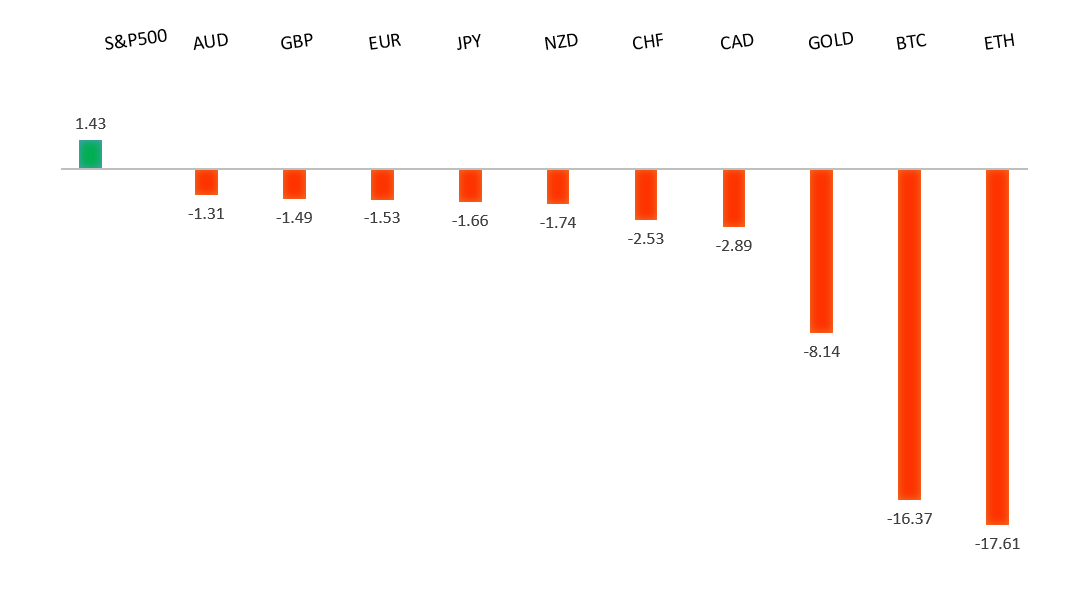

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1622 - 15 June high - Medium R1 1.1529 - 18 June high - Medium S1 1.1418 - 19 June low - Medium S2 1.1411 - 13 March/2026 low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has come under pressure primarily from a resurgent U.S. Dollar following the Federal Reserve’s hawkish policy shift under Chair Warsh. Markets are increasingly pricing the risk of additional Fed tightening later this year, widening the policy divergence between the Fed and the ECB and supporting the Dollar against most major currencies. While the ECB’s recent communication has leaned somewhat hawkish and helped limit the euro’s downside, investors remain focused on the prospect of higher U.S. rates and elevated Treasury yields, which continue to favor Dollar demand. At the same time, easing concerns around a broader Middle East disruption and hopes for renewed diplomatic efforts have reduced some safe-haven demand for the euro, while mixed European growth prospects and softer risk sentiment have left the single currency struggling to regain momentum. Overall, EURUSD remains largely driven by the market’s reassessment of a more restrictive Fed outlook, with any euro support from the ECB being overshadowed by the stronger shift in U.S. rate expectations. | ||

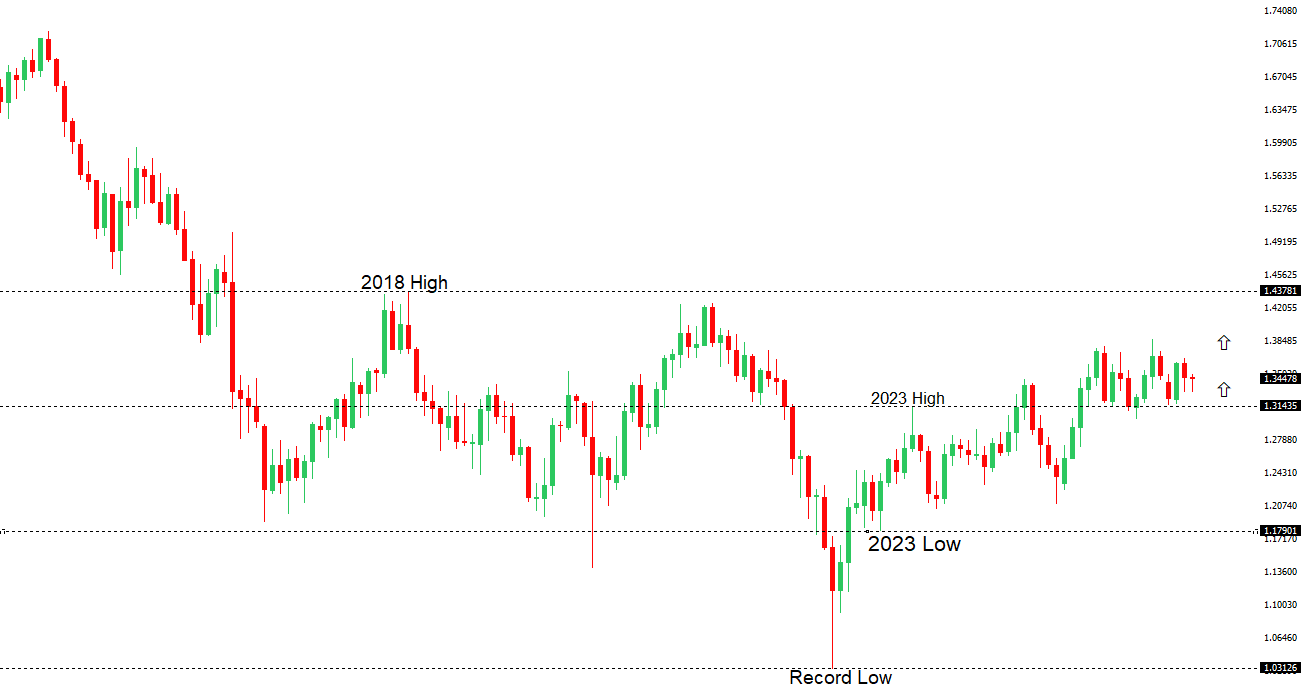

| GBPUSD: technical overview | ||

| The Pound remains exceptionally well supported on dips into the 1.3000 area, with the price largely consolidating above the psychological barrier and previous resistance turned support in the form of the 2023 high. Look for the market to continue be well supported on dips ahead of the next major upside extension through the yearly high at 1.3870 and towards a retest of the 2018 high at 1.4377 further up. Only a monthly close below 1.3000 negates. | ||

| ||

| R2 1.3509 - 25 May high - Strong R1 1.3325 - 18 June high - Medium S1 1.3163 - 19 June low - Medium S2 1.3159 - 31 May/2026 low - Strong | ||

| GBPUSD: fundamental overview | ||

| The Pound is ending the week on firmer footing after a much stronger-than-expected UK Retail Sales report reinforced signs of resilience in the consumer sector. Retail sales rose 1.2% in May, more than double expectations, while annual sales growth accelerated to 3.2%, with department stores, online retailers, and technology-related purchases benefiting from warm weather, promotions, and recent product launches. The data helped Sterling recover after recent pressure from softer UK inflation readings and the Bank of England’s decision to leave rates unchanged while maintaining a cautious, data-dependent stance. That said, the strong retail figures are unlikely to materially alter near-term BoE expectations, with policymakers still monitoring evidence that inflation pressures are easing. Meanwhile, broader GBPUSD direction continues to be heavily influenced by the US Dollar, which remains supported by a more hawkish Federal Reserve outlook and higher US yields. As a result, while the retail sales surprise has provided the Pound with a welcome boost, Sterling remains caught between encouraging domestic economic resilience and an external backdrop dominated by Dollar strength. | ||

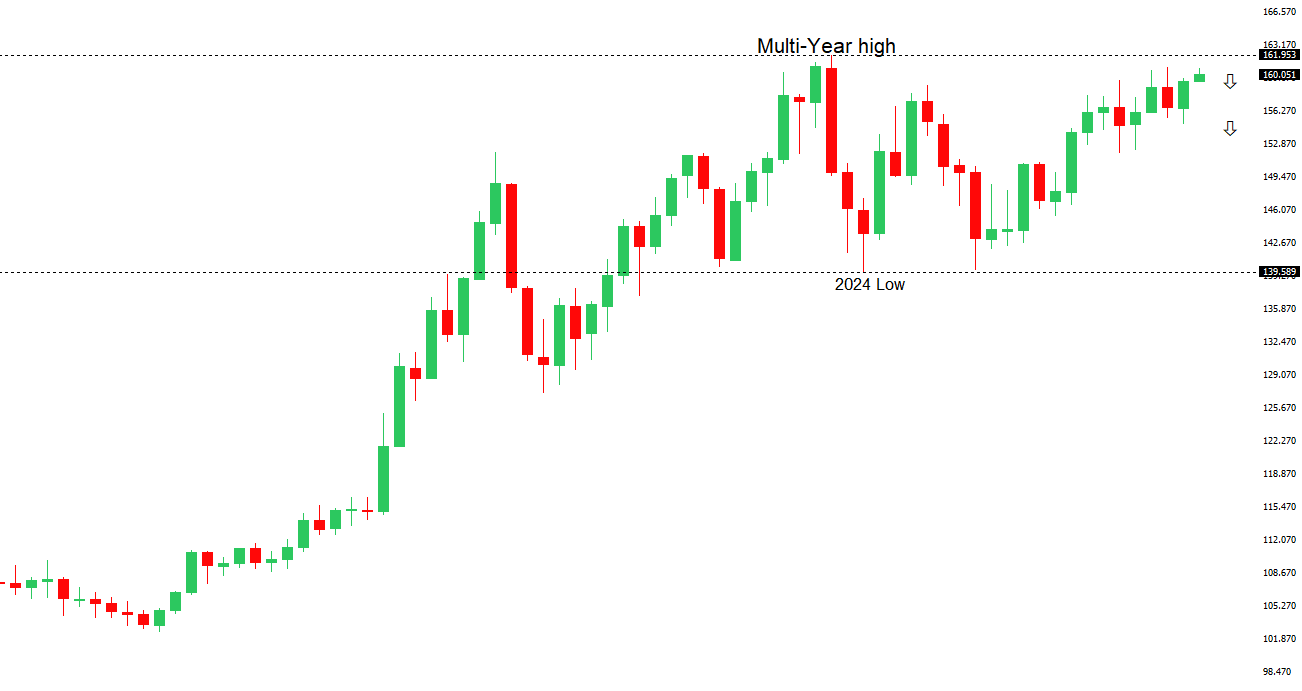

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped below 162.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 162.00 negates. | ||

| ||

| R2 161.96 - Multi-Year high/2024 - Very Strong R1 161.81 - 18 June/2026 high - Strong S1 160.41 - 18 June low - Medium S2 159.54 - 11 June low - Strong | ||

| USDJPY: fundamental overview | ||

| The Yen remains under pressure primarily because of the widening policy divergence between the Federal Reserve and the Bank of Japan, with the Fed’s hawkish June meeting prompting markets to price in a meaningful chance of additional US tightening while US Treasury yields remain elevated. That dynamic has helped drive USDJPY to its highest levels in decades, even as the pair has pulled back modestly from recent highs. On the domestic side, the BoJ delivered an expected rate hike to 1.00% and continues to signal a gradual normalization path, with recent comments from officials and the April meeting minutes reinforcing expectations for further tightening if economic and inflation conditions permit. However, softer Japanese inflation data and inflation measures still running below the BoJ’s 2% target have tempered expectations for an aggressive hiking cycle, limiting support for the Yen. At the same time, growing concern from Japanese officials over the currency’s rapid depreciation, including renewed warnings that authorities stand ready to respond to excessive FX moves, has increased intervention speculation and helped slow the pace of Yen weakness. More recently, some easing in geopolitical tensions following reports of progress toward a US-Iran agreement and the associated pullback in safe-haven demand for the US Dollar have allowed the Yen to recover modestly, though the broader bias remains for USDJPY strength as long as Fed-BoJ policy divergence persists. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7201 - 29 May high - Strong R1 0.7089 - 15 June high - Medium S1 0.6979 - 11 June low - Medium S2 0.6963 - 8 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian Dollar remains primarily at the mercy of broader US Dollar dynamics and global risk sentiment, with the currency struggling to regain upside momentum after the Federal Reserve’s hawkish June meeting under Chair Kevin Warsh. The Fed’s shift toward a higher-for-longer policy outlook has boosted the US Dollar and pressured AUDUSD back toward the 0.7000 area, while lingering uncertainty around US-Iran negotiations and Middle East developments has further weighed on risk-sensitive currencies like the Aussie. Domestically, however, the Australian backdrop remains relatively supportive. The Reserve Bank of Australia maintained its hawkish bias at its latest meeting, emphasizing that inflation remains above target and that further tightening cannot be ruled out if price pressures persist. While economic growth has moderated and labor market conditions have softened somewhat, inflation remains sticky enough to justify the RBA’s cautious stance. Australia’s trade balance has improved, China—the country’s largest trading partner—has stabilized rather than deteriorated, and speculative positioning remains historically constructive despite recent trimming of bullish bets. As a result, the near-term direction for the Australian Dollar is likely to remain heavily influenced by US interest rate expectations and risk appetite, though the combination of resilient domestic fundamentals and a still-cautious RBA continues to provide an underlying source of support. | ||

| Suggested reading | ||

| The Fed Has Been Honest…and Stupid, T. Buchholz, Project Syndicate (June 16, 2026) The Many Costs of Investing, S. Denton, Carson Group (June 17, 2026) | ||